Exam 12: Perfect Competition and the Supply Curve

Exam 1: First Principles198 Questions

Exam 2: Economic Models295 Questions

Exam 3: Supply and Demand264 Questions

Exam 4: Consumer and Producer Surplus228 Questions

Exam 5: Price Controls and Quotas215 Questions

Exam 6: Elasticity88 Questions

Exam 7: Taxes280 Questions

Exam 8: International Trade261 Questions

Exam 9: Decision Making by Individuals and Firms165 Questions

Exam 10: The Rational Consumer197 Questions

Exam 11: Behind the Supply Curve- Inputs and Costs357 Questions

Exam 12: Perfect Competition and the Supply Curve341 Questions

Exam 13: Monopoly316 Questions

Exam 14: Oligopoly272 Questions

Exam 15: Monopolistic Competition246 Questions

Exam 16: Externalities194 Questions

Exam 17: Public Goods and Common Resources180 Questions

Exam 18: The Economics of the Welfare State125 Questions

Exam 19: Factor Markets and the Distribution of Income317 Questions

Exam 20: Uncertainty, risk, and Private Information150 Questions

Exam 21: Graphs in Economics62 Questions

Exam 22: Consumer Preferences153 Questions

Exam 23: Indifference Curve Analysis41 Questions

Select questions type

In the short run,the fixed costs of running a farm should play no role in determining the level of production.

Free

(True/False)

4.8/5  (28)

(28)

Correct Answer: Verified

Verified

True

Suppose that the market for haircuts in a community is perfectly competitive and that the market is initially in long-run equilibrium.Subsequently,an increase in population increases the demand for haircuts.In the short run,the market price will _____ and the output of a typical firm will _____.

Free

(Multiple Choice)

4.7/5 (32)

Correct Answer:Verified

A

When perfect competition prevails,which characteristic of firms are we likely to observe?

Free

(Multiple Choice)

4.9/5 (38)

Correct Answer:Verified

D

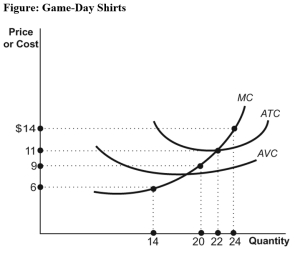

Use the following to answer questions :  -(Figure: Game-Day Shirts)Use Figure: Game-Day Shirts.Rick is one of the 10 vendors who sell Game-Day T-shirts at football games in a perfectly competitive market.His costs are identical to the costs of the other nine vendors.If the price of a shirt is $9,the short-run industry supply will be _____ shirts.

-(Figure: Game-Day Shirts)Use Figure: Game-Day Shirts.Rick is one of the 10 vendors who sell Game-Day T-shirts at football games in a perfectly competitive market.His costs are identical to the costs of the other nine vendors.If the price of a shirt is $9,the short-run industry supply will be _____ shirts.

(Multiple Choice)

4.9/5 (35)

Use the following to answer questions :

Figure: A Perfectly Competitive Firm in the Short Run  -(Figure: A Perfectly Competitive Firm in the Short Run)Use Figure: A Perfectly Competitive Firm in the Short Run.The minimum price that the firm must receive to produce in the short run is:

-(Figure: A Perfectly Competitive Firm in the Short Run)Use Figure: A Perfectly Competitive Firm in the Short Run.The minimum price that the firm must receive to produce in the short run is:

(Multiple Choice)

4.9/5 (35)

The short-run industry supply curve is more elastic than the long-run industry supply curve.

(True/False)

4.8/5 (38)

Use the following to answer questions :

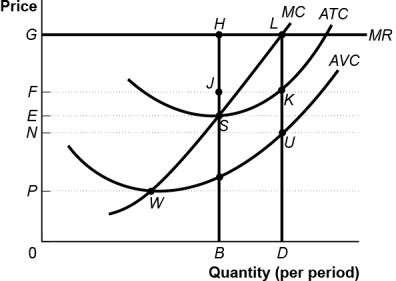

Figure: The Profit Maximizing Firm in the Short Run  -(Figure: The Profit-Maximizing Firm in the Short Run)Use Figure: The Profit-Maximizing Firm in the Short Run.If the market price is less than P2,the firm will _____ in the short run.

-(Figure: The Profit-Maximizing Firm in the Short Run)Use Figure: The Profit-Maximizing Firm in the Short Run.If the market price is less than P2,the firm will _____ in the short run.

(Multiple Choice)

4.8/5 (34)

Use the following to answer questions :

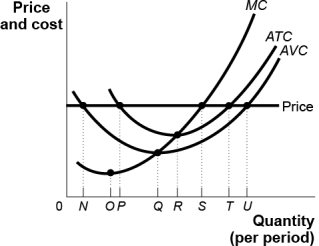

Figure: Short-Run Costs  -(Figure: Short-Run Costs)Use Figure: Short-Run Costs.At the given price,the MOST profitable level of output occurs at quantity:

-(Figure: Short-Run Costs)Use Figure: Short-Run Costs.At the given price,the MOST profitable level of output occurs at quantity:

(Multiple Choice)

4.8/5 (31)

Use the following to answer questions : Table: Variable Costs for Lots Quantity of Lots Variable Costs 0 \ 0 10 200 20 300 30 500 40 750 50 1,100 60 2,100

-(Table: Variable Costs for Lots)Use Table: Variable Costs for Lots.During the winter,Alexa runs a snow-clearing service in a perfectly competitive industry.Assume that costs are constant in each interval;so,for example,the marginal cost of clearing each of the lots from 1 through 10 is $20.Also assume that she can only plow the quantities of the lots given in the table (and not numbers in between).Her only fixed cost is $1 000 for a snowplow.Her variable costs include fuel,her time,and hot coffee.If the price to clear a lot is $60,what is Alexa's profit per unit at the optimal output?

(Multiple Choice)

4.7/5 (27)

A perfectly competitive industry with constant costs initially operates in long-run equilibrium.When demand increases:

(Multiple Choice)

4.8/5 (36)

Use the following to answer questions : Table: Soybean Cost Quantity of Soybeans (bushels) Total Cost (TC) 0 12 1 26 2 33 3 42 4 54 5 69 6 84 7 104

-(Table: Soybean Cost)Use Table: Soybean Cost.What is the shutdown price for this farmer?

(Multiple Choice)

4.8/5 (42)

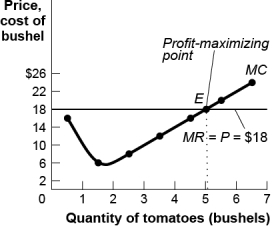

Use the following to answer questions :

Figure: Costs and Profits for Tomato Producers  -(Figure: Costs and Profits for Tomato Producers)Use Figure: Costs and Profits for Tomato Producers.The market for tomatoes is perfectly competitive.The market price of a kilogram of tomatoes is $18.If the market price falls to $16,the farmer's marginal revenue _____ and the profit-maximizing output _____.

-(Figure: Costs and Profits for Tomato Producers)Use Figure: Costs and Profits for Tomato Producers.The market for tomatoes is perfectly competitive.The market price of a kilogram of tomatoes is $18.If the market price falls to $16,the farmer's marginal revenue _____ and the profit-maximizing output _____.

(Multiple Choice)

4.8/5 (38)

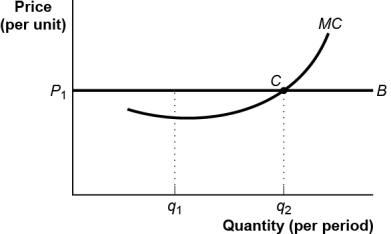

Use the following to answer questions :

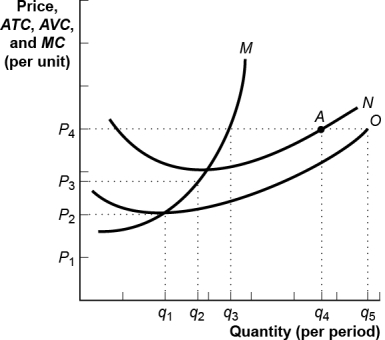

Figure: The Marginal Decision Rule  -(Figure: The Marginal Decision Rule)Use Figure: The Marginal Decision Rule.Given the market price P1,B is the _____ curve.

-(Figure: The Marginal Decision Rule)Use Figure: The Marginal Decision Rule.Given the market price P1,B is the _____ curve.

(Multiple Choice)

4.8/5 (42)

Use the following to answer questions :

Figure: The Profit Maximizing Firm in the Short Run

-(Figure: The Profit-Maximizing Firm in the Short Run)Use Figure: The Profit-Maximizing Firm in the Short Run.Which curve is the AVC curve?

(Multiple Choice)

4.9/5 (39)

Use the following to answer questions :

-(Figure: Game-Day Shirts)Use Figure: Game-Day Shirts.Rick is one of the 10 vendors who sell Game-Day T-shirts at football games in a perfectly competitive market.His costs are identical to the costs of the other nine vendors.If the price of a shirt is $14,the short-run industry supply will be _____ shirts.

(Multiple Choice)

4.8/5 (29)

A firm produces at the output level at which its average total costs are minimized.At this output level,its average total costs are NOT equal to:

(Multiple Choice)

4.8/5 (32)

The short-run supply curve for a perfectly competitive firm is the ____ cost curve above the _____ price.

(Multiple Choice)

4.8/5 (32)

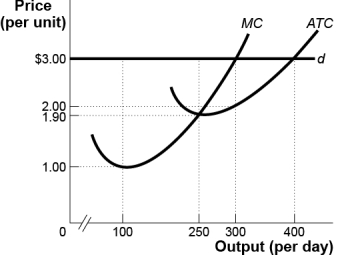

Use the following to answer questions :

Figure: The Perfectly Competitive Firm  -(Figure: The Perfectly Competitive Firm)Use Figure: The Perfectly Competitive Firm.The figure shows a perfectly competitive firm that faces demand curve d and maximizes profit.Given the market price,the firm's total cost per day is:

-(Figure: The Perfectly Competitive Firm)Use Figure: The Perfectly Competitive Firm.The figure shows a perfectly competitive firm that faces demand curve d and maximizes profit.Given the market price,the firm's total cost per day is:

(Multiple Choice)

4.8/5 (28)

Use the following to answer questions : Table: Variable Costs for Lawns Quantity of Lawns Variable Costs 0 \ 0 10 100 20 300 30 500 40 1,100 50 1,800 60 2,900

-(Table: Variable Costs for Lawns)Use Table: Variable Costs for Lawns.During the summer,Alex runs a lawn-mowing service,and lawn-mowing is a perfectly competitive industry.Assume that costs are constant in each interval;so,for example,the marginal cost of mowing each of the lawns from 1 through 10 is $10.Also assume that he can only mow the quantities of lawn given in the table (and not numbers in between).His only fixed cost is $1 000 for the mower.His variable costs include fuel,his time,and mower parts.If the price for mowing a lawn is $60,how much is Alex's profit at the profit-maximizing output?

(Multiple Choice)

4.8/5 (33)

In the long run,firms will leave an industry if the market price is consistently less than their break-even price.

(True/False)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)