Deck 11: Flexible Budgeting and Analysis of Overhead Costs

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Delicious Treats (DT) anticipated that 84,000 process hours would be worked during an upcoming accounting period when, in fact, 92,000 hours were actually worked. One of the company's cost functions is expressed as follows:

Y = $16PH + $640,000 where PH is defined as process hours

What budgeted dollar amount would appear in DT's static budget and flexible budget for the preceding cost function?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Y = $16PH + $640,000 where PH is defined as process hours

What budgeted dollar amount would appear in DT's static budget and flexible budget for the preceding cost function?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Bunnie's Bakery anticipated making 17,000 fancy cakes during a recent period, requiring 14,000 hours of process time. Each hour of process time was expected to cost the firm $11. Actual activity for the period was higher than anticipated: 18,000 cakes and 15,200 hours. If each hour of process time actually cost Bunnie $12, what process-time variance would be disclosed on a performance report that incorporated static budgets and flexible budgets?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

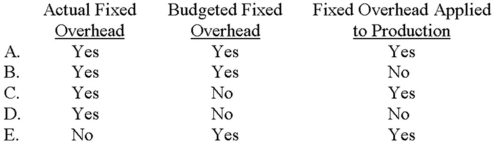

Which of the following is used in the computation of the fixed overhead budget variance?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

Question

Question

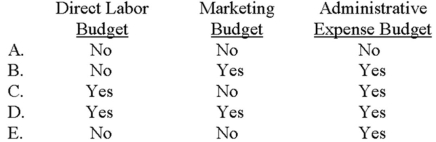

A flexible budget is appropriate for a:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

Question

Question

Question

Question

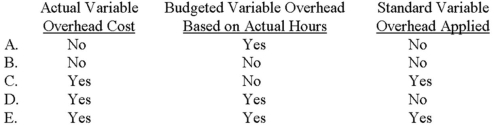

Which of the following is used in the computation of the variable-overhead spending variance?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

A flexible budget is appropriate for a(n):

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

Question

Question

Question

Which of the following variances would be useful to help control overhead spending?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

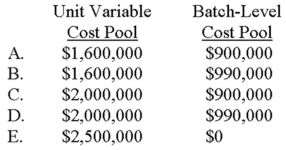

Sand Box Company is choosing new cost drivers for its accounting system. One driver is labor hours; the other is a combination of machine hours for unit variable costs and number of setups for a pool of batch-level costs. Data for the past year follow. Assume that the two separate pools are used. The flexible budget dollar amounts for the actual level of machine hours and actual number of setups are:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

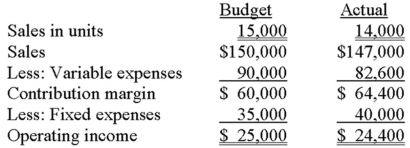

Master Products has the following information for the year just ended:  The company's sales-volume variance is:

The company's sales-volume variance is:

A) $3,000 unfavorable.

B) $4,000 unfavorable.

C) $4,400 favorable.

D) $10,000 unfavorable.

E) $10,000 favorable.

The company's sales-volume variance is:A) $3,000 unfavorable.

B) $4,000 unfavorable.

C) $4,400 favorable.

D) $10,000 unfavorable.

E) $10,000 favorable.

Question

Question

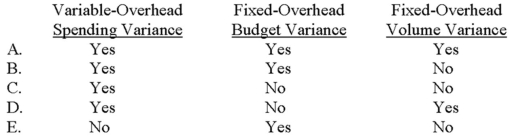

The fixed-overhead budget and volume variances are:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

Sand Box Company is choosing new cost drivers for its accounting system. One driver is labor hours; the other is a combination of machine hours for unit variable costs and number of setups for a pool of batch-level costs. Data for the past year follow. Assume that both cost pools are combined into a single pool, and labor hours is the driver. The total flexible budget for the actual level of labor hours and the total variance for the combined pool are:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

The Marketing Club at Southern University recently held an end-of-year dinner and swim party, which the treasurer declared to be a financial success. "Attendance was an all-time high, 60 members, and the results were much better than expected." The treasurer presented the following performance report at the executive board's June meeting:

The budget was based on the assumptions that follow.

• Forty-five members would attend at a fixed ticket price of $35.

• Food and beverage costs were anticipated to be $15 and $7 per attendee, respectively.

• A disc jockey was hired via a written contract at $50 per hour.

Required:

A. Briefly evaluate the meaningfulness of the treasurer's performance report.

B. Prepare a performance report by using flexible budgeting and determine whether the end-of-year party was as successful as originally reported.

C. Based on your answer in requirement "B," present a possible explanation for the variances in revenue, food costs, beverage costs, and the disc jockey.

The budget was based on the assumptions that follow.

• Forty-five members would attend at a fixed ticket price of $35.

• Food and beverage costs were anticipated to be $15 and $7 per attendee, respectively.

• A disc jockey was hired via a written contract at $50 per hour.

Required:

A. Briefly evaluate the meaningfulness of the treasurer's performance report.

B. Prepare a performance report by using flexible budgeting and determine whether the end-of-year party was as successful as originally reported.

C. Based on your answer in requirement "B," present a possible explanation for the variances in revenue, food costs, beverage costs, and the disc jockey.

Question

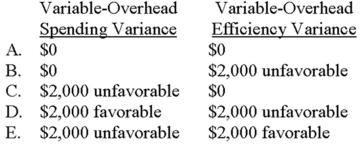

The variable-overhead spending and efficiency variances are:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

Question

Question

Question

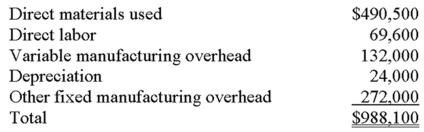

Hempstead Corporation plans to manufacture 8,000 units over the next month at the following costs: direct materials, $480,000; direct labor, $60,000; variable manufacturing overhead, $150,000; straight-line depreciation, $24,000, and other fixed manufacturing overhead, $272,000. The result is total budgeted cost of $990,000.

Shortly after the conclusion of the month, Hempstead reported the following costs:

Howard Krueger and his crews turned out 7,200 units-a remarkable feat given that the company's manufacturing plant was closed for several days because of blizzards and impassable roads. Krueger was especially pleased with the fact that total actual costs were less than budget. He was thus very surprised when Hempstead's general manager expressed unhappiness about the plant's financial performance.

Required:

A. Prepare a performance report that fairly compares budgeted and actual costs for the period just ended-namely, the report that the general manager likely used when assessing performance.

B. Should Krueger be praised for "having met the budget" or is the general manager's unhappiness justified? Explain, citing any apparent problems for the firm.

Shortly after the conclusion of the month, Hempstead reported the following costs:

Howard Krueger and his crews turned out 7,200 units-a remarkable feat given that the company's manufacturing plant was closed for several days because of blizzards and impassable roads. Krueger was especially pleased with the fact that total actual costs were less than budget. He was thus very surprised when Hempstead's general manager expressed unhappiness about the plant's financial performance.

Required:

A. Prepare a performance report that fairly compares budgeted and actual costs for the period just ended-namely, the report that the general manager likely used when assessing performance.

B. Should Krueger be praised for "having met the budget" or is the general manager's unhappiness justified? Explain, citing any apparent problems for the firm.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Master Products has the following information for the year just ended:  The company's sales-price variance is:

The company's sales-price variance is:

A) $3,000 unfavorable.

B) $7,000 unfavorable.

C) $7,000 favorable.

D) $7,500 unfavorable.

E) $7,500 favorable.

The company's sales-price variance is:A) $3,000 unfavorable.

B) $7,000 unfavorable.

C) $7,000 favorable.

D) $7,500 unfavorable.

E) $7,500 favorable.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/91

Play

Full screen (f)

Deck 11: Flexible Budgeting and Analysis of Overhead Costs

1

Gourmet Restaurants has the following flexible-budget formula:

Y = $13PH + $450,000 where PH is defined as process hours.

Which of the following statements is (are) true?

A) Gourmet has $450,000 of fixed costs.

B) Each additional hour of process time is expected to cost Gourmet $13.

C) Y would equal the amount shown as "total cost" in the company's flexible budget.

D) Both Gourmet has $450,000 of fixed costs and each additional hour of process time is expected to cost Gourmet $13.

E) All of the other answers are correct.

Y = $13PH + $450,000 where PH is defined as process hours.

Which of the following statements is (are) true?

A) Gourmet has $450,000 of fixed costs.

B) Each additional hour of process time is expected to cost Gourmet $13.

C) Y would equal the amount shown as "total cost" in the company's flexible budget.

D) Both Gourmet has $450,000 of fixed costs and each additional hour of process time is expected to cost Gourmet $13.

E) All of the other answers are correct.

E

2

Trois Elles Corporation recently prepared a manufacturing cost budget for an output of 50,000 units, as follows: Actual units produced amounted to 60,000. Actual costs incurred were: direct materials, $110,000; direct labor, $60,000; variable overhead, $100,000; and fixed overhead, $97,000. If Trois Elles evaluated performance by the use of a flexible budget, a performance report would reveal a total variance of:

A) $3,000 favorable.

B) $23,000 favorable.

C) $27,000 unfavorable.

D) $42,000 unfavorable.

E) None of the other answers are correct.

A) $3,000 favorable.

B) $23,000 favorable.

C) $27,000 unfavorable.

D) $42,000 unfavorable.

E) None of the other answers are correct.

$3,000 favorable.

3

Efficient or inefficient use of a specific component of variable overhead (e.g., electricity) will cause the firm to have a variable-overhead efficiency variance.

True

4

Young Corporation has a high probability of operating at 40,000 activity hours during the upcoming period, and lower probabilities of operating at 30,000 hours and 50,000 hours. The company's flexible budget revealed the following: If Young operated at 35,000 hours, its total budgeted cost would be:

A) $877,500.

B) $945,000.

C) $787,500.

D) $997,500.

E) $810,000.

A) $877,500.

B) $945,000.

C) $787,500.

D) $997,500.

E) $810,000.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

5

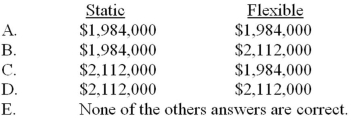

Del's Diner anticipated that 84,000 process hours would be worked during an upcoming accounting period when, in fact, 90,000 hours were actually worked. One of the company's cost functions is expressed as follows:

Y = $16PH + $640,000 where PH is defined as process hours

What is Del's flexible budget (Y) for the preceding cost function?

A) $1,280,000

B) $2,080,000

C) $1,984,000

D) $1,221,000

E) $2,112,000

Y = $16PH + $640,000 where PH is defined as process hours

What is Del's flexible budget (Y) for the preceding cost function?

A) $1,280,000

B) $2,080,000

C) $1,984,000

D) $1,221,000

E) $2,112,000

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

6

Gourmet Restaurants has the following flexible-budget formula:

Y = $13PH + $450,000 where PH is defined as process hours.

What is Gourmet's budgeted total cost if its process hours equal 25,000?

A) $325,000.

B) $450,000.

C) $775,000.

D) $1,225,000.

E) Answer cannot be determined from the information provided.

Y = $13PH + $450,000 where PH is defined as process hours.

What is Gourmet's budgeted total cost if its process hours equal 25,000?

A) $325,000.

B) $450,000.

C) $775,000.

D) $1,225,000.

E) Answer cannot be determined from the information provided.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

7

Flexible budgets reflect a company's anticipated costs based on variations in:

A) activity levels.

B) inflation rates.

C) managers.

D) anticipated capital acquisitions.

E) standards.

A) activity levels.

B) inflation rates.

C) managers.

D) anticipated capital acquisitions.

E) standards.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

8

The budget variance arises from a comparison of actual variable overhead expenditures with budgeted variable overhead costs.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

9

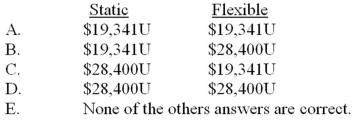

Interspace Merchandising anticipated selling 29,000 units of a major product and paying sales commissions of $6 per unit. Actual sales and sales commissions totaled 31,500 units and $182,700, respectively. If the company used a static budget for performance evaluations, Interstate would report a cost variance of:

A) $6,300U.

B) $6,300F.

C) $8,700U.

D) $8,700F.

E) None of the other answers are correct.

A) $6,300U.

B) $6,300F.

C) $8,700U.

D) $8,700F.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

10

Delicious Treats (DT) anticipated that 84,000 process hours would be worked during an upcoming accounting period when, in fact, 92,000 hours were actually worked. One of the company's cost functions is expressed as follows:

Y = $16PH + $640,000 where PH is defined as process hours

What budgeted dollar amount would appear in DT's static budget and flexible budget for the preceding cost function?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Y = $16PH + $640,000 where PH is defined as process hours

What budgeted dollar amount would appear in DT's static budget and flexible budget for the preceding cost function?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

11

Zin, Inc. is planning its cash needs for an upcoming period when 85,000 machine hours are expected to be worked. Activity may drop as low as 78,000 hours if some overdue equipment maintenance procedures are performed; on the other hand, activity could jump to 94,000 hours if one of Zin's major competitors likely goes bankrupt. A flexible cash budget to determine cash needs would best be based on:

A) 78,000 hours.

B) 85,000 hours.

C) 94,000 hours.

D) 78,000 hours and 94,000 hours.

E) 78,000 hours, 85,000 hours, and 94,000 hours.

A) 78,000 hours.

B) 85,000 hours.

C) 94,000 hours.

D) 78,000 hours and 94,000 hours.

E) 78,000 hours, 85,000 hours, and 94,000 hours.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

12

A flexible budget for 15,000 hours revealed variable manufacturing overhead of $90,000 and fixed manufacturing overhead of $120,000. The budget for 25,000 hours would reveal total overhead costs of $210,000.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

13

Gridiron Merchandising anticipated selling 27,000 units of a major product and paying sales commissions of $6 per unit. Actual sales and sales commissions totaled 27,500 units and $171,400, respectively. If the company used a flexible budget for performance evaluations, Gridiron would report a cost variance of:

A) $6,400U.

B) $6,400F.

C) $9,400U.

D) $9,400F.

E) None of the other answers are correct.

A) $6,400U.

B) $6,400F.

C) $9,400U.

D) $9,400F.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

14

Flexible budgets reflect a company's anticipated costs based on variations in activity levels.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

15

The manufacturing overhead applied to Work-in-Process Inventory by a company that uses standard costing would be computed as actual hours times a predetermined (standard) overhead rate.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

16

A flexible budget:

A) parallels a static budget with respect to format and advantages of use.

B) is preferred over a static budget in the evaluation of performance.

C) gives management flexibility in terms of meeting budget goals.

D) can be used to compare actual and budgeted costs at various levels of activity.

E) is both preferred over a static budget in the evaluation of performance and can be used to compare actual and budgeted costs at various levels of activity.

A) parallels a static budget with respect to format and advantages of use.

B) is preferred over a static budget in the evaluation of performance.

C) gives management flexibility in terms of meeting budget goals.

D) can be used to compare actual and budgeted costs at various levels of activity.

E) is both preferred over a static budget in the evaluation of performance and can be used to compare actual and budgeted costs at various levels of activity.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

17

Young Corporation has a high probability of operating at 40,000 activity hours during the upcoming period, and lower probabilities of operating at 30,000 hours and 50,000 hours. The company's flexible budget revealed the following: Young's flexible-budget formula, where Y is defined as total cost and AH represents activity hours, is:

A) Y = $4.50AH + $24AH.

B) Y = $4.50AH + $720,000.

C) Y = $22.50AH.

D) Y = $180,000 + $18AH.

E) Y = $945,000.

A) Y = $4.50AH + $24AH.

B) Y = $4.50AH + $720,000.

C) Y = $22.50AH.

D) Y = $180,000 + $18AH.

E) Y = $945,000.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following mathematical expressions is found in a typical flexible-budget formula for overhead?

A) Total activity units + budgeted fixed overhead cost per unit.

B) Budgeted variable overhead cost per unit + budgeted fixed overhead cost.

C) (Budgeted variable overhead cost per unit × total activity units) + budgeted fixed overhead costs.

D) (Budgeted fixed overhead cost per unit × total activity units) + (budgeted variable overhead cost per unit × total activity units).

E) None of the other answers are correct.

A) Total activity units + budgeted fixed overhead cost per unit.

B) Budgeted variable overhead cost per unit + budgeted fixed overhead cost.

C) (Budgeted variable overhead cost per unit × total activity units) + budgeted fixed overhead costs.

D) (Budgeted fixed overhead cost per unit × total activity units) + (budgeted variable overhead cost per unit × total activity units).

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

19

A static budget:

A) is based totally on prior year's costs.

B) is based on one anticipated activity level.

C) is based on a range of activity.

D) is preferred over a flexible budget in the evaluation of performance.

E) presents a clear measure of performance when planned activity differs from actual activity.

A) is based totally on prior year's costs.

B) is based on one anticipated activity level.

C) is based on a range of activity.

D) is preferred over a flexible budget in the evaluation of performance.

E) presents a clear measure of performance when planned activity differs from actual activity.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

20

Bunnie's Bakery anticipated making 17,000 fancy cakes during a recent period, requiring 14,000 hours of process time. Each hour of process time was expected to cost the firm $11. Actual activity for the period was higher than anticipated: 18,000 cakes and 15,200 hours. If each hour of process time actually cost Bunnie $12, what process-time variance would be disclosed on a performance report that incorporated static budgets and flexible budgets?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following is used in the computation of the fixed overhead budget variance?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following elements is (are) needed in a straightforward calculation of the variable-overhead spending variance?

A) Variable overhead incurred during the period.

B) Budgeted variable overhead based on actual hours worked.

C) Standard variable overhead applied to production.

D) Both variable overhead incurred during the period and budgeted variable overhead based on actual hours worked.

E) Both variable overhead incurred during the period and standard variable overhead applied to production.

A) Variable overhead incurred during the period.

B) Budgeted variable overhead based on actual hours worked.

C) Standard variable overhead applied to production.

D) Both variable overhead incurred during the period and budgeted variable overhead based on actual hours worked.

E) Both variable overhead incurred during the period and standard variable overhead applied to production.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following is not an overhead variance?

A) Variable-overhead spending variance.

B) Variable-overhead efficiency variance.

C) Fixed-overhead efficiency variance.

D) Fixed-overhead budget variance.

E) Fixed-overhead volume variance.

A) Variable-overhead spending variance.

B) Variable-overhead efficiency variance.

C) Fixed-overhead efficiency variance.

D) Fixed-overhead budget variance.

E) Fixed-overhead volume variance.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

24

A flexible budget is appropriate for a:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following statements is/are correct concerning the application of overhead in a standard costing system driven by process hours?

A) A predetermined overhead rate is allowed only for fixed overhead.

B) Overhead application is based on standard process hours allowed.

C) Overhead application is based on actual process hours incurred.

D) Only prime costs are considered to be product costs in a standard costing system.

E) Only variable overhead costs are applied to production.

A) A predetermined overhead rate is allowed only for fixed overhead.

B) Overhead application is based on standard process hours allowed.

C) Overhead application is based on actual process hours incurred.

D) Only prime costs are considered to be product costs in a standard costing system.

E) Only variable overhead costs are applied to production.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

26

Smithville uses labor hours to apply variable overhead to production. If the company's workers were very inefficient during the period, which of the following statements would be true about the variable-overhead efficiency variance?

A) The variance would be favorable.

B) The variance would be unfavorable.

C) The nature of the variance (favorable or unfavorable) would be unknown based on the facts presented.

D) The variance would be the same amount as the labor efficiency variance.

E) None of the other answers are correct.

A) The variance would be favorable.

B) The variance would be unfavorable.

C) The nature of the variance (favorable or unfavorable) would be unknown based on the facts presented.

D) The variance would be the same amount as the labor efficiency variance.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

27

A flexible budget for 15,000 hours revealed variable manufacturing overhead of $90,000 and fixed manufacturing overhead of $120,000. The budget for 20,000 hours would reveal total overhead costs of:

A) $240,000.

B) $270,000.

C) $290,000.

D) $350,000.

E) $210,000.

A) $240,000.

B) $270,000.

C) $290,000.

D) $350,000.

E) $210,000.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

28

A flexible budget for 15,000 hours revealed variable manufacturing overhead of $90,000 and fixed manufacturing overhead of $120,000. The budget for 25,000 hours would reveal total overhead costs of:

A) $210,000.

B) $270,000.

C) $290,000.

D) $350,000.

E) None of the other answers are correct.

A) $210,000.

B) $270,000.

C) $290,000.

D) $350,000.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following is used in the computation of the variable-overhead spending variance?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

30

A flexible budget is appropriate for a(n):

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

31

The activity measure selected for use in a variable- and fixed-overhead flexible budget:

A) should be stated in sales dollars.

B) should be approved by the company's president.

C) should vary in a similar behavior pattern to the way that variable overhead varies.

D) should remain fixed.

E) should produce the most attractive results for the individual who will use the budget in managerial applications.

A) should be stated in sales dollars.

B) should be approved by the company's president.

C) should vary in a similar behavior pattern to the way that variable overhead varies.

D) should remain fixed.

E) should produce the most attractive results for the individual who will use the budget in managerial applications.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following should have the strongest cause and effect relationship with overhead costs?

A) Cost followers.

B) Non-value-added costs.

C) Cost drivers.

D) Value-added costs.

E) Units of output.

A) Cost followers.

B) Non-value-added costs.

C) Cost drivers.

D) Value-added costs.

E) Units of output.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

33

With respect to overhead, what is the difference between normal costing and standard costing?

A) Use of a predetermined overhead rate.

B) Use of standard hours versus actual hours.

C) Use of a standard rate versus an actual rate.

D) The choice of an activity measure.

E) There is no difference.

A) Use of a predetermined overhead rate.

B) Use of standard hours versus actual hours.

C) Use of a standard rate versus an actual rate.

D) The choice of an activity measure.

E) There is no difference.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following variances would be useful to help control overhead spending?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

35

The difference between the total actual factory overhead and the total factory overhead applied to production is the:

A) sum of the spending, efficiency, budget, and volume variances.

B) controllable variance.

C) efficiency variance.

D) spending variance.

E) volume variance.

A) sum of the spending, efficiency, budget, and volume variances.

B) controllable variance.

C) efficiency variance.

D) spending variance.

E) volume variance.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

36

The budget variance arises from a comparison of:

A) budgeted fixed overhead expenditures with budgeted fixed overhead costs.

B) actual fixed overhead costs with budgeted fixed overhead costs.

C) actual variable overhead expenditures with budgeted variable overhead costs.

D) variable overhead costs with budgeted fixed overhead costs.

E) static-budget amounts with flexible-budget amounts.

A) budgeted fixed overhead expenditures with budgeted fixed overhead costs.

B) actual fixed overhead costs with budgeted fixed overhead costs.

C) actual variable overhead expenditures with budgeted variable overhead costs.

D) variable overhead costs with budgeted fixed overhead costs.

E) static-budget amounts with flexible-budget amounts.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

37

The manufacturing overhead applied to Work-in-Process Inventory by a company that uses standard costing would be computed as:

A) actual hours times a predetermined (standard) overhead rate.

B) standard hours times a predetermined (standard) overhead rate.

C) actual hours times an actual overhead rate.

D) standard hours times an actual overhead rate.

E) $0, because users of standard costing do not apply overhead to work in process.

A) actual hours times a predetermined (standard) overhead rate.

B) standard hours times a predetermined (standard) overhead rate.

C) actual hours times an actual overhead rate.

D) standard hours times an actual overhead rate.

E) $0, because users of standard costing do not apply overhead to work in process.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

38

What will cause the variable-overhead efficiency variance?

A) Efficient or inefficient use of a specific component of variable overhead (e.g., electricity).

B) Full or partial utilization of major equipment resources.

C) Production of units in excess of the number of units sold.

D) Efficient or inefficient use of the cost driver (e.g., machine hours) for variable overhead.

E) Changes in the salary cost of manufacturing supervisors.

A) Efficient or inefficient use of a specific component of variable overhead (e.g., electricity).

B) Full or partial utilization of major equipment resources.

C) Production of units in excess of the number of units sold.

D) Efficient or inefficient use of the cost driver (e.g., machine hours) for variable overhead.

E) Changes in the salary cost of manufacturing supervisors.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

39

Assume that machine hours is the cost driver for overhead. The difference between the actual variable overhead incurred and the applied variable overhead is the:

A) volume variance.

B) production variance.

C) efficiency variance.

D) sum of the spending and efficiency variances.

E) spending variance.

A) volume variance.

B) production variance.

C) efficiency variance.

D) sum of the spending and efficiency variances.

E) spending variance.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following is not an overhead variance?

A) Variable-overhead spending variance.

B) Variable-overhead volume variance.

C) Variable-overhead efficiency variance.

D) Fixed-overhead budget variance.

E) Fixed-overhead volume variance.

A) Variable-overhead spending variance.

B) Variable-overhead volume variance.

C) Variable-overhead efficiency variance.

D) Fixed-overhead budget variance.

E) Fixed-overhead volume variance.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

41

Benson Company, which uses a standard cost system, budgeted $600,000 of fixed overhead when 40,000 machine hours were anticipated. Other data for the period were:

Actual units produced: 10,000

Standard production time per unit: 3.9 machine hours

Fixed overhead incurred: $620,000

Actual machine hours worked: 42,000

Benson's fixed-overhead volume variance is:

A) $10,000 favorable.

B) $15,000 favorable.

C) $15,000 unfavorable.

D) $20,000 favorable.

E) $20,000 unfavorable.

Actual units produced: 10,000

Standard production time per unit: 3.9 machine hours

Fixed overhead incurred: $620,000

Actual machine hours worked: 42,000

Benson's fixed-overhead volume variance is:

A) $10,000 favorable.

B) $15,000 favorable.

C) $15,000 unfavorable.

D) $20,000 favorable.

E) $20,000 unfavorable.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

42

Abbott has a standard variable overhead rate of $4.50 per machine hour, and each unit produced has a standard time allowed of three hours. The company's static budget was based on 46,000 units. Actual results for the year follow.

Actual units produced: 42,000

Actual machine hours worked: 120,000

Actual variable overhead incurred: $520,000

Abbott's variable-overhead efficiency variance is:

A) $20,000 favorable.

B) $20,000 unfavorable.

C) $27,000 favorable.

D) $27,000 unfavorable.

E) None of the other answers are correct.

Actual units produced: 42,000

Actual machine hours worked: 120,000

Actual variable overhead incurred: $520,000

Abbott's variable-overhead efficiency variance is:

A) $20,000 favorable.

B) $20,000 unfavorable.

C) $27,000 favorable.

D) $27,000 unfavorable.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

43

The difference between budgeted fixed manufacturing overhead and the fixed overhead applied to production is the:

A) sum of the spending and efficiency variances.

B) controllable variance.

C) efficiency variance.

D) spending variance.

E) volume variance.

A) sum of the spending and efficiency variances.

B) controllable variance.

C) efficiency variance.

D) spending variance.

E) volume variance.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

44

Abbott has a standard variable overhead rate of $4.50 per machine hour, and each unit produced has a standard time allowed of three hours. The company's static budget was based on 46,000 units. Actual results for the year follow.

Actual units produced: 42,000

Actual machine hours worked: 120,000

Actual variable overhead incurred: $520,000

Abbott's variable-overhead spending variance is:

A) $20,000 favorable.

B) $20,000 unfavorable.

C) $27,000 favorable.

D) $27,000 unfavorable.

E) None of the other answers are correct.

Actual units produced: 42,000

Actual machine hours worked: 120,000

Actual variable overhead incurred: $520,000

Abbott's variable-overhead spending variance is:

A) $20,000 favorable.

B) $20,000 unfavorable.

C) $27,000 favorable.

D) $27,000 unfavorable.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

45

Darling Company, which applies overhead to production on the basis of machine hours, reported the following data for the period just ended:

Actual units produced: 12,000

Actual fixed overhead incurred: $730,000

Actual machine hours worked: 60,000

Budgeted fixed overhead: $720,000

Planned level of machine-hour activity: 50,000

If Darling estimates four hours to manufacture a completed unit, the company's standard fixed overhead rate per machine hour would be:

A) $12.00.

B) $14.40.

C) $14.60.

D) $15.00.

E) None of the other answers are correct.

Actual units produced: 12,000

Actual fixed overhead incurred: $730,000

Actual machine hours worked: 60,000

Budgeted fixed overhead: $720,000

Planned level of machine-hour activity: 50,000

If Darling estimates four hours to manufacture a completed unit, the company's standard fixed overhead rate per machine hour would be:

A) $12.00.

B) $14.40.

C) $14.60.

D) $15.00.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

46

Rich Company, which uses a standard cost system, budgeted $800,000 of fixed overhead when 50,000 machine hours were anticipated. Other data for the period were:

Actual units produced: 10,600

Actual machine hours worked: 51,800

Actual variable overhead incurred: $475,000

Actual fixed overhead incurred: $790,100

Standard variable overhead rate per machine hour: $8.50

Standard production time per unit: 5 hours

Rich's variable-overhead efficiency variance is:

A) $10,200U.

B) $10,200F.

C) $15,300U.

D) $15,300F.

E) None of the other answers are correct.

Actual units produced: 10,600

Actual machine hours worked: 51,800

Actual variable overhead incurred: $475,000

Actual fixed overhead incurred: $790,100

Standard variable overhead rate per machine hour: $8.50

Standard production time per unit: 5 hours

Rich's variable-overhead efficiency variance is:

A) $10,200U.

B) $10,200F.

C) $15,300U.

D) $15,300F.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

47

Enberg Company, which applies overhead to production on the basis of machine hours, reported the following data for the period just ended:

Actual units produced: 14,800

Actual fixed overhead incurred: $791,000

Standard fixed overhead rate: $13 per hour

Budgeted fixed overhead: $780,000

Planned level of machine-hour activity: 60,000

If Enberg estimates four hours to manufacture a completed unit, the company's fixed-overhead volume variance would be:

A) $10,400 favorable.

B) $10,400 unfavorable.

C) $11,000 favorable.

D) $11,000 unfavorable.

E) None of the other answers are correct.

Actual units produced: 14,800

Actual fixed overhead incurred: $791,000

Standard fixed overhead rate: $13 per hour

Budgeted fixed overhead: $780,000

Planned level of machine-hour activity: 60,000

If Enberg estimates four hours to manufacture a completed unit, the company's fixed-overhead volume variance would be:

A) $10,400 favorable.

B) $10,400 unfavorable.

C) $11,000 favorable.

D) $11,000 unfavorable.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

48

Atlanta Enterprises incurred $828,000 of fixed overhead during the period. During that same period, the company applied $845,000 of fixed overhead to production and reported an unfavorable budget variance of $41,000. How much was Atlanta's budgeted fixed overhead?

A) $787,000.

B) $804,000.

C) $869,000.

D) $886,000.

E) Not enough information to judge.

A) $787,000.

B) $804,000.

C) $869,000.

D) $886,000.

E) Not enough information to judge.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

49

Which variance is commonly associated with measuring the cost of under- or over-utilization of plant capacity?

A) The variable-overhead spending variance.

B) The variable-overhead efficiency variance.

C) The fixed-overhead budget variance.

D) The fixed-overhead volume variance.

E) The total fixed-overhead variance.

A) The variable-overhead spending variance.

B) The variable-overhead efficiency variance.

C) The fixed-overhead budget variance.

D) The fixed-overhead volume variance.

E) The total fixed-overhead variance.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

50

Rowe Corporation reported the following variances for the period just ended:

Variable-overhead spending variance: $50,000U

Variable-overhead efficiency variance: $28,000U

Fixed-overhead budget variance: $70,000U

Fixed-overhead volume variance: $30,000U

If Rowe desires to analyze variances that arose primarily from managers' expenditures in excess of anticipated amounts, the company should focus on variances that total:

A) $50,000U.

B) $70,000U.

C) $120,000U.

D) $178,000U.

E) None of the other answers are correct.

Variable-overhead spending variance: $50,000U

Variable-overhead efficiency variance: $28,000U

Fixed-overhead budget variance: $70,000U

Fixed-overhead volume variance: $30,000U

If Rowe desires to analyze variances that arose primarily from managers' expenditures in excess of anticipated amounts, the company should focus on variances that total:

A) $50,000U.

B) $70,000U.

C) $120,000U.

D) $178,000U.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

51

Luke, Inc. has a standard variable overhead rate of $5 per machine hour, with each completed unit expected to take three machine hours to produce. A review of the company's accounting records found the following:

Actual production: 19,500 units

Variable-overhead efficiency variance: $9,000U

Variable-overhead spending variance: $21,000F

What was Luke's actual variable overhead during the period?

A) $262,500.

B) $280,500.

C) $304,500.

D) $322,500.

E) None of the other answers are correct.

Actual production: 19,500 units

Variable-overhead efficiency variance: $9,000U

Variable-overhead spending variance: $21,000F

What was Luke's actual variable overhead during the period?

A) $262,500.

B) $280,500.

C) $304,500.

D) $322,500.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

52

Sussex Company uses a standard cost system and prepared the following budget for May when 24,000 machine hours of activity were anticipated: variable overhead, $48,000; fixed overhead: $240,000. Actual data for May were:

Standard machine hours allowed for output attained: 25,000

Actual machine hours worked: 24,000

Variable overhead incurred: $50,000

Fixed overhead incurred: $250,000

The standard variable overhead rate for May is:

A) $2.00.

B) $2.08.

C) $3.00.

D) $5.00.

E) $5.21.

Standard machine hours allowed for output attained: 25,000

Actual machine hours worked: 24,000

Variable overhead incurred: $50,000

Fixed overhead incurred: $250,000

The standard variable overhead rate for May is:

A) $2.00.

B) $2.08.

C) $3.00.

D) $5.00.

E) $5.21.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

53

A fixed-overhead volume variance would normally arise when:

A) actual hours of activity coincide with actual units of production.

B) budgeted fixed overhead is less than (or greater than) applied fixed overhead.

C) there is a fixed-overhead budget variance.

D) actual fixed overhead exceeds budgeted fixed overhead.

E) there is a variable-overhead efficiency variance.

A) actual hours of activity coincide with actual units of production.

B) budgeted fixed overhead is less than (or greater than) applied fixed overhead.

C) there is a fixed-overhead budget variance.

D) actual fixed overhead exceeds budgeted fixed overhead.

E) there is a variable-overhead efficiency variance.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

54

Rowe Corporation reported the following variances for the period just ended:

Variable-overhead spending variance: $50,000U

Variable-overhead efficiency variance: $28,000U

Fixed-overhead budget variance: $70,000U

Fixed-overhead volume variance: $30,000U

If Rowe prepared an overhead cost performance report, which of these overhead variances is likely to be excluded from the report?

A) Variable-overhead spending variance.

B) Variable-overhead efficiency variance.

C) Fixed-overhead budget variance.

D) Fixed-overhead volume variance.

E) None of the variances would be excluded.

Variable-overhead spending variance: $50,000U

Variable-overhead efficiency variance: $28,000U

Fixed-overhead budget variance: $70,000U

Fixed-overhead volume variance: $30,000U

If Rowe prepared an overhead cost performance report, which of these overhead variances is likely to be excluded from the report?

A) Variable-overhead spending variance.

B) Variable-overhead efficiency variance.

C) Fixed-overhead budget variance.

D) Fixed-overhead volume variance.

E) None of the variances would be excluded.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

55

Robert Company, which applies overhead to production on the basis of machine hours, reported the following data for the period just ended:

Actual units produced: 12,000

Actual variable overhead incurred: $77,700

Actual machine hours worked: 18,800

Standard variable overhead cost per machine hour: $4.50

If Robert estimates 1.5 hours to manufacture a completed unit, the company's variable-overhead spending variance is:

A) $3,600 favorable.

B) $3,600 unfavorable.

C) $6,900 favorable.

D) $6,900 unfavorable.

E) None of the other answers are correct.

Actual units produced: 12,000

Actual variable overhead incurred: $77,700

Actual machine hours worked: 18,800

Standard variable overhead cost per machine hour: $4.50

If Robert estimates 1.5 hours to manufacture a completed unit, the company's variable-overhead spending variance is:

A) $3,600 favorable.

B) $3,600 unfavorable.

C) $6,900 favorable.

D) $6,900 unfavorable.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

56

Martin Company, which applies overhead to production on the basis of machine hours, reported the following data for the period just ended:

Actual units produced: 9,000

Actual variable overhead incurred: $54,400

Actual machine hours worked: 16,000

Standard variable overhead cost per machine hour: $3.50

If Martin estimates two hours to manufacture a completed unit, the company's variable-overhead efficiency variance is:

A) $1,600 favorable.

B) $1,600 unfavorable.

C) $7,000 favorable.

D) $7,000 unfavorable.

E) None of the other answers are correct.

Actual units produced: 9,000

Actual variable overhead incurred: $54,400

Actual machine hours worked: 16,000

Standard variable overhead cost per machine hour: $3.50

If Martin estimates two hours to manufacture a completed unit, the company's variable-overhead efficiency variance is:

A) $1,600 favorable.

B) $1,600 unfavorable.

C) $7,000 favorable.

D) $7,000 unfavorable.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

57

Bushnell, Inc. has a standard variable overhead rate of $4 per machine hour, with each completed unit expected to take three machine hours to produce. A review of the company's accounting records found the following:

Actual variable overhead: $210,000

Variable-overhead efficiency variance: $18,000U

Variable-overhead spending variance: $30,000F

How many units did Bushnell actually produce during the period?

A) 13,500.

B) 16,500.

C) 18,500.

D) 21,500.

E) None of the other answers are correct.

Actual variable overhead: $210,000

Variable-overhead efficiency variance: $18,000U

Variable-overhead spending variance: $30,000F

How many units did Bushnell actually produce during the period?

A) 13,500.

B) 16,500.

C) 18,500.

D) 21,500.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

58

Rich Company, which uses a standard cost system, budgeted $800,000 of fixed overhead when 50,000 machine hours were anticipated. Other data for the period were:

Actual units produced: 10,600

Actual machine hours worked: 51,800

Actual variable overhead incurred: $475,000

Actual fixed overhead incurred: $790,100

Standard variable overhead rate per machine hour: $8.50

Standard production time per unit: 5 hours

Rich's fixed-overhead budget variance is:

A) $9,900U.

B) $9,900F.

C) $28,800U.

D) $28,800F.

E) None of the other answers are correct.

Actual units produced: 10,600

Actual machine hours worked: 51,800

Actual variable overhead incurred: $475,000

Actual fixed overhead incurred: $790,100

Standard variable overhead rate per machine hour: $8.50

Standard production time per unit: 5 hours

Rich's fixed-overhead budget variance is:

A) $9,900U.

B) $9,900F.

C) $28,800U.

D) $28,800F.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

59

Herman Company, which applies overhead to production on the basis of machine hours, reported the following data for the period just ended:

Actual units produced: 13,000

Actual fixed overhead incurred: $742,000

Standard fixed overhead rate: $15 per hour

Budgeted fixed overhead: $720,000

Planned level of machine-hour activity: 48,000

If Herman estimates four hours to manufacture a completed unit, the company's fixed-overhead budget variance would be:

A) $22,000 favorable.

B) $22,000 unfavorable.

C) $60,000 favorable.

D) $60,000 unfavorable.

E) None of the other answers are correct.

Actual units produced: 13,000

Actual fixed overhead incurred: $742,000

Standard fixed overhead rate: $15 per hour

Budgeted fixed overhead: $720,000

Planned level of machine-hour activity: 48,000

If Herman estimates four hours to manufacture a completed unit, the company's fixed-overhead budget variance would be:

A) $22,000 favorable.

B) $22,000 unfavorable.

C) $60,000 favorable.

D) $60,000 unfavorable.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

60

Benson Company, which uses a standard cost system, budgeted $600,000 of fixed overhead when 40,000 machine hours were anticipated. Other data for the period were:

Actual units produced: 10,000

Standard production time per unit: 3.9 machine hours

Fixed overhead incurred: $620,000

Actual machine hours worked: 42,000

Benson's fixed-overhead budget variance is:

A) $10,000 favorable.

B) $15,000 favorable.

C) $15,000 unfavorable.

D) $20,000 favorable.

E) $20,000 unfavorable.

Actual units produced: 10,000

Standard production time per unit: 3.9 machine hours

Fixed overhead incurred: $620,000

Actual machine hours worked: 42,000

Benson's fixed-overhead budget variance is:

A) $10,000 favorable.

B) $15,000 favorable.

C) $15,000 unfavorable.

D) $20,000 favorable.

E) $20,000 unfavorable.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

61

Sand Box Company is choosing new cost drivers for its accounting system. One driver is labor hours; the other is a combination of machine hours for unit variable costs and number of setups for a pool of batch-level costs. Data for the past year follow. Assume that the two separate pools are used. The flexible budget dollar amounts for the actual level of machine hours and actual number of setups are:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

62

Master Products has the following information for the year just ended: The company's sales-volume variance is:

A) $3,000 unfavorable.

B) $4,000 unfavorable.

C) $4,400 favorable.

D) $10,000 unfavorable.

E) $10,000 favorable.

The company's sales-volume variance is:A) $3,000 unfavorable.

B) $4,000 unfavorable.

C) $4,400 favorable.

D) $10,000 unfavorable.

E) $10,000 favorable.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

63

What is the most common treatment of the fixed-overhead budget variance at the end of the accounting period?

A) Reported as a deferred charge or credit.

B) Allocated among Work-in-Process Inventory, Finished-Goods Inventory, and Cost of Goods Sold.

C) Charged or credited to Cost of Goods Sold.

D) Allocated among Cost of Goods Manufactured, Finished-Goods Inventory, and Cost of Goods Sold.

E) Charged or credited to Income Summary.

A) Reported as a deferred charge or credit.

B) Allocated among Work-in-Process Inventory, Finished-Goods Inventory, and Cost of Goods Sold.

C) Charged or credited to Cost of Goods Sold.

D) Allocated among Cost of Goods Manufactured, Finished-Goods Inventory, and Cost of Goods Sold.

E) Charged or credited to Income Summary.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

64

The fixed-overhead budget and volume variances are:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

65

Sand Box Company is choosing new cost drivers for its accounting system. One driver is labor hours; the other is a combination of machine hours for unit variable costs and number of setups for a pool of batch-level costs. Data for the past year follow. Assume that both cost pools are combined into a single pool, and labor hours is the driver. The total flexible budget for the actual level of labor hours and the total variance for the combined pool are:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

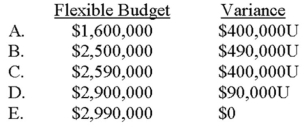

66

The Marketing Club at Southern University recently held an end-of-year dinner and swim party, which the treasurer declared to be a financial success. "Attendance was an all-time high, 60 members, and the results were much better than expected." The treasurer presented the following performance report at the executive board's June meeting:

The budget was based on the assumptions that follow.

• Forty-five members would attend at a fixed ticket price of $35.

• Food and beverage costs were anticipated to be $15 and $7 per attendee, respectively.

• A disc jockey was hired via a written contract at $50 per hour.

Required:

A. Briefly evaluate the meaningfulness of the treasurer's performance report.

B. Prepare a performance report by using flexible budgeting and determine whether the end-of-year party was as successful as originally reported.

C. Based on your answer in requirement "B," present a possible explanation for the variances in revenue, food costs, beverage costs, and the disc jockey.

The budget was based on the assumptions that follow.

• Forty-five members would attend at a fixed ticket price of $35.

• Food and beverage costs were anticipated to be $15 and $7 per attendee, respectively.

• A disc jockey was hired via a written contract at $50 per hour.

Required:

A. Briefly evaluate the meaningfulness of the treasurer's performance report.

B. Prepare a performance report by using flexible budgeting and determine whether the end-of-year party was as successful as originally reported.

C. Based on your answer in requirement "B," present a possible explanation for the variances in revenue, food costs, beverage costs, and the disc jockey.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

67

The variable-overhead spending and efficiency variances are:

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

68

Draco, Inc. has the following overhead standards:

Variable overhead: 4 hours at $8 per hour

Fixed overhead: 4 hours at $10 per hour

The standards were based on a planned activity of 20,000 machine hours when 5,000 units were scheduled for production. Actual data follow.

Variable overhead incurred: $167,750

Fixed overhead incurred: $210,000

Machine hours worked: 19,800

Actual units produced: 5,100

Draco's fixed-overhead budget variance is:

A) $6,000 unfavorable.

B) $7,000 unfavorable.

C) $10,000 unfavorable.

D) $12,000 unfavorable.

E) None of the other answers are correct.

Variable overhead: 4 hours at $8 per hour

Fixed overhead: 4 hours at $10 per hour

The standards were based on a planned activity of 20,000 machine hours when 5,000 units were scheduled for production. Actual data follow.

Variable overhead incurred: $167,750

Fixed overhead incurred: $210,000

Machine hours worked: 19,800

Actual units produced: 5,100

Draco's fixed-overhead budget variance is:

A) $6,000 unfavorable.

B) $7,000 unfavorable.

C) $10,000 unfavorable.

D) $12,000 unfavorable.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

69

The Houston Chamber Orchestra presents a series of concerts throughout the year. Budgeted fixed costs total $300,000 for the concert season; variable costs are expected to average $5 per patron. The orchestra uses flexible budgeting.

Required:

A. Prepare a flexible budget that shows the expected costs of 8,000, 8,500, and 9,000 patrons.

B. Construct the orchestra's flexible budget formula.

C. Assume that 8,700 patrons attended concerts during the year just ended, and actual costs were: variable, $42,000; fixed, $307,500. Evaluate the orchestra's financial performance by computing variances for variable costs and fixed costs.

Required:

A. Prepare a flexible budget that shows the expected costs of 8,000, 8,500, and 9,000 patrons.

B. Construct the orchestra's flexible budget formula.

C. Assume that 8,700 patrons attended concerts during the year just ended, and actual costs were: variable, $42,000; fixed, $307,500. Evaluate the orchestra's financial performance by computing variances for variable costs and fixed costs.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

70

In an effort to reduce record-keeping, companies that sell perishable goods will often enter the standard cost of direct material, direct labor, and manufacturing overhead directly into what account?

A) Work-in-Process Inventory.

B) Finished-Goods Inventory.

C) Cost of Goods Sold.

D) Cost of Goods Manufactured.

E) Sales Revenue.

A) Work-in-Process Inventory.

B) Finished-Goods Inventory.

C) Cost of Goods Sold.

D) Cost of Goods Manufactured.

E) Sales Revenue.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

71

Hempstead Corporation plans to manufacture 8,000 units over the next month at the following costs: direct materials, $480,000; direct labor, $60,000; variable manufacturing overhead, $150,000; straight-line depreciation, $24,000, and other fixed manufacturing overhead, $272,000. The result is total budgeted cost of $990,000.

Shortly after the conclusion of the month, Hempstead reported the following costs:

Howard Krueger and his crews turned out 7,200 units-a remarkable feat given that the company's manufacturing plant was closed for several days because of blizzards and impassable roads. Krueger was especially pleased with the fact that total actual costs were less than budget. He was thus very surprised when Hempstead's general manager expressed unhappiness about the plant's financial performance.

Required:

A. Prepare a performance report that fairly compares budgeted and actual costs for the period just ended-namely, the report that the general manager likely used when assessing performance.

B. Should Krueger be praised for "having met the budget" or is the general manager's unhappiness justified? Explain, citing any apparent problems for the firm.

Shortly after the conclusion of the month, Hempstead reported the following costs:

Howard Krueger and his crews turned out 7,200 units-a remarkable feat given that the company's manufacturing plant was closed for several days because of blizzards and impassable roads. Krueger was especially pleased with the fact that total actual costs were less than budget. He was thus very surprised when Hempstead's general manager expressed unhappiness about the plant's financial performance.

Required:

A. Prepare a performance report that fairly compares budgeted and actual costs for the period just ended-namely, the report that the general manager likely used when assessing performance.

B. Should Krueger be praised for "having met the budget" or is the general manager's unhappiness justified? Explain, citing any apparent problems for the firm.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

72

Draco, Inc. has the following overhead standards:

Variable overhead: 4 hours at $8 per hour

Fixed overhead: 4 hours at $10 per hour

The standards were based on a planned activity of 20,000 machine hours when 5,000 units were scheduled for production. Actual data follow.

Variable overhead incurred: $167,750

Fixed overhead incurred: $210,000

Machine hours worked: 19,800

Actual units produced: 5,100

Draco's variable-overhead efficiency variance is:

A) $550 favorable.

B) $550 unfavorable.

C) $4,800 favorable.

D) $4,800 unfavorable.

E) None of the other answers are correct.

Variable overhead: 4 hours at $8 per hour

Fixed overhead: 4 hours at $10 per hour

The standards were based on a planned activity of 20,000 machine hours when 5,000 units were scheduled for production. Actual data follow.

Variable overhead incurred: $167,750

Fixed overhead incurred: $210,000

Machine hours worked: 19,800

Actual units produced: 5,100

Draco's variable-overhead efficiency variance is:

A) $550 favorable.

B) $550 unfavorable.

C) $4,800 favorable.

D) $4,800 unfavorable.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

73

The sales-volume variance equals:

A) (actual sales volume - budgeted sales volume) × actual sales price.

B) (actual sales volume - budgeted sales volume) × actual contribution margin.

C) (actual sales volume - budgeted sales volume) × budgeted sales price.

D) (actual sales price - budgeted sales price) × budgeted sales volume.

E) (actual sales price - budgeted sales price) × fixed-overhead volume variance.

A) (actual sales volume - budgeted sales volume) × actual sales price.

B) (actual sales volume - budgeted sales volume) × actual contribution margin.

C) (actual sales volume - budgeted sales volume) × budgeted sales price.

D) (actual sales price - budgeted sales price) × budgeted sales volume.

E) (actual sales price - budgeted sales price) × fixed-overhead volume variance.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

74

Draco, Inc. has the following overhead standards:

Variable overhead: 4 hours at $8 per hour

Fixed overhead: 4 hours at $10 per hour

The standards were based on a planned activity of 20,000 machine hours when 5,000 units were scheduled for production. Actual data follow.

Variable overhead incurred: $167,750

Fixed overhead incurred: $210,000

Machine hours worked: 19,800

Actual units produced: 5,100

Draco's variable-overhead spending variance is:

A) $550 favorable.

B) $4,550 unfavorable.

C) $4,800 favorable.

D) $9,350 unfavorable.

E) None of the other answers are correct.

Variable overhead: 4 hours at $8 per hour

Fixed overhead: 4 hours at $10 per hour

The standards were based on a planned activity of 20,000 machine hours when 5,000 units were scheduled for production. Actual data follow.

Variable overhead incurred: $167,750

Fixed overhead incurred: $210,000

Machine hours worked: 19,800

Actual units produced: 5,100

Draco's variable-overhead spending variance is:

A) $550 favorable.

B) $4,550 unfavorable.

C) $4,800 favorable.

D) $9,350 unfavorable.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

75

Riskless Insurance uses budgets to forecast and monitor overhead throughout the organization. The following budget formula relates to the processing of applications for automobile policies in any given month:

Total overhead = $6.80APH + $13,500

where APH = application processing hours

The typical automobile insurance policy has an estimated processing time of 1.5 hours.

During June, management originally anticipated that 320 applications would be processed. Activity was lower than expected, with only 280 applications completed by month-end, and the following costs were incurred: variable overhead, $2,950; fixed overhead, $13,700.

Required:

A. What volume level of applications and processing hours would have been used if Sitka had constructed a static budget?

B. Construct a flexible budget that shows the expected monthly variable and fixed overhead costs of processing 270, 300, and 330 applications.

C. From a cost perspective, did the company perform better or worse than anticipated in June? Show calculations to support your answer.

Total overhead = $6.80APH + $13,500

where APH = application processing hours

The typical automobile insurance policy has an estimated processing time of 1.5 hours.

During June, management originally anticipated that 320 applications would be processed. Activity was lower than expected, with only 280 applications completed by month-end, and the following costs were incurred: variable overhead, $2,950; fixed overhead, $13,700.

Required:

A. What volume level of applications and processing hours would have been used if Sitka had constructed a static budget?

B. Construct a flexible budget that shows the expected monthly variable and fixed overhead costs of processing 270, 300, and 330 applications.

C. From a cost perspective, did the company perform better or worse than anticipated in June? Show calculations to support your answer.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

76

When actual variable cost per unit equals standard variable cost per unit, the difference between actual and budgeted contribution margin is explained by a combination of which two variances?

A) The sales-volume variance and the fixed-overhead volume variance.

B) The sales-volume variance and the fixed-overhead budget variance.

C) The sales-price variance and the fixed-overhead volume variance.

D) The sales-price variance and sales-volume variance.

E) The sales-price variance and fixed-overhead budget variance.

A) The sales-volume variance and the fixed-overhead volume variance.

B) The sales-volume variance and the fixed-overhead budget variance.

C) The sales-price variance and the fixed-overhead volume variance.

D) The sales-price variance and sales-volume variance.

E) The sales-price variance and fixed-overhead budget variance.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

77

Draco, Inc. has the following overhead standards:

Variable overhead: 4 hours at $8 per hour

Fixed overhead: 4 hours at $10 per hour

The standards were based on a planned activity of 20,000 machine hours when 5,000 units were scheduled for production. Actual data follow.

Variable overhead incurred: $167,750

Fixed overhead incurred: $210,000

Machine hours worked: 19,800

Actual units produced: 5,100

The amount of variable overhead that Draco applied to production is:

A) $158,400.

B) $160,000.

C) $163,200.

D) $167,750.

E) None of the other answers are correct.

Variable overhead: 4 hours at $8 per hour

Fixed overhead: 4 hours at $10 per hour

The standards were based on a planned activity of 20,000 machine hours when 5,000 units were scheduled for production. Actual data follow.

Variable overhead incurred: $167,750

Fixed overhead incurred: $210,000

Machine hours worked: 19,800

Actual units produced: 5,100

The amount of variable overhead that Draco applied to production is:

A) $158,400.

B) $160,000.

C) $163,200.

D) $167,750.

E) None of the other answers are correct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

78

Draco, Inc. has the following overhead standards:

Variable overhead: 4 hours at $8 per hour

Fixed overhead: 4 hours at $10 per hour

The standards were based on a planned activity of 20,000 machine hours when 5,000 units were scheduled for production. Actual data follow.

Variable overhead incurred: $167,750

Fixed overhead incurred: $210,000

Machine hours worked: 19,800

Actual units produced: 5,100

Draco's fixed-overhead volume variance is:

A) $4,000 favorable.

B) $4,000 unfavorable.

C) $10,000 favorable.

D) $10,000 unfavorable.

E) None of the other answers are correct.

Variable overhead: 4 hours at $8 per hour

Fixed overhead: 4 hours at $10 per hour

The standards were based on a planned activity of 20,000 machine hours when 5,000 units were scheduled for production. Actual data follow.

Variable overhead incurred: $167,750

Fixed overhead incurred: $210,000

Machine hours worked: 19,800

Actual units produced: 5,100

Draco's fixed-overhead volume variance is: