Exam 11: Flexible Budgeting and Analysis of Overhead Costs

Exam 1: The Changing Role of Managerial Accounting in a Dynamic Business Environment62 Questions

Exam 2: Basic Cost Management Concepts85 Questions

Exam 3: Product Costing and Cost Accumulation in a Batch Production Environment80 Questions

Exam 4: Process Costing and Hybrid Product-Costing Systems84 Questions

Exam 5: Activity-Based Costing and Management85 Questions

Exam 6: Activity Analysis, Cost Behavior, and Cost Estimation93 Questions

Exam 7: Cost-Volume-Profit Analysis89 Questions

Exam 8: Variable Costing and the Costs of Quality and Sustainability64 Questions

Exam 9: Financial Planning and Analysis: the Master Budget95 Questions

Exam 10: Standard Costing and Analysis of Direct Costs80 Questions

Exam 11: Flexible Budgeting and Analysis of Overhead Costs91 Questions

Exam 12: Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard72 Questions

Exam 13: Investment Centers and Transfer Pricing95 Questions

Exam 14: Decision Making: Relevant Costs and Benefits90 Questions

Exam 15: Target Costing and Cost Analysis for Pricing Decisions99 Questions

Exam 16: Capital Expenditure Decisions104 Questions

Exam 17: Allocation of Support Activity Costs and Joint Costs81 Questions

Exam 18: The Sarbanes-Oxley Act, Internal Controls, and Management Accounting14 Questions

Exam 19: Compound Interest and the Concept of Present Value24 Questions

Exam 20: Inventory Management14 Questions

Select questions type

The manufacturing overhead applied to Work-in-Process Inventory by a company that uses standard costing would be computed as actual hours times a predetermined (standard) overhead rate.

Free

(True/False)

4.8/5  (35)

(35)

Correct Answer: Verified

Verified

False

A flexible budget for 15,000 hours revealed variable manufacturing overhead of $90,000 and fixed manufacturing overhead of $120,000. The budget for 25,000 hours would reveal total overhead costs of:

Free

(Multiple Choice)

4.8/5 (37)

Correct Answer:Verified

B

Abbott has a standard variable overhead rate of $4.50 per machine hour, and each unit produced has a standard time allowed of three hours. The company's static budget was based on 46,000 units. Actual results for the year follow.

Actual units produced: 42,000

Actual machine hours worked: 120,000

Actual variable overhead incurred: $520,000

Abbott's variable-overhead efficiency variance is:

Free

(Multiple Choice)

4.8/5 (35)

Correct Answer:Verified

C

Enberg Company, which applies overhead to production on the basis of machine hours, reported the following data for the period just ended:

Actual units produced: 14,800

Actual fixed overhead incurred: $791,000

Standard fixed overhead rate: $13 per hour

Budgeted fixed overhead: $780,000

Planned level of machine-hour activity: 60,000

If Enberg estimates four hours to manufacture a completed unit, the company's fixed-overhead volume variance would be:

(Multiple Choice)

4.8/5 (38)

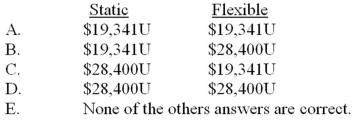

Young Corporation has a high probability of operating at 40,000 activity hours during the upcoming period, and lower probabilities of operating at 30,000 hours and 50,000 hours. The company's flexible budget revealed the following: Variable costs \ 135,000 \ 180,000 \ 225,000 Fixed costs 720,000 720,000 720,000 If Young operated at 35,000 hours, its total budgeted cost would be:

(Multiple Choice)

4.8/5 (33)

Bunnie's Bakery anticipated making 17,000 fancy cakes during a recent period, requiring 14,000 hours of process time. Each hour of process time was expected to cost the firm $11. Actual activity for the period was higher than anticipated: 18,000 cakes and 15,200 hours. If each hour of process time actually cost Bunnie $12, what process-time variance would be disclosed on a performance report that incorporated static budgets and flexible budgets?

(Multiple Choice)

4.8/5 (32)

Rich Company, which uses a standard cost system, budgeted $800,000 of fixed overhead when 50,000 machine hours were anticipated. Other data for the period were:

Actual units produced: 10,600

Actual machine hours worked: 51,800

Actual variable overhead incurred: $475,000

Actual fixed overhead incurred: $790,100

Standard variable overhead rate per machine hour: $8.50

Standard production time per unit: 5 hours

Rich's variable-overhead efficiency variance is:

(Multiple Choice)

4.8/5 (46)

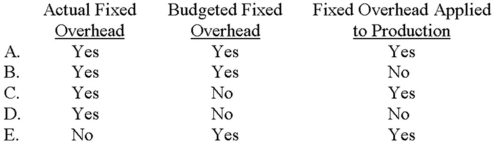

Which of the following is used in the computation of the fixed overhead budget variance?

(Multiple Choice)

4.9/5 (31)

When actual variable cost per unit equals standard variable cost per unit, the difference between actual and budgeted contribution margin is explained by a combination of which two variances?

(Multiple Choice)

4.8/5 (35)

Which variance is commonly associated with measuring the cost of under- or over-utilization of plant capacity?

(Multiple Choice)

4.9/5 (37)

Assume that machine hours is the cost driver for overhead. The difference between the actual variable overhead incurred and the applied variable overhead is the:

(Multiple Choice)

4.8/5 (30)

Luke, Inc. has a standard variable overhead rate of $5 per machine hour, with each completed unit expected to take three machine hours to produce. A review of the company's accounting records found the following:

Actual production: 19,500 units

Variable-overhead efficiency variance: $9,000U

Variable-overhead spending variance: $21,000F

What was Luke's actual variable overhead during the period?

(Multiple Choice)

4.9/5 (41)

Rowe Corporation reported the following variances for the period just ended:

Variable-overhead spending variance: $50,000U

Variable-overhead efficiency variance: $28,000U

Fixed-overhead budget variance: $70,000U

Fixed-overhead volume variance: $30,000U

If Rowe prepared an overhead cost performance report, which of these overhead variances is likely to be excluded from the report?

(Multiple Choice)

4.8/5 (46)

The following information relates to Joplin Company for the period just ended: Standard variable overhead rate per hour \ 1 Standard fixed-overhead rate per hour \ 2 Planned monthly activity 40,000 machine hours Actual production completed 82,000 units Standard machine processing time Two units per hour Actual variable overhead \ 37,000 Actual total overhead \ 121,000 Actual machine hours worked 40,500

All of the company's overhead is variable or fixed in nature.

Required:

A. Calculate the spending and efficiency variances for variable overhead.

B. Calculate the budget and volume variances for fixed overhead.

(Essay)

4.8/5 (42)

Young Corporation has a high probability of operating at 40,000 activity hours during the upcoming period, and lower probabilities of operating at 30,000 hours and 50,000 hours. The company's flexible budget revealed the following: Variable costs \ 135,000 \ 180,000 \ 225,000 Fixed costs 720,000 720,000 720,000 Young's flexible-budget formula, where Y is defined as total cost and AH represents activity hours, is:

(Multiple Choice)

4.9/5 (38)

Draco, Inc. has the following overhead standards:

Variable overhead: 4 hours at $8 per hour

Fixed overhead: 4 hours at $10 per hour

The standards were based on a planned activity of 20,000 machine hours when 5,000 units were scheduled for production. Actual data follow.

Variable overhead incurred: $167,750

Fixed overhead incurred: $210,000

Machine hours worked: 19,800

Actual units produced: 5,100

The amount of variable overhead that Draco applied to production is:

(Multiple Choice)

5.0/5 (42)

Efficient or inefficient use of a specific component of variable overhead (e.g., electricity) will cause the firm to have a variable-overhead efficiency variance.

(True/False)

4.9/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)