Deck 12: Standard Costs: Direct Labor and Materials

Full screen (f)

Question

Question

Basic Price and Quantity Variances for Labor and Materials

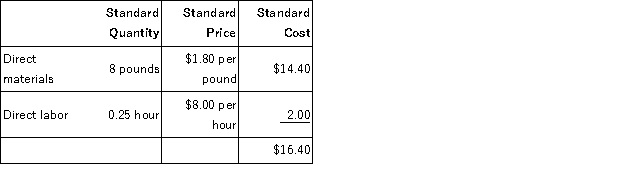

Arrow Industries employs a standard cost system in which direct materials inventory is carried at standard cost. Arrow has established the following standards for the direct costs of one unit of product. During May, Arrow purchased 160,000 pounds of direct materials at a total cost of $304,000. The total factory wages for May were $42,000, 90 percent of which were for direct labor. Arrow manufactured 19,000 units of product during May using 142,500 pounds of direct material and 5,000 direct labor hours.

During May, Arrow purchased 160,000 pounds of direct materials at a total cost of $304,000. The total factory wages for May were $42,000, 90 percent of which were for direct labor. Arrow manufactured 19,000 units of product during May using 142,500 pounds of direct material and 5,000 direct labor hours.

Required:

a. Calculate the direct materials price variance for May.

b. Calculate the direct materials quantity variance for May.

c. Calculate the direct labor wage rate variance for May.

d. Calculate the direct labor efficiency variance for May.

Arrow Industries employs a standard cost system in which direct materials inventory is carried at standard cost. Arrow has established the following standards for the direct costs of one unit of product.

During May, Arrow purchased 160,000 pounds of direct materials at a total cost of $304,000. The total factory wages for May were $42,000, 90 percent of which were for direct labor. Arrow manufactured 19,000 units of product during May using 142,500 pounds of direct material and 5,000 direct labor hours.Required:

a. Calculate the direct materials price variance for May.

b. Calculate the direct materials quantity variance for May.

c. Calculate the direct labor wage rate variance for May.

d. Calculate the direct labor efficiency variance for May.

Question

Question

Question

Question

Question

Question

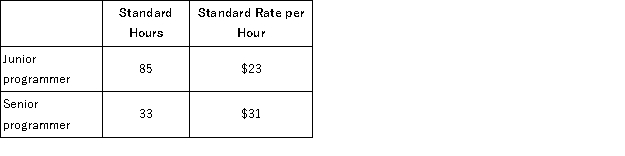

Labor Variances

Hospital Software sells and installs computer software used by hospitals for patient admissions and billing. Every sale requires that Hospital Services modify its proprietary software for the specific demands of the client. Prior to each installation, Hospital Software estimates the number of hours of programming time each job will require and the cost of the programmers. Programmers record the amount of time they spend on each modification, and variance reports are prepared at the end of each installation.

For the Denver General Hospital account, Hospital Software estimates the following labor standards: After the job was completed, the following costs were reported:

After the job was completed, the following costs were reported:  Required:

Required:

Calculate the labor efficiency and labor wage rate variances for the junior and senior programmers on the Denver General Hospital account.

Compute the actual wage rates given the actual hours and actual cost:

Hospital Software sells and installs computer software used by hospitals for patient admissions and billing. Every sale requires that Hospital Services modify its proprietary software for the specific demands of the client. Prior to each installation, Hospital Software estimates the number of hours of programming time each job will require and the cost of the programmers. Programmers record the amount of time they spend on each modification, and variance reports are prepared at the end of each installation.

For the Denver General Hospital account, Hospital Software estimates the following labor standards:

After the job was completed, the following costs were reported: Required:Calculate the labor efficiency and labor wage rate variances for the junior and senior programmers on the Denver General Hospital account.

Compute the actual wage rates given the actual hours and actual cost:

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

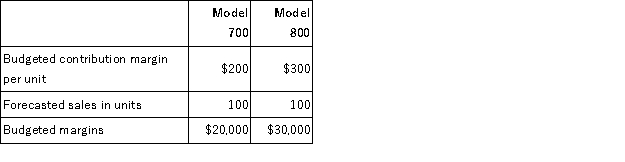

Adapting Variance Analysis to a Marketing Department

Sue Young sells fax machines for Express Fax. There are two fax machines: model 700 and model 800. At the beginning of the month, Sue's sales budget is as follows: At the end of the month, the number of units sold and the actual contribution margins are as follows:

At the end of the month, the number of units sold and the actual contribution margins are as follows:  Contribution margins have changed during the month because the fax machines are imported and foreign exchange rates have changed.

Contribution margins have changed during the month because the fax machines are imported and foreign exchange rates have changed.

Required:

Design a performance evaluation report that analyzes Sue Young's performance for the month.

Sue Young sells fax machines for Express Fax. There are two fax machines: model 700 and model 800. At the beginning of the month, Sue's sales budget is as follows:

At the end of the month, the number of units sold and the actual contribution margins are as follows: Contribution margins have changed during the month because the fax machines are imported and foreign exchange rates have changed.Required:

Design a performance evaluation report that analyzes Sue Young's performance for the month.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/22

Play

Full screen (f)

Deck 12: Standard Costs: Direct Labor and Materials

1

Establishing a Standard Cost System

The Tipy Canoe Company makes fiberglass canoes. The fiberglass resin is initially molded to the shape of a canoe, then sanded and painted. Metal or wooden seats and frames are added for stability. The Tipy Canoe Company was started several years ago in the owner's garage. The owner, Jeff George, did a lot of the initial manual labor with the help of a few friends. The company has since expanded into a large warehouse and new employees have been hired. Because of the expansion, Jeff is no longer directly involved with production and is concerned about his ability to plan for and control the company. He is considering the implementation of a standard cost system.

Required:

a. Describe the procedures Jeff should use in setting standards for direct labor and direct materials.

b. Describe how Jeff could use standards for planning purposes.

c. Describe how Jeff could use standards for motivating employees and problems in using standards as performance measures.

d. Why are some of Jeff's friends who worked with from the beginning not very excited about a change to a standard cost system?

The Tipy Canoe Company makes fiberglass canoes. The fiberglass resin is initially molded to the shape of a canoe, then sanded and painted. Metal or wooden seats and frames are added for stability. The Tipy Canoe Company was started several years ago in the owner's garage. The owner, Jeff George, did a lot of the initial manual labor with the help of a few friends. The company has since expanded into a large warehouse and new employees have been hired. Because of the expansion, Jeff is no longer directly involved with production and is concerned about his ability to plan for and control the company. He is considering the implementation of a standard cost system.

Required:

a. Describe the procedures Jeff should use in setting standards for direct labor and direct materials.

b. Describe how Jeff could use standards for planning purposes.

c. Describe how Jeff could use standards for motivating employees and problems in using standards as performance measures.

d. Why are some of Jeff's friends who worked with from the beginning not very excited about a change to a standard cost system?

a. Direct material standards should be established for the fiberglass resin and the wood and metal for the seats and the frame. For planning purposes, the standards for quantity and price should reflect expectations, but Jeff is no longer familiar with production and must ask some employees about expected quantities and prices. The purchasing manager has information on prices and the manufacturing manager has information on quantities. The direct labor standards are based on expectations from the personnel manager and the manufacturing manager.

b. If accurate estimates of prices and quantities are provided, Jeff can use the information to plan for cash flows. Also, the standards can be used to plan for appropriate inventory levels given planned manufacturing efforts.

c. The standards can be used as benchmarks to evaluate the performance of employees. A problem with using standards as performance measures is the difficulty of obtaining accurate standards from the individuals being evaluated. Standards can also provide incentives to increase inventories, discourage cooperative behavior, and lead to satisficing behavior.

d. Some of Jeff's friends who are still working in the expanded organization will probably be unhappy with the standard costing system because they will no longer be judged directly by their friend Jeff, but through standards that appear impersonal and lacking in trust. Jeff's friends, however, must recognize that Jeff can no longer directly observe what is happening in the company. Standard costing systems are not established because of a lack of trust. Standard costing systems are used to convey information among the different members of the organization.

b. If accurate estimates of prices and quantities are provided, Jeff can use the information to plan for cash flows. Also, the standards can be used to plan for appropriate inventory levels given planned manufacturing efforts.

c. The standards can be used as benchmarks to evaluate the performance of employees. A problem with using standards as performance measures is the difficulty of obtaining accurate standards from the individuals being evaluated. Standards can also provide incentives to increase inventories, discourage cooperative behavior, and lead to satisficing behavior.

d. Some of Jeff's friends who are still working in the expanded organization will probably be unhappy with the standard costing system because they will no longer be judged directly by their friend Jeff, but through standards that appear impersonal and lacking in trust. Jeff's friends, however, must recognize that Jeff can no longer directly observe what is happening in the company. Standard costing systems are not established because of a lack of trust. Standard costing systems are used to convey information among the different members of the organization.

2

Basic Price and Quantity Variances for Labor and Materials

Arrow Industries employs a standard cost system in which direct materials inventory is carried at standard cost. Arrow has established the following standards for the direct costs of one unit of product. During May, Arrow purchased 160,000 pounds of direct materials at a total cost of $304,000. The total factory wages for May were $42,000, 90 percent of which were for direct labor. Arrow manufactured 19,000 units of product during May using 142,500 pounds of direct material and 5,000 direct labor hours.

Required:

a. Calculate the direct materials price variance for May.

b. Calculate the direct materials quantity variance for May.

c. Calculate the direct labor wage rate variance for May.

d. Calculate the direct labor efficiency variance for May.

Arrow Industries employs a standard cost system in which direct materials inventory is carried at standard cost. Arrow has established the following standards for the direct costs of one unit of product.

During May, Arrow purchased 160,000 pounds of direct materials at a total cost of $304,000. The total factory wages for May were $42,000, 90 percent of which were for direct labor. Arrow manufactured 19,000 units of product during May using 142,500 pounds of direct material and 5,000 direct labor hours.Required:

a. Calculate the direct materials price variance for May.

b. Calculate the direct materials quantity variance for May.

c. Calculate the direct labor wage rate variance for May.

d. Calculate the direct labor efficiency variance for May.

a. $16,000 unfavorable ($304,000/160,000 - $1.80) × 160,000

b. $17,100 favorable (142,500 - 19,000 × 8) × $1.80

c. $2,200 favorable ($42,000 × .9 ÷ 5,000 - $8) × 5,000

d. $2,000 unfavorable (5,000 - 19,000 × .25) × $8

Notice that 17,500 pounds of material are still in inventory (160,000 pounds less 142,500). These are being carried at standard cost of $1.80 per pound. Thus, the inventory value at standard cost is $31,500 ($1.80 × 17,500).

b. $17,100 favorable (142,500 - 19,000 × 8) × $1.80

c. $2,200 favorable ($42,000 × .9 ÷ 5,000 - $8) × 5,000

d. $2,000 unfavorable (5,000 - 19,000 × .25) × $8

Notice that 17,500 pounds of material are still in inventory (160,000 pounds less 142,500). These are being carried at standard cost of $1.80 per pound. Thus, the inventory value at standard cost is $31,500 ($1.80 × 17,500).

3

Developing Standards

Cold Queen Company is a small producer of fruit-flavored frozen desserts. For many years, Cold Queen's products have had strong regional sales on the basis of brand recognition; however, other companies have begun marketing similar products in the area, and price competition has become increasingly important. John Wakefield, the company's controller, is planning to implement a standard cost system for Cold Queen and has gathered considerable information from his co-workers on production and materials requirements for Cold Queen's products. Wakefield believes that the use of standard costing will allow Cold Queen to improve cost control and make better pricing decisions.

Cold Queen's most popular product is raspberry sherbet. The sherbet is produced in 10-gallon batches, and each batch requires six quarts of good raspberries. The fresh raspberries are sorted by hand before entering the production process. Because of imperfections in the raspberries and normal spoilage, one quart of berries is discarded for every four quarts of acceptable berries. Three minutes is the standard direct labor time for sorting to obtain one quart of acceptable raspberries. The acceptable raspberries are then blended with the other ingredients; blending requires 12 minutes of direct labor time per batch. After blending, the sherbet is packaged in quart containers. Wakefield has gathered the following pricing information:

• Cold Queen purchases raspberries at a cost of $0.80 per quart. All other ingredients cost a total of $4.50 per 10-gallon batch.

• Direct labor is paid at the rate of $9.00 per hour.

• The total cost of material and labor required to package the sherbet is $0.38 per quart.

Required:

a. Develop the standard cost for the direct cost components of a 10-gallon batch of raspberry sherbet. For each direct cost component of a batch of raspberry sherbet, the standard cost should identify the

(i) Standard quantity.

(ii) Standard rate.

(iii) Standard cost per batch.

b. As part of the implementation of a standard cost system at Cold Queen, John Wakefield plans to train those responsible for maintaining the standards in the use of variance analysis. Wakefield is particularly concerned with the causes of unfavorable variances.

(i) Discuss the possible causes of unfavorable materials price variances and identify the individual(s) who should be held responsible for them.

(ii) Discuss the possible causes of unfavorable labor efficiency variances and identify the individual(s) who should be held responsible for them.

Cold Queen Company is a small producer of fruit-flavored frozen desserts. For many years, Cold Queen's products have had strong regional sales on the basis of brand recognition; however, other companies have begun marketing similar products in the area, and price competition has become increasingly important. John Wakefield, the company's controller, is planning to implement a standard cost system for Cold Queen and has gathered considerable information from his co-workers on production and materials requirements for Cold Queen's products. Wakefield believes that the use of standard costing will allow Cold Queen to improve cost control and make better pricing decisions.

Cold Queen's most popular product is raspberry sherbet. The sherbet is produced in 10-gallon batches, and each batch requires six quarts of good raspberries. The fresh raspberries are sorted by hand before entering the production process. Because of imperfections in the raspberries and normal spoilage, one quart of berries is discarded for every four quarts of acceptable berries. Three minutes is the standard direct labor time for sorting to obtain one quart of acceptable raspberries. The acceptable raspberries are then blended with the other ingredients; blending requires 12 minutes of direct labor time per batch. After blending, the sherbet is packaged in quart containers. Wakefield has gathered the following pricing information:

• Cold Queen purchases raspberries at a cost of $0.80 per quart. All other ingredients cost a total of $4.50 per 10-gallon batch.

• Direct labor is paid at the rate of $9.00 per hour.

• The total cost of material and labor required to package the sherbet is $0.38 per quart.

Required:

a. Develop the standard cost for the direct cost components of a 10-gallon batch of raspberry sherbet. For each direct cost component of a batch of raspberry sherbet, the standard cost should identify the

(i) Standard quantity.

(ii) Standard rate.

(iii) Standard cost per batch.

b. As part of the implementation of a standard cost system at Cold Queen, John Wakefield plans to train those responsible for maintaining the standards in the use of variance analysis. Wakefield is particularly concerned with the causes of unfavorable variances.

(i) Discuss the possible causes of unfavorable materials price variances and identify the individual(s) who should be held responsible for them.

(ii) Discuss the possible causes of unfavorable labor efficiency variances and identify the individual(s) who should be held responsible for them.

a. Standard cost for ten-gallon batch of raspberry sherbet.

quarts quarts required to obtain 6 acceptable quarts.

quarts per gallon gallons quarts b. (i) In general, the purchasing manager is held responsible for material price variances. Causes of these variances include the following:

• Failure to correctly forecast price increases.

• Purchasing nonstandard or uneconomical lots.

• Purchasing from suppliers other than those offering the most favorable terms.

(ii) In general, the production manager or supervisor is held responsible for labor efficiency variances. Causes of these variances include the following:

• Poorly trained labor.

• Substandard or inefficient equipment.

• Inadequate supervision.

• Purchasing substandard raspberries.

quarts quarts required to obtain 6 acceptable quarts.

quarts per gallon gallons quarts b. (i) In general, the purchasing manager is held responsible for material price variances. Causes of these variances include the following:

• Failure to correctly forecast price increases.

• Purchasing nonstandard or uneconomical lots.

• Purchasing from suppliers other than those offering the most favorable terms.

(ii) In general, the production manager or supervisor is held responsible for labor efficiency variances. Causes of these variances include the following:

• Poorly trained labor.

• Substandard or inefficient equipment.

• Inadequate supervision.

• Purchasing substandard raspberries.

4

Assignment of Decision Rights for Setting Standards

Attendant Media Graphics (AMG) is a rapidly expanding company involved in the mass reproduction of instructional materials. AMG is organized into a number of production departments, each of which is responsible for a particular stage of the production process, such as copyediting, typesetting, printing, and binding. An engineering department provides technical assistance to the various production units. Ralph Davis, owner and manager of AMG, has made a concentrated effort to provide a quality product at a competitive price with delivery on the promised due date. Expanding sales have been attributed to this philosophy. Davis is finding it increasingly difficult to personally supervise the operations of AMG and is beginning to institute an organizational structure that would facilitate management control.

One change recently made was the designation of operating departments as cost centers, with control over departmental operations transferred from Davis to each departmental manager. However, quality control still reports directly to Davis, as do the finance and accounting functions. A materials manager was hired to purchase all raw materials and to oversee the inventory handling (receiving, storage, etc.) and record-keeping functions. The materials manager is also responsible for maintaining an adequate inventory based upon planned production levels.

The loss of personal control over the operations of AMG caused Davis to look for a method of efficiently evaluating performance. Dave Cress, a new cost accountant, proposed the use of a standard cost system. Variances for materials and labor could then be calculated and reported directly to Davis.

Required:

a. Assume that AMG is going to implement a standard cost system and establish standards for materials, labor, and manufacturing overhead. For each of these cost components, identify and discuss.

(i) Who should be involved in setting the standards?

(ii) The factors that should be considered in establishing the standards.

b. Describe the basis for assignment of responsibility under a standard cost system.

Attendant Media Graphics (AMG) is a rapidly expanding company involved in the mass reproduction of instructional materials. AMG is organized into a number of production departments, each of which is responsible for a particular stage of the production process, such as copyediting, typesetting, printing, and binding. An engineering department provides technical assistance to the various production units. Ralph Davis, owner and manager of AMG, has made a concentrated effort to provide a quality product at a competitive price with delivery on the promised due date. Expanding sales have been attributed to this philosophy. Davis is finding it increasingly difficult to personally supervise the operations of AMG and is beginning to institute an organizational structure that would facilitate management control.

One change recently made was the designation of operating departments as cost centers, with control over departmental operations transferred from Davis to each departmental manager. However, quality control still reports directly to Davis, as do the finance and accounting functions. A materials manager was hired to purchase all raw materials and to oversee the inventory handling (receiving, storage, etc.) and record-keeping functions. The materials manager is also responsible for maintaining an adequate inventory based upon planned production levels.

The loss of personal control over the operations of AMG caused Davis to look for a method of efficiently evaluating performance. Dave Cress, a new cost accountant, proposed the use of a standard cost system. Variances for materials and labor could then be calculated and reported directly to Davis.

Required:

a. Assume that AMG is going to implement a standard cost system and establish standards for materials, labor, and manufacturing overhead. For each of these cost components, identify and discuss.

(i) Who should be involved in setting the standards?

(ii) The factors that should be considered in establishing the standards.

b. Describe the basis for assignment of responsibility under a standard cost system.

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

5

Standard costs embody targets. The targets should:

A)be very easy to achieve so everyone gets rewarded

B)reflect ideal performance so the company can measure efficiency losses

C)be used to evaluate performance and assign blame

D)reflect a particular management team's goals

E)none of the above

A)be very easy to achieve so everyone gets rewarded

B)reflect ideal performance so the company can measure efficiency losses

C)be used to evaluate performance and assign blame

D)reflect a particular management team's goals

E)none of the above

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

6

Fegox Firinghi (FF) produces flip flops. Each flip-flop requires 2 lbs of Flub and 1 lb of Fleeb, which are planned to cost $8 and $3 per lb. respectively. During the month of May, FF purchased 22,000 lbs of Flub for $194,000 and 13,000 lbs of Fleeb for $42,000. All materials were consumed in producing 10,500 good flip flops. Which is true?

A)Direct materials price variances total $21,000 unfav

B)Direct material price variances total $6,950 unfav

C)The standard price of Flub should be revised

D)The standard price of Flub should not be revised

E)a) and c) only

A)Direct materials price variances total $21,000 unfav

B)Direct material price variances total $6,950 unfav

C)The standard price of Flub should be revised

D)The standard price of Flub should not be revised

E)a) and c) only

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

7

Barb Bubbletop (BB) produces bangles. Each bangle requires .25 lbs of bronze which should cost $16 per lb. In August, BB purchased 12,000 lbs of bronze at $15 per lb. In the month, 41,000 bangles were made, and 11,000 lbs of bronze were used. Which is false of BB's materials variances?

A)The company should have spent $164,000 on materials

B)Bronze inventory increased by $15,000

C)Material quantity variance is $18,000 unfav

D)Materials price variance is $12,000 unfav

E)All of the above are false

A)The company should have spent $164,000 on materials

B)Bronze inventory increased by $15,000

C)Material quantity variance is $18,000 unfav

D)Materials price variance is $12,000 unfav

E)All of the above are false

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

8

Labor Variances

Hospital Software sells and installs computer software used by hospitals for patient admissions and billing. Every sale requires that Hospital Services modify its proprietary software for the specific demands of the client. Prior to each installation, Hospital Software estimates the number of hours of programming time each job will require and the cost of the programmers. Programmers record the amount of time they spend on each modification, and variance reports are prepared at the end of each installation.

For the Denver General Hospital account, Hospital Software estimates the following labor standards: After the job was completed, the following costs were reported: Required:

Calculate the labor efficiency and labor wage rate variances for the junior and senior programmers on the Denver General Hospital account.

Compute the actual wage rates given the actual hours and actual cost:

Hospital Software sells and installs computer software used by hospitals for patient admissions and billing. Every sale requires that Hospital Services modify its proprietary software for the specific demands of the client. Prior to each installation, Hospital Software estimates the number of hours of programming time each job will require and the cost of the programmers. Programmers record the amount of time they spend on each modification, and variance reports are prepared at the end of each installation.

For the Denver General Hospital account, Hospital Software estimates the following labor standards:

After the job was completed, the following costs were reported: Required:Calculate the labor efficiency and labor wage rate variances for the junior and senior programmers on the Denver General Hospital account.

Compute the actual wage rates given the actual hours and actual cost:

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

9

What is the typical treatment of large year-end balances in the variance accounts?

A)Recalculate all standard costs, and adjust to the actual basis for external financial reporting purposes

B)Close to cost of goods of sold

C)Prorate the direct material and labor variances across cost of goods sold, work in process and finished goods inventories

D)Prorate the variances across the raw materials, work in process, and finished goods inventories

E)b and c above

A)Recalculate all standard costs, and adjust to the actual basis for external financial reporting purposes

B)Close to cost of goods of sold

C)Prorate the direct material and labor variances across cost of goods sold, work in process and finished goods inventories

D)Prorate the variances across the raw materials, work in process, and finished goods inventories

E)b and c above

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

10

Differences between Lean Manufacturing and Standard Costing

Lean Manufacturing and standard cost accounting systems are not necessarily substitutes. However, very few firms use both lean manufacturing and standard costs. In fact, some management consultants who advocate lean manufacturing argue that firms should abandon their standard cost systems.

Required:

a. Concisely describe lean manufacturing.

b. Concisely describe standard costing.

c. Why do so few firms use both lean manufacturing and standard costing together?

Lean Manufacturing and standard cost accounting systems are not necessarily substitutes. However, very few firms use both lean manufacturing and standard costs. In fact, some management consultants who advocate lean manufacturing argue that firms should abandon their standard cost systems.

Required:

a. Concisely describe lean manufacturing.

b. Concisely describe standard costing.

c. Why do so few firms use both lean manufacturing and standard costing together?

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

11

A review of skilled engineering labor rates and variances at Kumisomo Industries revealed the following: Actual wage per hour was ¥15,000, as opposed to ¥13,000 planned. Actual labor hours per unit produced were 1.2 compared with 1.4 hours planned. If during a period 1,000 units were produced, which of the following is false?

A)The DL wage rate variance is unfavorable.

B)The DL wage rate variance is ¥2,400 favorable

C)The DL efficiency variance is ¥26,000 favorable

D)The DL efficiency variance may be random

E)None of the above is false

A)The DL wage rate variance is unfavorable.

B)The DL wage rate variance is ¥2,400 favorable

C)The DL efficiency variance is ¥26,000 favorable

D)The DL efficiency variance may be random

E)None of the above is false

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

12

Materials Quantity Variance: Solving for Actual Quantity

Toddca planned to produce 3,000 units of its single product, Terrgam, during November. The standard specifications for one unit of Terrgam include six pounds of material at $0.30 per pound. Actual production in November was 3,100 units of Terrgam. The accountant computed a favorable materials purchase price variance of $380 and an unfavorable materials quantity variance of $120.

Required:

Based on these data, calculate how many pounds of material were used in the production of Terrgam during November.

Toddca planned to produce 3,000 units of its single product, Terrgam, during November. The standard specifications for one unit of Terrgam include six pounds of material at $0.30 per pound. Actual production in November was 3,100 units of Terrgam. The accountant computed a favorable materials purchase price variance of $380 and an unfavorable materials quantity variance of $120.

Required:

Based on these data, calculate how many pounds of material were used in the production of Terrgam during November.

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

13

When variances are used as an input to the performance evaluation system, which of the following scenarios may be encountered?

A)Purchasing managers may buy too much inventory to get a bulk purchase discount

B)Purchasing managers may buy lower quality materials to generate a favorable price variance

C)If standards are set at easily achievable levels, some people will only do enough to meet the target, but no more

D)When labor efficiency is measured on a team or production cell basis, the free rider may take advantage

E)All of the above

A)Purchasing managers may buy too much inventory to get a bulk purchase discount

B)Purchasing managers may buy lower quality materials to generate a favorable price variance

C)If standards are set at easily achievable levels, some people will only do enough to meet the target, but no more

D)When labor efficiency is measured on a team or production cell basis, the free rider may take advantage

E)All of the above

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

14

Fantastic Diapers made 3,000 batches this month. According to the plan, each batch needs 45 minutes of direct labor, which is paid $12.50 per hour, including benefits. Payroll records showed that 2,100 labor hours were worked and that 50 cents more per hour was paid. Which is true?

A)The direct labor rate variance is $1,050 fav

B)The direct labor rate variance is $1,125 unfav

C)The direct labor efficiency variance is $1,875 fav

D)The direct labor efficiency variance is $1,875 unfav

E)None of the above

A)The direct labor rate variance is $1,050 fav

B)The direct labor rate variance is $1,125 unfav

C)The direct labor efficiency variance is $1,875 fav

D)The direct labor efficiency variance is $1,875 unfav

E)None of the above

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

15

Ultimate U-bolts (UU) paid $161,175 for direct labor this month, paying $1.50 cents less per hour than planned. Fifty-four thousand pounds of bolts were produced and direct labor was paid for 9,210 hours. Producing one pound takes ten minutes. Which is true?

A)The direct labor rate variance is $4,605 unfav

B)The direct labor rate variance is $4,605 fav

C)The direct labor rate variance is $4,500 fav

D)The labor operating efficiency is 102%

E)None of the above

A)The direct labor rate variance is $4,605 unfav

B)The direct labor rate variance is $4,605 fav

C)The direct labor rate variance is $4,500 fav

D)The labor operating efficiency is 102%

E)None of the above

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

16

Standard costs:

A)represent the actual amount spent

B)are standard prices

C)are often set based on inputs by engineers

D)are never changed

E)none of the above

A)represent the actual amount spent

B)are standard prices

C)are often set based on inputs by engineers

D)are never changed

E)none of the above

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

17

Standard Labor Variances

A CPA firm estimates that an audit will require the following work: The actual hours and costs were: Required:

Calculate the direct labor, wage rate, and labor efficiency variances for each type of auditor and interpret.

A CPA firm estimates that an audit will require the following work: The actual hours and costs were: Required:

Calculate the direct labor, wage rate, and labor efficiency variances for each type of auditor and interpret.

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

18

Fegox Firinghi (FF) produces flip flops. Each flip-flop requires 2 lbs of Flub and 1 lb of Fleeb, which are planned to cost $8 and $3 per lb. respectively. During the month of May, FF purchased 22,000 lbs of Flub for $194,000 and 13,000 lbs of Fleeb for $42,000. All materials were consumed in producing 10,500 good flip flops. Which is true?

A)The direct material quantity variances total $21,000 fav

B)FF was very efficient in using raw materials to produce their output

C)Direct material quantity variances total $15,500 fav

D)Direct materials quantity variances total $15,500 unfav

E)All of the above are false

A)The direct material quantity variances total $21,000 fav

B)FF was very efficient in using raw materials to produce their output

C)Direct material quantity variances total $15,500 fav

D)Direct materials quantity variances total $15,500 unfav

E)All of the above are false

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

19

Continuing Ultimate U-bolts above. Which is true?

A)The workers were efficient because UU saved $825 overall

B)The workers were efficient because they used 210 fewer hours than allowed

C)The direct labor efficiency variance is $3,780 U

D)The direct labor efficiency variance cannot be calculated from the information provided

E)None of the above

A)The workers were efficient because UU saved $825 overall

B)The workers were efficient because they used 210 fewer hours than allowed

C)The direct labor efficiency variance is $3,780 U

D)The direct labor efficiency variance cannot be calculated from the information provided

E)None of the above

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

20

Expected, Standard, and Actual Labor Hours

The Pizza Company makes two types of frozen pizzas: pepperoni and cheese. The Pizza Company allocates overhead to these two products based on the number of direct labor hours. The direct labor hours per unit for making a pepperoni pizza is 5 minutes or 1/12 of an hour. The direct labor hours per unit for making a cheese pizza is 4 minutes or 1/15 of an hour. At the start of the year the Pizza Company expected to make 12,000 pepperoni pizzas and 6,000 cheese pizzas. During the year, the Pizza Company actually made 9,000 pepperoni pizzas and 7,500 cheese pizzas. The time cards indicate that direct laborers worked for 1,300 hours. What are the total expected direct labor hours, standard direct labor hours, and actual direct labor hours?

The Pizza Company makes two types of frozen pizzas: pepperoni and cheese. The Pizza Company allocates overhead to these two products based on the number of direct labor hours. The direct labor hours per unit for making a pepperoni pizza is 5 minutes or 1/12 of an hour. The direct labor hours per unit for making a cheese pizza is 4 minutes or 1/15 of an hour. At the start of the year the Pizza Company expected to make 12,000 pepperoni pizzas and 6,000 cheese pizzas. During the year, the Pizza Company actually made 9,000 pepperoni pizzas and 7,500 cheese pizzas. The time cards indicate that direct laborers worked for 1,300 hours. What are the total expected direct labor hours, standard direct labor hours, and actual direct labor hours?

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

21

Direct Labor Variances

Moran Health Care is a large hospital system outside Chicago that offers both hospital (inpatient) and clinic (outpatient) services. It has a centralized admissions office that admits and registers clients, some of whom are seeking inpatient hospital services and others outpatient services. Moran uses a standard cost system to control its labor costs. The standard labor time to admit an inpatient is 15 minutes. Outpatient admissions have a standard labor time of 9 minutes. The standard wage rate for admissions agents is $14.50 per hour. During the last week, the admissions office admitted 820 inpatients and 2,210 out-patients. Actual hours worked by the admissions agents last week were 540 hours, and their total wages paid were $8,235.

Required:

a. Prepare a financial report that summarizes the operating performance (including the efficiency) of the admissions office for last week.

b. Based on the financial report you prepared in (a), write a short memo summarizing your findings and conclusions from this report.

Moran Health Care is a large hospital system outside Chicago that offers both hospital (inpatient) and clinic (outpatient) services. It has a centralized admissions office that admits and registers clients, some of whom are seeking inpatient hospital services and others outpatient services. Moran uses a standard cost system to control its labor costs. The standard labor time to admit an inpatient is 15 minutes. Outpatient admissions have a standard labor time of 9 minutes. The standard wage rate for admissions agents is $14.50 per hour. During the last week, the admissions office admitted 820 inpatients and 2,210 out-patients. Actual hours worked by the admissions agents last week were 540 hours, and their total wages paid were $8,235.

Required:

a. Prepare a financial report that summarizes the operating performance (including the efficiency) of the admissions office for last week.

b. Based on the financial report you prepared in (a), write a short memo summarizing your findings and conclusions from this report.

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

22

Adapting Variance Analysis to a Marketing Department

Sue Young sells fax machines for Express Fax. There are two fax machines: model 700 and model 800. At the beginning of the month, Sue's sales budget is as follows: At the end of the month, the number of units sold and the actual contribution margins are as follows: Contribution margins have changed during the month because the fax machines are imported and foreign exchange rates have changed.

Required:

Design a performance evaluation report that analyzes Sue Young's performance for the month.

Sue Young sells fax machines for Express Fax. There are two fax machines: model 700 and model 800. At the beginning of the month, Sue's sales budget is as follows:

At the end of the month, the number of units sold and the actual contribution margins are as follows: Contribution margins have changed during the month because the fax machines are imported and foreign exchange rates have changed.Required:

Design a performance evaluation report that analyzes Sue Young's performance for the month.

Unlock Deck

Unlock for access to all 22 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 22 flashcards in this deck.