Deck 24: Multiperiod Binomial Heath Jarrow Morton Model

Full screen (f)

Question

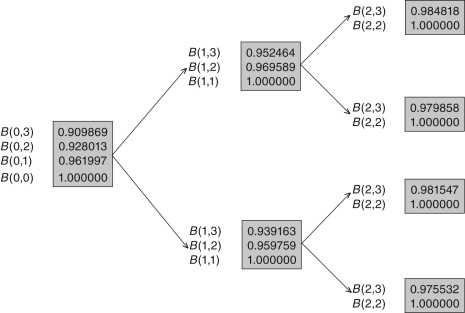

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

Consider a Eurodollar futures with maturity date 2.What is the Eurodollar futures rate on this contract at time 0?

A) 0.019941

B) 0.036619

C) 0.039505

D) 0.019963

E) 0.017755

Consider a Eurodollar futures with maturity date 2.What is the Eurodollar futures rate on this contract at time 0?

A) 0.019941

B) 0.036619

C) 0.039505

D) 0.019963

E) 0.017755

Question

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

Consider a floorlet with maturity time 1 and strike price 0.035.What is the time 0 value of the floorlet?

A) 0.000000

B) 0.003525

C) 0.003198

D) 0.001696

E) 0.001763

Consider a floorlet with maturity time 1 and strike price 0.035.What is the time 0 value of the floorlet?

A) 0.000000

B) 0.003525

C) 0.003198

D) 0.001696

E) 0.001763

Question

What is the value of the money market account in the up and down nodes at time 1?

A) 1.046815,1.032195

B) 1.044801,1.034208

C) 1.039505,1.039505

D) 1.045130,1.038726

E) 1.031364,1.041928

Question

Question

Question

What are the spot rates R(1)in the up and down nodes at time 1?

A) 0.046815,0.032195

B) 0.044801,0.034208

C) 0.039505,0.039505

D) 0.045130,0.038726

E) 0.031364,0.041928

Question

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

-Consider a caplet with maturity time 1 and strike price 0.035.What are the holdings in the three-period bond and money market account at time 0 that replicate the caplet's time 1 payoffs in both the up and down nodes?

A) -0.499864,0.458009

B) 0.265009,-0.239428

C) 0.003198,0.001696

D) 0.000000,0.006640

E) 0.003525,0.000000

-Consider a caplet with maturity time 1 and strike price 0.035.What are the holdings in the three-period bond and money market account at time 0 that replicate the caplet's time 1 payoffs in both the up and down nodes?

A) -0.499864,0.458009

B) 0.265009,-0.239428

C) 0.003198,0.001696

D) 0.000000,0.006640

E) 0.003525,0.000000

Question

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

Consider a caplet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

A) 0.000000,0.006649

B) 0.003525,0.000000

C) 0.003198,0.001696

D) 0.000000,0.003325

E) 0.001763,0.000000

Consider a caplet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

A) 0.000000,0.006649

B) 0.003525,0.000000

C) 0.003198,0.001696

D) 0.000000,0.003325

E) 0.001763,0.000000

Question

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

Consider a forward rate agreement (FRA)with maturity date 2.What is the FRA rate on this contract at time 0?

A) 0.019941

B) 0.036619

C) 0.039505

D) 0.019963

E) 0.017755

Consider a forward rate agreement (FRA)with maturity date 2.What is the FRA rate on this contract at time 0?

A) 0.019941

B) 0.036619

C) 0.039505

D) 0.019963

E) 0.017755

Question

Question

Question

Question

What are the up and down dollar returns on the three-period zero-coupon bond at time 0?

A) 1.046815,1.032195

B) 1.044801,1.034208

C) 1.039505,1.039505

D) 1.045130,1.038726

E) 1.031364,1.041928

Question

Question

Question

What are the up and down dollar returns on the two-period zero-coupon bond at time 0?

A) 1.046815,1.032195

B) 1.044801,1.034208

C) 1.039505,1.039505

D) 1.045130,1.038726

E) 1.031364,1.041928

Question

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

Consider a caplet with maturity time 1 and strike price 0.035.What is the time 0 value of the caplet?

A) 0.000000

B) 0.003525

C) 0.003198

D) 0.000000

E) 0.001763

Consider a caplet with maturity time 1 and strike price 0.035.What is the time 0 value of the caplet?

A) 0.000000

B) 0.003525

C) 0.003198

D) 0.000000

E) 0.001763

Question

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

Consider a floorlet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

A) 0.000000,0.006649

B) 0.003525,0.000000

C) 0.003198,0.001696

D) 0.000000,0.003325

E) 0.001763,0.000000

Consider a floorlet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

A) 0.000000,0.006649

B) 0.003525,0.000000

C) 0.003198,0.001696

D) 0.000000,0.003325

E) 0.001763,0.000000

Question

Question

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

-Consider a floorlet with maturity time 1 and strike price 0.035.What are the holdings in the three-period bond and money market account at time 0 that replicate the floorlet's time 1 payoffs in both the up and down nodes?

A) -0.499864,0.458009

B) 0.265009,-0.239428

C) 0.003198,0.001696

D) 0.000000,0.006640

E) 0.003525,0.000000

-Consider a floorlet with maturity time 1 and strike price 0.035.What are the holdings in the three-period bond and money market account at time 0 that replicate the floorlet's time 1 payoffs in both the up and down nodes?

A) -0.499864,0.458009

B) 0.265009,-0.239428

C) 0.003198,0.001696

D) 0.000000,0.006640

E) 0.003525,0.000000

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/20

Play

Full screen (f)

Deck 24: Multiperiod Binomial Heath Jarrow Morton Model

1

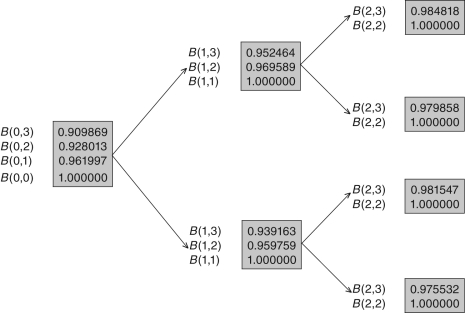

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

Consider a Eurodollar futures with maturity date 2.What is the Eurodollar futures rate on this contract at time 0?

A) 0.019941

B) 0.036619

C) 0.039505

D) 0.019963

E) 0.017755

Consider a Eurodollar futures with maturity date 2.What is the Eurodollar futures rate on this contract at time 0?

A) 0.019941

B) 0.036619

C) 0.039505

D) 0.019963

E) 0.017755

D

2

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

Consider a floorlet with maturity time 1 and strike price 0.035.What is the time 0 value of the floorlet?

A) 0.000000

B) 0.003525

C) 0.003198

D) 0.001696

E) 0.001763

Consider a floorlet with maturity time 1 and strike price 0.035.What is the time 0 value of the floorlet?

A) 0.000000

B) 0.003525

C) 0.003198

D) 0.001696

E) 0.001763

D

3

What is the value of the money market account in the up and down nodes at time 1?

A) 1.046815,1.032195

B) 1.044801,1.034208

C) 1.039505,1.039505

D) 1.045130,1.038726

E) 1.031364,1.041928

C

4

Which of the following statements is INCORRECT?

A) The single-period Heath-Jarrow-Morton (HJM)model is useful as a teaching tool and cannot be used to get realistic option values.

B) The single-period HJM model can be used to illustrate key ideas underlying the pricing and hedging methodology.

C) Interest rate derivatives like American options,futures contracts,and swaptions need at least two periods to capture their complexity.

D) Interest rate derivatives like American options,futures contracts,and swaptions need at least three periods to capture their complexity.

E) The term structure evolution underlying a properly specified binomial model becomes realistic when the time between periods is small and the number of periods is large.

A) The single-period Heath-Jarrow-Morton (HJM)model is useful as a teaching tool and cannot be used to get realistic option values.

B) The single-period HJM model can be used to illustrate key ideas underlying the pricing and hedging methodology.

C) Interest rate derivatives like American options,futures contracts,and swaptions need at least two periods to capture their complexity.

D) Interest rate derivatives like American options,futures contracts,and swaptions need at least three periods to capture their complexity.

E) The term structure evolution underlying a properly specified binomial model becomes realistic when the time between periods is small and the number of periods is large.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

5

A necessary and sufficient condition to rule out arbitrage profits in the multiperiod binomial tree is that the following must hold:

A) "up factor down factor dollar return"

B) "up factor dollar return down factor"

C) the pseudo-probability for an up movement must equal that for the down movement

D) the pseudo-probabilities for an up movement at any node of the tree must be the same for all bond/money market account pairs

E) None of these answers are correct.

A) "up factor down factor dollar return"

B) "up factor dollar return down factor"

C) the pseudo-probability for an up movement must equal that for the down movement

D) the pseudo-probabilities for an up movement at any node of the tree must be the same for all bond/money market account pairs

E) None of these answers are correct.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

6

What are the spot rates R(1)in the up and down nodes at time 1?

A) 0.046815,0.032195

B) 0.044801,0.034208

C) 0.039505,0.039505

D) 0.045130,0.038726

E) 0.031364,0.041928

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

7

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

-Consider a caplet with maturity time 1 and strike price 0.035.What are the holdings in the three-period bond and money market account at time 0 that replicate the caplet's time 1 payoffs in both the up and down nodes?

A) -0.499864,0.458009

B) 0.265009,-0.239428

C) 0.003198,0.001696

D) 0.000000,0.006640

E) 0.003525,0.000000

-Consider a caplet with maturity time 1 and strike price 0.035.What are the holdings in the three-period bond and money market account at time 0 that replicate the caplet's time 1 payoffs in both the up and down nodes?

A) -0.499864,0.458009

B) 0.265009,-0.239428

C) 0.003198,0.001696

D) 0.000000,0.006640

E) 0.003525,0.000000

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

8

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

Consider a caplet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

A) 0.000000,0.006649

B) 0.003525,0.000000

C) 0.003198,0.001696

D) 0.000000,0.003325

E) 0.001763,0.000000

Consider a caplet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

A) 0.000000,0.006649

B) 0.003525,0.000000

C) 0.003198,0.001696

D) 0.000000,0.003325

E) 0.001763,0.000000

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

9

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

Consider a forward rate agreement (FRA)with maturity date 2.What is the FRA rate on this contract at time 0?

A) 0.019941

B) 0.036619

C) 0.039505

D) 0.019963

E) 0.017755

Consider a forward rate agreement (FRA)with maturity date 2.What is the FRA rate on this contract at time 0?

A) 0.019941

B) 0.036619

C) 0.039505

D) 0.019963

E) 0.017755

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

10

Identify the INCORRECT statement.If we try to fit the following derivatives in a single-period framework,then:

A) an American call option becomes a European call option

B) an American put option becomes a digital put option

C) a futures contract simplifies to a forward contract

D) a swaption becomes a deterministic security

E) None of these answers are correct.

A) an American call option becomes a European call option

B) an American put option becomes a digital put option

C) a futures contract simplifies to a forward contract

D) a swaption becomes a deterministic security

E) None of these answers are correct.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

11

A multiperiod binomial interest rate derivative pricing model:

A) has a vector of zero-coupon bonds evolving over time which are used for pricing derivatives

B) requires only a spot rate evolving over time for pricing derivatives

C) requires a money market account to earn a constant rate of interest across time

D) requires a stock whose value goes up in the "up state" and down in the "down state"

E) None of these answers are correct.

A) has a vector of zero-coupon bonds evolving over time which are used for pricing derivatives

B) requires only a spot rate evolving over time for pricing derivatives

C) requires a money market account to earn a constant rate of interest across time

D) requires a stock whose value goes up in the "up state" and down in the "down state"

E) None of these answers are correct.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

12

A multiperiod binomial model prices an interest rate derivative by:

A) computing an expected payoff of the derivative's values using actual probabilities

B) computing an expected payoff of the derivative's values using pseudo-probabilities

C) computing an expected value,using actual probabilities,of the derivative's values,discounted by the spot rates

D) computing an expected value,using pseudo-probabilities,of the derivative's values,discounted by the spot rates

E) None of these answers are correct.

A) computing an expected payoff of the derivative's values using actual probabilities

B) computing an expected payoff of the derivative's values using pseudo-probabilities

C) computing an expected value,using actual probabilities,of the derivative's values,discounted by the spot rates

D) computing an expected value,using pseudo-probabilities,of the derivative's values,discounted by the spot rates

E) None of these answers are correct.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

13

What are the up and down dollar returns on the three-period zero-coupon bond at time 0?

A) 1.046815,1.032195

B) 1.044801,1.034208

C) 1.039505,1.039505

D) 1.045130,1.038726

E) 1.031364,1.041928

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following statements about the binomial interest rate derivative pricing model is INCORRECT?

A) The binomial interest rate derivative pricing model assumes that the markets are competitive.

B) The binomial interest rate derivative pricing model assumes that there is no credit risk.

C) The binomial interest rate derivative pricing model requires as many bonds trading in each period as the number of periods in the entire tree.

D) In its most general form,the branches in a binomial interest rate tree do not recombine.

E) The binomial interest rate derivative pricing model imposes a structure on the evolution of zero-coupon bond prices.

A) The binomial interest rate derivative pricing model assumes that the markets are competitive.

B) The binomial interest rate derivative pricing model assumes that there is no credit risk.

C) The binomial interest rate derivative pricing model requires as many bonds trading in each period as the number of periods in the entire tree.

D) In its most general form,the branches in a binomial interest rate tree do not recombine.

E) The binomial interest rate derivative pricing model imposes a structure on the evolution of zero-coupon bond prices.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following statements about a binomial interest rate derivative pricing model is INCORRECT?

A) The model can be used to price European caplets and floorlets.

B) The model can be used to price a forward rate agreement.

C) The model can be used to price a Eurodollar futures contract.

D) The model can be used to price a swaption.

E) The model can be used to price an equity option.

A) The model can be used to price European caplets and floorlets.

B) The model can be used to price a forward rate agreement.

C) The model can be used to price a Eurodollar futures contract.

D) The model can be used to price a swaption.

E) The model can be used to price an equity option.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

16

What are the up and down dollar returns on the two-period zero-coupon bond at time 0?

A) 1.046815,1.032195

B) 1.044801,1.034208

C) 1.039505,1.039505

D) 1.045130,1.038726

E) 1.031364,1.041928

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

17

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

Consider a caplet with maturity time 1 and strike price 0.035.What is the time 0 value of the caplet?

A) 0.000000

B) 0.003525

C) 0.003198

D) 0.000000

E) 0.001763

Consider a caplet with maturity time 1 and strike price 0.035.What is the time 0 value of the caplet?

A) 0.000000

B) 0.003525

C) 0.003198

D) 0.000000

E) 0.001763

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

18

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

Consider a floorlet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

A) 0.000000,0.006649

B) 0.003525,0.000000

C) 0.003198,0.001696

D) 0.000000,0.003325

E) 0.001763,0.000000

Consider a floorlet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

A) 0.000000,0.006649

B) 0.003525,0.000000

C) 0.003198,0.001696

D) 0.000000,0.003325

E) 0.001763,0.000000

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following statements about caplet-floorlet parity is INCORRECT?

A) It is a relationship in the interest rate world that is analogous to put-call parity for European options in the world of equities that pay no dividends.

B) It enables you to price a floorlet using the price of a caplet along with some other relevant information.

C) It enables you to price a caplet using the price of a floorlet along with some other relevant information.

D) It is a relationship that links the prices of a caplet,a floorlet,and a zero-coupon bond with a forward rate.

E) It is a relationship that links the prices of four securities: a caplet,a floorlet,a stock,and a bond.

A) It is a relationship in the interest rate world that is analogous to put-call parity for European options in the world of equities that pay no dividends.

B) It enables you to price a floorlet using the price of a caplet along with some other relevant information.

C) It enables you to price a caplet using the price of a floorlet along with some other relevant information.

D) It is a relationship that links the prices of a caplet,a floorlet,and a zero-coupon bond with a forward rate.

E) It is a relationship that links the prices of four securities: a caplet,a floorlet,a stock,and a bond.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

20

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

-Consider a floorlet with maturity time 1 and strike price 0.035.What are the holdings in the three-period bond and money market account at time 0 that replicate the floorlet's time 1 payoffs in both the up and down nodes?

A) -0.499864,0.458009

B) 0.265009,-0.239428

C) 0.003198,0.001696

D) 0.000000,0.006640

E) 0.003525,0.000000

-Consider a floorlet with maturity time 1 and strike price 0.035.What are the holdings in the three-period bond and money market account at time 0 that replicate the floorlet's time 1 payoffs in both the up and down nodes?

A) -0.499864,0.458009

B) 0.265009,-0.239428

C) 0.003198,0.001696

D) 0.000000,0.006640

E) 0.003525,0.000000

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 20 flashcards in this deck.