Exam 24: Multiperiod Binomial Heath Jarrow Morton Model

Exam 1: Derivatives and Risk Management16 Questions

Exam 2: Interest Rates15 Questions

Exam 3: Stocks19 Questions

Exam 4: Forwards and Futures15 Questions

Exam 5: Options18 Questions

Exam 6: Arbitrage and Trading12 Questions

Exam 7: Financial Engineering and Swaps15 Questions

Exam 8: Forwards and Futures Markets17 Questions

Exam 9: Futures Trading14 Questions

Exam 10: Futures Regulations20 Questions

Exam 11: The Cost of Carry Model15 Questions

Exam 12: The Extended Cost-Of-Carry Model20 Questions

Exam 13: Futures Hedging13 Questions

Exam 14: Options Markets and Trading19 Questions

Exam 15: Option Trading Strategies16 Questions

Exam 16: Option Relations21 Questions

Exam 17: Single-Period Binomial Model21 Questions

Exam 18: Multiperiod Binomial Model26 Questions

Exam 19: The Black-Scholes-Merton Model23 Questions

Exam 20: Using the Black-Scholes-Merton Model17 Questions

Exam 21: Yields and Forward Rates17 Questions

Exam 22: Interest Rate Swaps20 Questions

Exam 23: Single Period Binomial Heath Jarrow Morton Model23 Questions

Exam 24: Multiperiod Binomial Heath Jarrow Morton Model20 Questions

Exam 25: The Heath Jarrow Morton Libor Model23 Questions

Exam 26: Risk-Management Models18 Questions

Select questions type

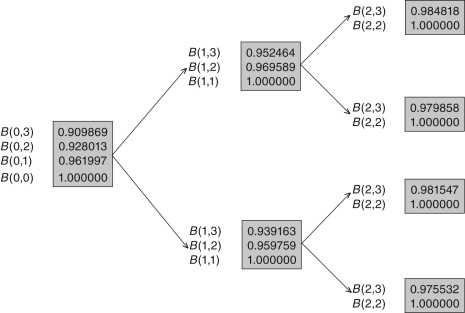

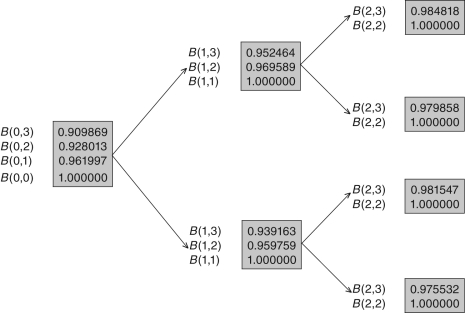

A multiperiod binomial interest rate derivative pricing model:

Free

(Multiple Choice)

4.8/5  (32)

(32)

Correct Answer: Verified

Verified

A

A necessary and sufficient condition to rule out arbitrage profits in the multiperiod binomial tree is that the following must hold:

Free

(Multiple Choice)

4.7/5 (33)

Correct Answer:Verified

D

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.  -Consider a forward rate agreement (FRA)with maturity date 2.What is the FRA rate on this contract at time 0?

-Consider a forward rate agreement (FRA)with maturity date 2.What is the FRA rate on this contract at time 0?

Free

(Multiple Choice)

4.7/5 (39)

Correct Answer:Verified

B

A multiperiod binomial model prices an interest rate derivative by:

(Multiple Choice)

4.9/5 (39)

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

-Consider a floorlet with maturity time 1 and strike price 0.035.What is the time 0 value of the floorlet?

(Multiple Choice)

4.8/5 (31)

Which of the following statements about a binomial interest rate derivative pricing model is INCORRECT?

(Multiple Choice)

4.9/5 (34)

-What is the value of the money market account in the up and down nodes at time 1?

-What is the value of the money market account in the up and down nodes at time 1?

(Multiple Choice)

4.9/5 (31)

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

-Consider a Eurodollar futures with maturity date 2.What is the Eurodollar futures rate on this contract at time 0?

(Multiple Choice)

4.9/5 (43)

Which of the following statements about the binomial interest rate derivative pricing model is INCORRECT?

(Multiple Choice)

4.8/5 (41)

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

-Consider a caplet with maturity time 1 and strike price 0.035.What is the time 0 value of the caplet?

(Multiple Choice)

4.8/5 (32)

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

-Consider a floorlet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

(Multiple Choice)

4.8/5 (40)

-What are the spot rates R(1)in the up and down nodes at time 1?

(Multiple Choice)

4.7/5 (26)

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

-Consider a caplet with maturity time 1 and strike price 0.035.What are the holdings in the three-period bond and money market account at time 0 that replicate the caplet's time 1 payoffs in both the up and down nodes?

(Multiple Choice)

4.7/5 (47)

Identify the INCORRECT statement.If we try to fit the following derivatives in a single-period framework,then:

(Multiple Choice)

4.8/5 (44)

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

-Consider a caplet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

(Multiple Choice)

4.9/5 (38)

Use the fact that the pseudo-probability of default at time zero is (1 / 2)to answer the questions that follow.

-Consider a floorlet with maturity time 1 and strike price 0.035.What are the holdings in the three-period bond and money market account at time 0 that replicate the floorlet's time 1 payoffs in both the up and down nodes?

(Multiple Choice)

4.8/5 (39)

-What are the up and down dollar returns on the two-period zero-coupon bond at time 0?

(Multiple Choice)

4.8/5 (30)

Which of the following statements about caplet-floorlet parity is INCORRECT?

(Multiple Choice)

4.7/5 (32)

-What are the up and down dollar returns on the three-period zero-coupon bond at time 0?

(Multiple Choice)

4.8/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)