Deck 7: Allocating Costs of Support Departments and Joint Products

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Figure 7-1

Luxurious Department Store incurred $6,000 of indirect advertising costs for its operations. The following data has been collected for 2016 for its three departments:

Refer to Figure 7-1. How much of the indirect advertising costs will be allocated to the Sportswear Department if newspaper ad space is the activity driver?

A) $6,000

B) $4,340

C) $3,720

D) $2,280

Luxurious Department Store incurred $6,000 of indirect advertising costs for its operations. The following data has been collected for 2016 for its three departments:

Refer to Figure 7-1. How much of the indirect advertising costs will be allocated to the Sportswear Department if newspaper ad space is the activity driver?

A) $6,000

B) $4,340

C) $3,720

D) $2,280

Question

Question

Question

Question

Question

Question

Question

Question

Figure 7-1

Luxurious Department Store incurred $6,000 of indirect advertising costs for its operations. The following data has been collected for 2016 for its three departments:

Refer to Figure 7-1. How much of the indirect advertising costs will be allocated to the Lingerie Department if direct advertising costs is the activity driver? (Round to the nearest dollar if necessary)

A) $3,000

B) $3,273

C) $6,000

D) $12,000

Luxurious Department Store incurred $6,000 of indirect advertising costs for its operations. The following data has been collected for 2016 for its three departments:

Refer to Figure 7-1. How much of the indirect advertising costs will be allocated to the Lingerie Department if direct advertising costs is the activity driver? (Round to the nearest dollar if necessary)

A) $3,000

B) $3,273

C) $6,000

D) $12,000

Question

Question

Question

Question

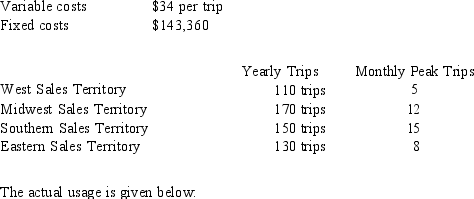

Figure 7-2

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 trips

West Sales Territory 100 trips

Midwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

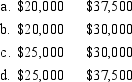

Refer to Figure 7-2. Using both a fixed and variable rate, what are the respective rates for fixed and variable per trip for the West Sales Territory? Fixed costs are allocated on the basis of monthly peak trips.

A) 12.5%; $34

B) 19.6%; $34

C) 18.2%; $34

D) 19%; $34

E) none of the above

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 tripsMidwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

Refer to Figure 7-2. Using both a fixed and variable rate, what are the respective rates for fixed and variable per trip for the West Sales Territory? Fixed costs are allocated on the basis of monthly peak trips.

A) 12.5%; $34

B) 19.6%; $34

C) 18.2%; $34

D) 19%; $34

E) none of the above

Question

A company incurred $80,000 of common fixed costs and $120,000 of common variable costs. These costs are to be allocated to Departments A and B. Data on capacity provided and capacity used are as follows: Capacity Provided Capacity Used

Department in Hours in Hours

Assume that both fixed and variable costs are allocated on the basis of capacity used. The fixed and variable costs allocated to Department A are

Assume that both fixed and variable costs are allocated on the basis of capacity used. The fixed and variable costs allocated to Department A are

Fixed Variable

A) $40,000 $60,000

B) $50,000 $60,000

C) $40,000 $75,000

D) $50,000 $75,000

Department in Hours in Hours

Assume that both fixed and variable costs are allocated on the basis of capacity used. The fixed and variable costs allocated to Department A areFixed Variable

A) $40,000 $60,000

B) $50,000 $60,000

C) $40,000 $75,000

D) $50,000 $75,000

Question

A company incurred $40,000 of common fixed costs and $60,000 of common variable costs. These costs are to be allocated to Departments A and B. Data on capacity provided and capacity used are as follows: Capacity Provided Capacity Used

Department in Hours in Hours

Assume that common fixed costs are to be allocated to Departments A and B on the basis of capacity provided and that common variable costs are to be allocated to Departments A and B on the basis of capacity used. The fixed and variable costs allocated to Department A are

Assume that common fixed costs are to be allocated to Departments A and B on the basis of capacity provided and that common variable costs are to be allocated to Departments A and B on the basis of capacity used. The fixed and variable costs allocated to Department A are

Fixed Variable

Department in Hours in Hours

Assume that common fixed costs are to be allocated to Departments A and B on the basis of capacity provided and that common variable costs are to be allocated to Departments A and B on the basis of capacity used. The fixed and variable costs allocated to Department A areFixed Variable

Question

Figure 7-2

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 trips

Midwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

Refer to Figure 7-2. Using a single charging rate, determine the rate per trip.

A) $256

B) $290

C) $295

D) $261

E) $34

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 tripsMidwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

Refer to Figure 7-2. Using a single charging rate, determine the rate per trip.

A) $256

B) $290

C) $295

D) $261

E) $34

Question

Question

FIGURE 7-5

Stronghold, Inc., operates a brochure business at two different locations. Stronghold, Inc., has one support department that is responsible for cleaning, service, and maintenance of its printing equipment. The costs of the support department are allocated to each brochure center on the basis of total brochures made.

During the first month, the costs of the support department were expected to be $400,000. Of this amount, $120,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $256,000 and actual fixed costs of $144,000.

Normal and actual activity (brochures made) are as follows:

Refer to Figure 7-5.For purposes of performance evaluation, fixed costs allocated to Brochure Center 1 are

A) $60,000.

B) $72,000.

C) $65,600.

D) $75,200.

Stronghold, Inc., operates a brochure business at two different locations. Stronghold, Inc., has one support department that is responsible for cleaning, service, and maintenance of its printing equipment. The costs of the support department are allocated to each brochure center on the basis of total brochures made.

During the first month, the costs of the support department were expected to be $400,000. Of this amount, $120,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $256,000 and actual fixed costs of $144,000.

Normal and actual activity (brochures made) are as follows:

Refer to Figure 7-5.For purposes of performance evaluation, fixed costs allocated to Brochure Center 1 are

A) $60,000.

B) $72,000.

C) $65,600.

D) $75,200.

Question

A company incurred $120,000 of common fixed costs and $180,000 of common variable costs. These costs are to be allocated to Departments XX and YY. Data on capacity provided and capacity used are as follows:  Assume that common fixed costs are to be allocated to Departments XX and YY on the basis of capacity provided

Assume that common fixed costs are to be allocated to Departments XX and YY on the basis of capacity provided

And that common variable costs are to be allocated to Departments XX and YY on the basis of capacity used. The fixed and variable costs allocated to Department XX are

Fixed Variable

A) $75,000 $112,500

B) $75,000 $90,000

C) $60,000 $112,500

D) $60,000 $90,000

Assume that common fixed costs are to be allocated to Departments XX and YY on the basis of capacity providedAnd that common variable costs are to be allocated to Departments XX and YY on the basis of capacity used. The fixed and variable costs allocated to Department XX are

Fixed Variable

A) $75,000 $112,500

B) $75,000 $90,000

C) $60,000 $112,500

D) $60,000 $90,000

Question

Figure 7-2

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 trips

Midwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

Refer to Figure 7-2. Using both a fixed and variable rate with fixed costs allocated on the basis of monthly peak trips, what will the West Sales Territory be charged for the year? (round to the nearest dollar)

A) $31,498

B) $21,320

C) $29,492

D) $30,638

E) none of the above

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 tripsMidwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

Refer to Figure 7-2. Using both a fixed and variable rate with fixed costs allocated on the basis of monthly peak trips, what will the West Sales Territory be charged for the year? (round to the nearest dollar)

A) $31,498

B) $21,320

C) $29,492

D) $30,638

E) none of the above

Question

FIGURE 7-4

Copies Plus Print operates a copy business at two different locations. Copies Plus Print has one support department that is responsible for cleaning, service, and maintenance of its copying equipment. The costs of the support department are allocated to each copy center on the basis of total copies made.

During the first month, the costs of the support department were expected to be $200,000. Of this amount, $60,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $128,000 and actual fixed costs of $72,000.

Normal and actual activity (copies made) are as follows:

Refer to Figure 7-4. For purposes of performance evaluation, fixed costs allocated to Copy Center 2 are

A) $28,800.

B) $60,000.

C) $51,200.

D) $24,000.

Copies Plus Print operates a copy business at two different locations. Copies Plus Print has one support department that is responsible for cleaning, service, and maintenance of its copying equipment. The costs of the support department are allocated to each copy center on the basis of total copies made.

During the first month, the costs of the support department were expected to be $200,000. Of this amount, $60,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $128,000 and actual fixed costs of $72,000.

Normal and actual activity (copies made) are as follows:

Refer to Figure 7-4. For purposes of performance evaluation, fixed costs allocated to Copy Center 2 are

A) $28,800.

B) $60,000.

C) $51,200.

D) $24,000.

Question

FIGURE 7-5

Stronghold, Inc., operates a brochure business at two different locations. Stronghold, Inc., has one support department that is responsible for cleaning, service, and maintenance of its printing equipment. The costs of the support department are allocated to each brochure center on the basis of total brochures made.

During the first month, the costs of the support department were expected to be $400,000. Of this amount, $120,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $256,000 and actual fixed costs of $144,000.

Normal and actual activity (brochures made) are as follows:

Refer to Figure 7-5. Support department costs NOT allocated to the two brochure centers are

A) $16,800.

B) $19,680.

C) $44,000.

D) $8,000.

Stronghold, Inc., operates a brochure business at two different locations. Stronghold, Inc., has one support department that is responsible for cleaning, service, and maintenance of its printing equipment. The costs of the support department are allocated to each brochure center on the basis of total brochures made.

During the first month, the costs of the support department were expected to be $400,000. Of this amount, $120,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $256,000 and actual fixed costs of $144,000.

Normal and actual activity (brochures made) are as follows:

Refer to Figure 7-5. Support department costs NOT allocated to the two brochure centers are

A) $16,800.

B) $19,680.

C) $44,000.

D) $8,000.

Question

FIGURE 7-5

Stronghold, Inc., operates a brochure business at two different locations. Stronghold, Inc., has one support department that is responsible for cleaning, service, and maintenance of its printing equipment. The costs of the support department are allocated to each brochure center on the basis of total brochures made.

During the first month, the costs of the support department were expected to be $400,000. Of this amount, $120,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $256,000 and actual fixed costs of $144,000.

Normal and actual activity (brochures made) are as follows:

Refer to Figure 7-5. For purposes of performance evaluation, fixed costs allocated to Brochure Center 2 are

A) $57,600.

B) $120,000.

C) $48,000.

D) $102,400.

Stronghold, Inc., operates a brochure business at two different locations. Stronghold, Inc., has one support department that is responsible for cleaning, service, and maintenance of its printing equipment. The costs of the support department are allocated to each brochure center on the basis of total brochures made.

During the first month, the costs of the support department were expected to be $400,000. Of this amount, $120,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $256,000 and actual fixed costs of $144,000.

Normal and actual activity (brochures made) are as follows:

Refer to Figure 7-5. For purposes of performance evaluation, fixed costs allocated to Brochure Center 2 are

A) $57,600.

B) $120,000.

C) $48,000.

D) $102,400.

Question

Figure 7-2

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 trips

Midwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

Refer to Figure 7-2. Using a single charging rate, how much will be charged to the West Sales Territory?

A) $29,000

B) $31,900

C) $29,500

D) $28,160

E) none of the above

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 tripsMidwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

Refer to Figure 7-2. Using a single charging rate, how much will be charged to the West Sales Territory?

A) $29,000

B) $31,900

C) $29,500

D) $28,160

E) none of the above

Question

A company incurred $120,000 of common fixed costs and $180,000 of common variable costs. These costs are to be allocated to Departments XX and YY. Data on capacity provided and capacity used are as follows:  Assume that both fixed and variable costs are allocated on the basis of capacity used. The fixed and variable costs

Assume that both fixed and variable costs are allocated on the basis of capacity used. The fixed and variable costs

Allocated to Department XX are

Fixed Variable

A) $75,000 $112,500

B) $75,000 $90,000

C) $60,000 $112,500

D) $60,000 $90,000

Assume that both fixed and variable costs are allocated on the basis of capacity used. The fixed and variable costsAllocated to Department XX are

Fixed Variable

A) $75,000 $112,500

B) $75,000 $90,000

C) $60,000 $112,500

D) $60,000 $90,000

Question

FIGURE 7-4

Copies Plus Print operates a copy business at two different locations. Copies Plus Print has one support department that is responsible for cleaning, service, and maintenance of its copying equipment. The costs of the support department are allocated to each copy center on the basis of total copies made.

During the first month, the costs of the support department were expected to be $200,000. Of this amount, $60,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $128,000 and actual fixed costs of $72,000.

Normal and actual activity (copies made) are as follows:

Refer to Figure 7-4. For purposes of performance evaluation, fixed costs allocated to Copy Center 1 are

A) $36,000.

B) $37,600.

C) $30,000.

D) $32,800.

Copies Plus Print operates a copy business at two different locations. Copies Plus Print has one support department that is responsible for cleaning, service, and maintenance of its copying equipment. The costs of the support department are allocated to each copy center on the basis of total copies made.

During the first month, the costs of the support department were expected to be $200,000. Of this amount, $60,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $128,000 and actual fixed costs of $72,000.

Normal and actual activity (copies made) are as follows:

Refer to Figure 7-4. For purposes of performance evaluation, fixed costs allocated to Copy Center 1 are

A) $36,000.

B) $37,600.

C) $30,000.

D) $32,800.

Question

FIGURE 7-4

Copies Plus Print operates a copy business at two different locations. Copies Plus Print has one support department that is responsible for cleaning, service, and maintenance of its copying equipment. The costs of the support department are allocated to each copy center on the basis of total copies made.

During the first month, the costs of the support department were expected to be $200,000. Of this amount, $60,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $128,000 and actual fixed costs of $72,000.

Normal and actual activity (copies made) are as follows:

Refer to Figure 7-4. Support department costs NOT allocated to the two copy centers are

A) $22,000.

B) $9,840.

C) $8,400.

D) $6,000.

Copies Plus Print operates a copy business at two different locations. Copies Plus Print has one support department that is responsible for cleaning, service, and maintenance of its copying equipment. The costs of the support department are allocated to each copy center on the basis of total copies made.

During the first month, the costs of the support department were expected to be $200,000. Of this amount, $60,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $128,000 and actual fixed costs of $72,000.

Normal and actual activity (copies made) are as follows:

Refer to Figure 7-4. Support department costs NOT allocated to the two copy centers are

A) $22,000.

B) $9,840.

C) $8,400.

D) $6,000.

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/171

Play

Full screen (f)

Deck 7: Allocating Costs of Support Departments and Joint Products

1

The use of a multiple charging rate is needed, one for variable costs, and one for fixed costs.

True

2

Joint production processes result in the output of two or more products produced simultaneously.

True

3

Departmental overhead rate is computed by dividing the budgeted base by the total overhead in a producing department.

False

4

The reciprocal method of allocation recognizes only some of the support departments' interactions.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

5

Departmental overhead is applied to products passing through the department.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

6

Allocation increases total costs.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

7

Causal factors are variables or activities within a producing department that stimulate the incurrence of support costs.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

8

Budgeted rates are allocated based on original capacity.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

9

A single changing rate uses the fixed costs of the support department.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

10

Dual rates combine the fixed and variable costs.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

11

The sequential method allocates costs in ranking order of support departments.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

12

The direct method is the most difficult way to allocate costs to the support departments.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

13

Allocation is not necessary when using JIT manufacturing.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

14

Common costs are mutually beneficial costs, used in the output of two or more services or products.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

15

Support department fixed costs are allocated on the basis of original capacity.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

16

Producing departments create products and services to make and sell.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

17

The three methods of allocating support center costs to producing departments are the direct, sequential, and reciprocal methods.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

18

Producing departments provide essential services for support departments.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

19

The choice of allocation method depends on an evaluation of costs and benefits, and circumstances.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

20

The overhead rate may be computed once allocation from support service cost to producing department has been performed.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

21

The charging rate combines variable and fixed costs of support departments.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following departments is NOT a support department?

A) food services

B) bottling

C) health services

D) security

A) food services

B) bottling

C) health services

D) security

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

23

Joint products are two or more products produced simultaneously by the same process.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

24

A common cost occurs

A) when only one product or service is benefited.

B) when different resources are used to produce one output.

C) when the same resource is used in the output of two or more outputs.

D) when a resource is used by two or more companies.

A) when only one product or service is benefited.

B) when different resources are used to produce one output.

C) when the same resource is used in the output of two or more outputs.

D) when a resource is used by two or more companies.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

25

Support departments

A) are responsible for manufacturing the products sold to customers.

B) work directly on the products of the firm.

C) provide services directly to customers.

D) provide essential services to the producing departments.

A) are responsible for manufacturing the products sold to customers.

B) work directly on the products of the firm.

C) provide services directly to customers.

D) provide essential services to the producing departments.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

26

Support department cost to the producing departments is(are) called:

A) direct materials

B) direct labor

C) activity driver

D) common cost

A) direct materials

B) direct labor

C) activity driver

D) common cost

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

27

Under the physical units method, joint costs are distributed to products on the basis of some physical measure.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

28

After allocation, total overhead in producing department is divided by the budgeted measure of activity to get the

__________ overhead rate.

__________ overhead rate.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

29

The method of allocating costs assumes "step down" interdepartmental services.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

30

The split-off point is the ending point of a joint product process.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

31

The method of allocating costs, allocates costs from support to producing departments.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

32

Departmental is applied to products passing through the department.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

33

A secondary product recovered during the manufacturing of a primary product during a joint process is called a(n):

__________ .

__________ .

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

34

Products produced simultaneously by the same process up to a point are called products.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

35

Costs that are easily traced to individual products are called separable costs.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

36

are mutually beneficial costs to joint product costing.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

37

Examples of support departments include all of the following EXCEPT

A) maintenance.

B) personnel.

C) machining.

D) data processing.

A) maintenance.

B) personnel.

C) machining.

D) data processing.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

38

Activities or variables within a producing department that provoke the incurrence of support costs are called

__________ .

__________ .

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

39

Support department costs are allocated on the basis of original capacity.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

40

The weight factor addresses the advantages of the physical units method.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

41

The Ruling Company assigns plant administration costs to the production departments based on the number of employees. Which of the following would NOT be a good combination of common costs with an activity driver?

A) personnel department costs based on number of employees

B) purchasing department costs based on machine hours

C) cafeteria costs based on meals served

D) warehouse costs based on the value of materials stored

A) personnel department costs based on number of employees

B) purchasing department costs based on machine hours

C) cafeteria costs based on meals served

D) warehouse costs based on the value of materials stored

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

42

The activities or variables within a producing department that provoke the incurrence of support costs are called:

A) Causal factors

B) Common costs

C) Cost objectives

D) Activity output

A) Causal factors

B) Common costs

C) Cost objectives

D) Activity output

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

43

Which of the following would be the most appropriate base for allocating the costs of the housekeeping department?

A) machine hours

B) direct labor hours

C) square feet

D) number of employees

A) machine hours

B) direct labor hours

C) square feet

D) number of employees

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

44

Support department costs are accounted for in which one of the following ways?

A) They are allocated directly to units of product.

B) They are allocated to producing departments and then allocated to units of product.

C) They are allocated to units of product and then allocated to the producing departments.

D) They are expensed as incurred.

A) They are allocated directly to units of product.

B) They are allocated to producing departments and then allocated to units of product.

C) They are allocated to units of product and then allocated to the producing departments.

D) They are expensed as incurred.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following would be the most appropriate base for allocating the costs of the maintenance department?

A) machine hours

B) direct labor hours

C) number of employees

D) square feet

A) machine hours

B) direct labor hours

C) number of employees

D) square feet

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

46

Which of the following cost categories would most likely use machine hours as its activity driver?

A) personnel

B) maintenance

C) purchasing

D) both a and b

A) personnel

B) maintenance

C) purchasing

D) both a and b

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following is NOT a major objective of allocation as identified by the IMA?

A) to detect fraud

B) to obtain a mutually agreeable price

C) to compute product-line profitability

D) to value inventory

A) to detect fraud

B) to obtain a mutually agreeable price

C) to compute product-line profitability

D) to value inventory

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

48

If a support department's costs were budgeted to be $150,000 and actual costs incurred by the support department were $200,000, the total amount of the support department's costs that should be allocated to other departments is

A) $350,000.

B) $200,000.

C) $150,000.

D) $50,000.

A) $350,000.

B) $200,000.

C) $150,000.

D) $50,000.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

49

A possible causal factor to use when allocating cafeteria costs would be

A) number of square feet.

B) number of direct labor hours.

C) number of employees.

D) appraised value of square footage.

A) number of square feet.

B) number of direct labor hours.

C) number of employees.

D) appraised value of square footage.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

50

Rules of financial reporting (GAAP) require

A) that direct manufacturing costs and a fair share of indirect manufacturing costs be assigned to products.

B) that only producing department costs be assigned to products.

C) that only direct manufacturing costs be assigned to products.

D) that only indirect manufacturing costs be assigned to products.

A) that direct manufacturing costs and a fair share of indirect manufacturing costs be assigned to products.

B) that only producing department costs be assigned to products.

C) that only direct manufacturing costs be assigned to products.

D) that only indirect manufacturing costs be assigned to products.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

51

Figure 7-1

Luxurious Department Store incurred $6,000 of indirect advertising costs for its operations. The following data has been collected for 2016 for its three departments:

Refer to Figure 7-1. How much of the indirect advertising costs will be allocated to the Sportswear Department if newspaper ad space is the activity driver?

A) $6,000

B) $4,340

C) $3,720

D) $2,280

Luxurious Department Store incurred $6,000 of indirect advertising costs for its operations. The following data has been collected for 2016 for its three departments:

Refer to Figure 7-1. How much of the indirect advertising costs will be allocated to the Sportswear Department if newspaper ad space is the activity driver?

A) $6,000

B) $4,340

C) $3,720

D) $2,280

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

52

The major objective(s) of allocations are

A) to motivate managers.

B) to compute product line profitability.

C) to value inventory.

D) all of the above.

A) to motivate managers.

B) to compute product line profitability.

C) to value inventory.

D) all of the above.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

53

Examples of producing departments include all of the following EXCEPT

A) mixing.

B) molding.

C) packaging.

D) accounting.

A) mixing.

B) molding.

C) packaging.

D) accounting.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

54

What is the most likely action to be taken by a company when a support department is NOT as cost effective as an outside source?

A) The company may force managers to use the internal support department.

B) The company may force managers to use an external source for the service.

C) The company may elect not to supply the service internally.

D) all of the above

A) The company may force managers to use the internal support department.

B) The company may force managers to use an external source for the service.

C) The company may elect not to supply the service internally.

D) all of the above

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following is NOT a benefit of the costs of support departments being allocated to production departments?

A) The allocation assists producing departments' use of support departments at a more efficient level.

B) Allocation of support department costs encourages managers of production departments to monitor performance of the support department.

C) The allocation helps each department select the correct level of support service consumption.

D) Management will use the information to support out-sourcing all support services.

A) The allocation assists producing departments' use of support departments at a more efficient level.

B) Allocation of support department costs encourages managers of production departments to monitor performance of the support department.

C) The allocation helps each department select the correct level of support service consumption.

D) Management will use the information to support out-sourcing all support services.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the major objectives of allocation as identified by the IMA would NOT be relevant in a service organization?

A) to obtain a mutually agreeable price

B) to compute product-line profitability

C) to predict the economic effects of planning and control

D) all of the above are objectives of allocation

A) to obtain a mutually agreeable price

B) to compute product-line profitability

C) to predict the economic effects of planning and control

D) all of the above are objectives of allocation

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

57

What is one of the potential disadvantages of NOT allocating support department costs to production departments?

A) total costs would not be accumulated

B) managers may tend to overconsume these services

C) this would encourage managers to monitor support department performance

D) managers will use a support service at a more efficient level

A) total costs would not be accumulated

B) managers may tend to overconsume these services

C) this would encourage managers to monitor support department performance

D) managers will use a support service at a more efficient level

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

58

Which of the following cost categories would most likely use the number of employees or new hires as its activity driver?

A) maintenance

B) purchasing

C) personnel

D) accounting

A) maintenance

B) purchasing

C) personnel

D) accounting

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

59

Figure 7-1

Luxurious Department Store incurred $6,000 of indirect advertising costs for its operations. The following data has been collected for 2016 for its three departments:

Refer to Figure 7-1. How much of the indirect advertising costs will be allocated to the Lingerie Department if direct advertising costs is the activity driver? (Round to the nearest dollar if necessary)

A) $3,000

B) $3,273

C) $6,000

D) $12,000

Luxurious Department Store incurred $6,000 of indirect advertising costs for its operations. The following data has been collected for 2016 for its three departments:

Refer to Figure 7-1. How much of the indirect advertising costs will be allocated to the Lingerie Department if direct advertising costs is the activity driver? (Round to the nearest dollar if necessary)

A) $3,000

B) $3,273

C) $6,000

D) $12,000

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

60

If the costs of support departments are NOT allocated to producing departments,

A) product costs would be understated.

B) GAAP requirements would not be met.

C) managers of producing departments may tend to overconsume services.

D) all of the above.

A) product costs would be understated.

B) GAAP requirements would not be met.

C) managers of producing departments may tend to overconsume services.

D) all of the above.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

61

Figure 7-3

Hanover and Trust, a large law firm, utilizes an internal centralized printing center to serve its three departments: Individuals, Corporate, Trust. The costs of the printing department include fixed costs of $69,190 and variable costs of $0.04 per page. Total estimated print pages are estimated to be 330,000 pages. Individuals are estimated to use 130,000; Corporate will use 165,000 and 35,000 from the trust area.

Refer to Figure 7-3. Assuming a single charging rate is used, if the total pages printed were 340,000, which of the following statements is correct?

A) The printing costs allocated to all departments would be $85,000.

B) The printing department would expect to incur costs of $82,790.

C) Any extra amount charged is due to the fixed costs being charged as if they were variable costs.

D) all of the above.

Hanover and Trust, a large law firm, utilizes an internal centralized printing center to serve its three departments: Individuals, Corporate, Trust. The costs of the printing department include fixed costs of $69,190 and variable costs of $0.04 per page. Total estimated print pages are estimated to be 330,000 pages. Individuals are estimated to use 130,000; Corporate will use 165,000 and 35,000 from the trust area.

Refer to Figure 7-3. Assuming a single charging rate is used, if the total pages printed were 340,000, which of the following statements is correct?

A) The printing costs allocated to all departments would be $85,000.

B) The printing department would expect to incur costs of $82,790.

C) Any extra amount charged is due to the fixed costs being charged as if they were variable costs.

D) all of the above.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

62

If the allocation is for product costing, the allocation of variable support department costs would be calculated as

A) Actual rate × Actual usage.

B) Actual rate × Budgeted usage.

C) Budgeted rate × Actual usage.

D) Budgeted rate × Budgeted usage.

A) Actual rate × Actual usage.

B) Actual rate × Budgeted usage.

C) Budgeted rate × Actual usage.

D) Budgeted rate × Budgeted usage.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

63

Figure 7-2

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 trips

Midwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

Refer to Figure 7-2. Using both a fixed and variable rate, what are the respective rates for fixed and variable per trip for the West Sales Territory? Fixed costs are allocated on the basis of monthly peak trips.

A) 12.5%; $34

B) 19.6%; $34

C) 18.2%; $34

D) 19%; $34

E) none of the above

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 tripsMidwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

Refer to Figure 7-2. Using both a fixed and variable rate, what are the respective rates for fixed and variable per trip for the West Sales Territory? Fixed costs are allocated on the basis of monthly peak trips.

A) 12.5%; $34

B) 19.6%; $34

C) 18.2%; $34

D) 19%; $34

E) none of the above

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

64

A company incurred $80,000 of common fixed costs and $120,000 of common variable costs. These costs are to be allocated to Departments A and B. Data on capacity provided and capacity used are as follows: Capacity Provided Capacity Used

Department in Hours in Hours

Assume that both fixed and variable costs are allocated on the basis of capacity used. The fixed and variable costs allocated to Department A are

Fixed Variable

A) $40,000 $60,000

B) $50,000 $60,000

C) $40,000 $75,000

D) $50,000 $75,000

Department in Hours in Hours

Assume that both fixed and variable costs are allocated on the basis of capacity used. The fixed and variable costs allocated to Department A areFixed Variable

A) $40,000 $60,000

B) $50,000 $60,000

C) $40,000 $75,000

D) $50,000 $75,000

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

65

A company incurred $40,000 of common fixed costs and $60,000 of common variable costs. These costs are to be allocated to Departments A and B. Data on capacity provided and capacity used are as follows: Capacity Provided Capacity Used

Department in Hours in Hours

Assume that common fixed costs are to be allocated to Departments A and B on the basis of capacity provided and that common variable costs are to be allocated to Departments A and B on the basis of capacity used. The fixed and variable costs allocated to Department A are

Fixed Variable

Department in Hours in Hours

Assume that common fixed costs are to be allocated to Departments A and B on the basis of capacity provided and that common variable costs are to be allocated to Departments A and B on the basis of capacity used. The fixed and variable costs allocated to Department A areFixed Variable

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

66

Figure 7-2

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 trips

Midwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

Refer to Figure 7-2. Using a single charging rate, determine the rate per trip.

A) $256

B) $290

C) $295

D) $261

E) $34

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 tripsMidwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

Refer to Figure 7-2. Using a single charging rate, determine the rate per trip.

A) $256

B) $290

C) $295

D) $261

E) $34

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

67

If a support department's costs were budgeted to be $75,000 and actual costs incurred by the support department were $70,000, the total amount of the support department's costs that should be allocated to other departments is

A) $145,000.

B) $75,000.

C) $70,000.

D) $5,000.

A) $145,000.

B) $75,000.

C) $70,000.

D) $5,000.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

68

FIGURE 7-5

Stronghold, Inc., operates a brochure business at two different locations. Stronghold, Inc., has one support department that is responsible for cleaning, service, and maintenance of its printing equipment. The costs of the support department are allocated to each brochure center on the basis of total brochures made.

During the first month, the costs of the support department were expected to be $400,000. Of this amount, $120,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $256,000 and actual fixed costs of $144,000.

Normal and actual activity (brochures made) are as follows:

Refer to Figure 7-5.For purposes of performance evaluation, fixed costs allocated to Brochure Center 1 are

A) $60,000.

B) $72,000.

C) $65,600.

D) $75,200.

Stronghold, Inc., operates a brochure business at two different locations. Stronghold, Inc., has one support department that is responsible for cleaning, service, and maintenance of its printing equipment. The costs of the support department are allocated to each brochure center on the basis of total brochures made.

During the first month, the costs of the support department were expected to be $400,000. Of this amount, $120,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $256,000 and actual fixed costs of $144,000.

Normal and actual activity (brochures made) are as follows:

Refer to Figure 7-5.For purposes of performance evaluation, fixed costs allocated to Brochure Center 1 are

A) $60,000.

B) $72,000.

C) $65,600.

D) $75,200.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

69

A company incurred $120,000 of common fixed costs and $180,000 of common variable costs. These costs are to be allocated to Departments XX and YY. Data on capacity provided and capacity used are as follows: Assume that common fixed costs are to be allocated to Departments XX and YY on the basis of capacity provided

And that common variable costs are to be allocated to Departments XX and YY on the basis of capacity used. The fixed and variable costs allocated to Department XX are

Fixed Variable

A) $75,000 $112,500

B) $75,000 $90,000

C) $60,000 $112,500

D) $60,000 $90,000

Assume that common fixed costs are to be allocated to Departments XX and YY on the basis of capacity providedAnd that common variable costs are to be allocated to Departments XX and YY on the basis of capacity used. The fixed and variable costs allocated to Department XX are

Fixed Variable

A) $75,000 $112,500

B) $75,000 $90,000

C) $60,000 $112,500

D) $60,000 $90,000

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

70

Figure 7-2

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 trips

Midwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

Refer to Figure 7-2. Using both a fixed and variable rate with fixed costs allocated on the basis of monthly peak trips, what will the West Sales Territory be charged for the year? (round to the nearest dollar)

A) $31,498

B) $21,320

C) $29,492

D) $30,638

E) none of the above

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 tripsMidwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

Refer to Figure 7-2. Using both a fixed and variable rate with fixed costs allocated on the basis of monthly peak trips, what will the West Sales Territory be charged for the year? (round to the nearest dollar)

A) $31,498

B) $21,320

C) $29,492

D) $30,638

E) none of the above

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

71

FIGURE 7-4

Copies Plus Print operates a copy business at two different locations. Copies Plus Print has one support department that is responsible for cleaning, service, and maintenance of its copying equipment. The costs of the support department are allocated to each copy center on the basis of total copies made.

During the first month, the costs of the support department were expected to be $200,000. Of this amount, $60,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $128,000 and actual fixed costs of $72,000.

Normal and actual activity (copies made) are as follows:

Refer to Figure 7-4. For purposes of performance evaluation, fixed costs allocated to Copy Center 2 are

A) $28,800.

B) $60,000.

C) $51,200.

D) $24,000.

Copies Plus Print operates a copy business at two different locations. Copies Plus Print has one support department that is responsible for cleaning, service, and maintenance of its copying equipment. The costs of the support department are allocated to each copy center on the basis of total copies made.

During the first month, the costs of the support department were expected to be $200,000. Of this amount, $60,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $128,000 and actual fixed costs of $72,000.

Normal and actual activity (copies made) are as follows:

Refer to Figure 7-4. For purposes of performance evaluation, fixed costs allocated to Copy Center 2 are

A) $28,800.

B) $60,000.

C) $51,200.

D) $24,000.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

72

FIGURE 7-5

Stronghold, Inc., operates a brochure business at two different locations. Stronghold, Inc., has one support department that is responsible for cleaning, service, and maintenance of its printing equipment. The costs of the support department are allocated to each brochure center on the basis of total brochures made.

During the first month, the costs of the support department were expected to be $400,000. Of this amount, $120,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $256,000 and actual fixed costs of $144,000.

Normal and actual activity (brochures made) are as follows:

Refer to Figure 7-5. Support department costs NOT allocated to the two brochure centers are

A) $16,800.

B) $19,680.

C) $44,000.

D) $8,000.

Stronghold, Inc., operates a brochure business at two different locations. Stronghold, Inc., has one support department that is responsible for cleaning, service, and maintenance of its printing equipment. The costs of the support department are allocated to each brochure center on the basis of total brochures made.

During the first month, the costs of the support department were expected to be $400,000. Of this amount, $120,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $256,000 and actual fixed costs of $144,000.

Normal and actual activity (brochures made) are as follows:

Refer to Figure 7-5. Support department costs NOT allocated to the two brochure centers are

A) $16,800.

B) $19,680.

C) $44,000.

D) $8,000.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

73

FIGURE 7-5

Stronghold, Inc., operates a brochure business at two different locations. Stronghold, Inc., has one support department that is responsible for cleaning, service, and maintenance of its printing equipment. The costs of the support department are allocated to each brochure center on the basis of total brochures made.

During the first month, the costs of the support department were expected to be $400,000. Of this amount, $120,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $256,000 and actual fixed costs of $144,000.

Normal and actual activity (brochures made) are as follows:

Refer to Figure 7-5. For purposes of performance evaluation, fixed costs allocated to Brochure Center 2 are

A) $57,600.

B) $120,000.

C) $48,000.

D) $102,400.

Stronghold, Inc., operates a brochure business at two different locations. Stronghold, Inc., has one support department that is responsible for cleaning, service, and maintenance of its printing equipment. The costs of the support department are allocated to each brochure center on the basis of total brochures made.

During the first month, the costs of the support department were expected to be $400,000. Of this amount, $120,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $256,000 and actual fixed costs of $144,000.

Normal and actual activity (brochures made) are as follows:

Refer to Figure 7-5. For purposes of performance evaluation, fixed costs allocated to Brochure Center 2 are

A) $57,600.

B) $120,000.

C) $48,000.

D) $102,400.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

74

Figure 7-2

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 trips

Midwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

Refer to Figure 7-2. Using a single charging rate, how much will be charged to the West Sales Territory?

A) $29,000

B) $31,900

C) $29,500

D) $28,160

E) none of the above

Long Distance Company's travel department had the following budgeted costs for the coming year:

West Sales Territory 100 tripsMidwest Sales Territory 150 trips

Southern Sales Territory 160 trips

Eastern Sales Territory 140 trips

Refer to Figure 7-2. Using a single charging rate, how much will be charged to the West Sales Territory?

A) $29,000

B) $31,900

C) $29,500

D) $28,160

E) none of the above

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

75

A company incurred $120,000 of common fixed costs and $180,000 of common variable costs. These costs are to be allocated to Departments XX and YY. Data on capacity provided and capacity used are as follows: Assume that both fixed and variable costs are allocated on the basis of capacity used. The fixed and variable costs

Allocated to Department XX are

Fixed Variable

A) $75,000 $112,500

B) $75,000 $90,000

C) $60,000 $112,500

D) $60,000 $90,000

Assume that both fixed and variable costs are allocated on the basis of capacity used. The fixed and variable costsAllocated to Department XX are

Fixed Variable

A) $75,000 $112,500

B) $75,000 $90,000

C) $60,000 $112,500

D) $60,000 $90,000

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

76

FIGURE 7-4

Copies Plus Print operates a copy business at two different locations. Copies Plus Print has one support department that is responsible for cleaning, service, and maintenance of its copying equipment. The costs of the support department are allocated to each copy center on the basis of total copies made.

During the first month, the costs of the support department were expected to be $200,000. Of this amount, $60,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $128,000 and actual fixed costs of $72,000.

Normal and actual activity (copies made) are as follows:

Refer to Figure 7-4. For purposes of performance evaluation, fixed costs allocated to Copy Center 1 are

A) $36,000.

B) $37,600.

C) $30,000.

D) $32,800.

Copies Plus Print operates a copy business at two different locations. Copies Plus Print has one support department that is responsible for cleaning, service, and maintenance of its copying equipment. The costs of the support department are allocated to each copy center on the basis of total copies made.

During the first month, the costs of the support department were expected to be $200,000. Of this amount, $60,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $128,000 and actual fixed costs of $72,000.

Normal and actual activity (copies made) are as follows:

Refer to Figure 7-4. For purposes of performance evaluation, fixed costs allocated to Copy Center 1 are

A) $36,000.

B) $37,600.

C) $30,000.

D) $32,800.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

77

FIGURE 7-4

Copies Plus Print operates a copy business at two different locations. Copies Plus Print has one support department that is responsible for cleaning, service, and maintenance of its copying equipment. The costs of the support department are allocated to each copy center on the basis of total copies made.

During the first month, the costs of the support department were expected to be $200,000. Of this amount, $60,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $128,000 and actual fixed costs of $72,000.

Normal and actual activity (copies made) are as follows:

Refer to Figure 7-4. Support department costs NOT allocated to the two copy centers are

A) $22,000.

B) $9,840.

C) $8,400.

D) $6,000.

Copies Plus Print operates a copy business at two different locations. Copies Plus Print has one support department that is responsible for cleaning, service, and maintenance of its copying equipment. The costs of the support department are allocated to each copy center on the basis of total copies made.

During the first month, the costs of the support department were expected to be $200,000. Of this amount, $60,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $128,000 and actual fixed costs of $72,000.

Normal and actual activity (copies made) are as follows:

Refer to Figure 7-4. Support department costs NOT allocated to the two copy centers are

A) $22,000.

B) $9,840.

C) $8,400.

D) $6,000.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

78

If the allocation is for performance evaluation, the allocation of variable support department costs would be calculated as

A) Actual rate × Actual usage.

B) Actual rate × Budgeted usage.

C) Budgeted rate × Actual usage.

D) Budgeted rate × Budgeted usage.

A) Actual rate × Actual usage.

B) Actual rate × Budgeted usage.

C) Budgeted rate × Actual usage.

D) Budgeted rate × Budgeted usage.

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

79

Figure 7-3

Hanover and Trust, a large law firm, utilizes an internal centralized printing center to serve its three departments: Individuals, Corporate, Trust. The costs of the printing department include fixed costs of $69,190 and variable costs of $0.04 per page. Total estimated print pages are estimated to be 330,000 pages. Individuals are estimated to use 130,000; Corporate will use 165,000 and 35,000 from the trust area.

Refer to Figure 7-3. Assuming a single charging rate is used, if the Corporate Department used 190,000 pages, what would be the printing charges for the Corporate Department? (Round to the nearest cent.)

A) $47,500

B) $39,900

C) $7,600

D) $42,195

Hanover and Trust, a large law firm, utilizes an internal centralized printing center to serve its three departments: Individuals, Corporate, Trust. The costs of the printing department include fixed costs of $69,190 and variable costs of $0.04 per page. Total estimated print pages are estimated to be 330,000 pages. Individuals are estimated to use 130,000; Corporate will use 165,000 and 35,000 from the trust area.

Refer to Figure 7-3. Assuming a single charging rate is used, if the Corporate Department used 190,000 pages, what would be the printing charges for the Corporate Department? (Round to the nearest cent.)

A) $47,500

B) $39,900

C) $7,600

D) $42,195

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

80

Figure 7-3

Hanover and Trust, a large law firm, utilizes an internal centralized printing center to serve its three departments: Individuals, Corporate, Trust. The costs of the printing department include fixed costs of $69,190 and variable costs of $0.04 per page. Total estimated print pages are estimated to be 330,000 pages. Individuals are estimated to use 130,000; Corporate will use 165,000 and 35,000 from the trust area.

Refer to Figure 7-3. Assuming a single charging rate is used, what would be the charge per page? (round to the nearest cent)

A) $.04

B) $.25

C) $.21

D) none of the above amounts

Hanover and Trust, a large law firm, utilizes an internal centralized printing center to serve its three departments: Individuals, Corporate, Trust. The costs of the printing department include fixed costs of $69,190 and variable costs of $0.04 per page. Total estimated print pages are estimated to be 330,000 pages. Individuals are estimated to use 130,000; Corporate will use 165,000 and 35,000 from the trust area.

Refer to Figure 7-3. Assuming a single charging rate is used, what would be the charge per page? (round to the nearest cent)

A) $.04

B) $.25

C) $.21

D) none of the above amounts

Unlock Deck

Unlock for access to all 171 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 171 flashcards in this deck.