Deck 7: The Cost of Production

Full screen (f)

Question

Question

Question

Question

Question

The total cost (TC) of producing computer software diskettes (Q) is given as:  What is the fixed cost?

What is the fixed cost?

A) 200

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

What is the fixed cost?A) 200

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

Question

Question

Question

Question

Question

Question

The total cost (TC) of producing computer software diskettes (Q) is given as:  What is the marginal cost?

What is the marginal cost?

A) 200

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

What is the marginal cost?A) 200

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

Question

The total cost (TC) of producing computer software diskettes (Q) is given as:  . What is the variable cost?

. What is the variable cost?

A) 200

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

. What is the variable cost?A) 200

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

Question

The total cost (TC) of producing computer software diskettes (Q) is given as:  What is the average fixed cost?

What is the average fixed cost?

A) 500

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

What is the average fixed cost?A) 500

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

Question

Question

Question

Question

Question

The total cost (TC) of producing computer software diskettes (Q) is given as:  What is the average total cost?

What is the average total cost?

A) 500

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

What is the average total cost?A) 500

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

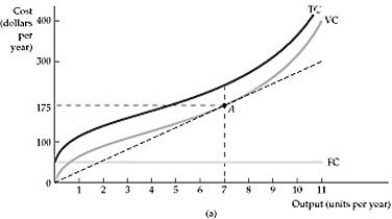

Figure 7.2.1

Figure 7.2.1Refer to Figure 7.2.1 above. The diagram above contains ________ cost curves.

A) short-run

B) intermediate run

C) long-run

D) both short-run and long-run

Question

Question

Question

Question

Question

Question

Figure 7.2.1Refer to Figure 7.2.1 above. At what level of output are average total cost, average cost, average fixed cost and marginal cost increasing?

A) 2 units of output

B) 7 units of output

C) 10 units of output

D) none of the above

Question

Figure 7.2.1Refer to Figure 7.2.1 above. When 2 units of output are produced:

A) marginal cost is falling.

B) average total cost is falling.

C) average variable cost is less than average fixed cost.

D) marginal cost is less than average total cost.

E) all of the above

Question

Question

Question

Question

Question

Question

Figure 7.2.1Refer to Figure 7.2.1 above. At what level of output is average total cost closest to marginal cost?

A) 2 units of output

B) 7 units of output

C) 8 units of output

D) 10 units of output

Question

Question

Question

Question

Question

Question

Figure 7.2.1Refer to Figure 7.2.1 above. When 7 units of output are produced:

A) average fixed cost reaches its minimum.

B) average total cost reaches its minimum.

C) average variable cost reaches its minimum.

D) marginal cost reaches its minimum.

E) all of the above

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

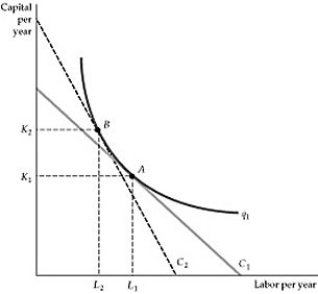

Figure 7.3.2

Figure 7.3.2Refer to Figure 7.3.2 above. Which of the following changes, which causes the move from A to B?

A) The price of one of the inputs

B) the productivity of inputs

C) The quantity to be produced

D) The budget of the producer

Question

Question

Question

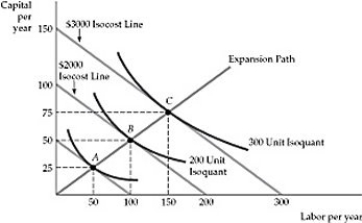

Figure 7.3.3

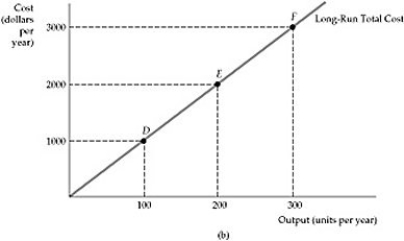

Figure 7.3.3Refer to Figure 7.3.3 above. The expansion path in the figure leads to the construction of:

A) a short run marginal cost curve.

B) a long run marginal cost curve.

C) a long run total cost curve.

D) a long run average total cost curve.

Question

Question

Question

Question

Question

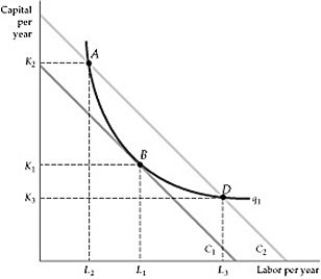

Figure 7.3.1

Figure 7.3.1Refer to Figure 7.3.1 above. Which point on the graph shows the optimal combination of inputs?

A) Point A, when the production process is capital intensive

B) Point B

C) Point D, when the production process is capital intensive

D) All three points, A, B and D are optimal

Question

Question

Figure 7.3.4

Figure 7.3.4Refer to Figure 7.3.4 above. The long run cost curve comes from:

A) a map of isoquants.

B) a map of isocosts.

C) an expansion path.

D) an optimal combination of inputs for a given level of output.

Question

Suppose that the price of labor (  ) is $10 and the price of capital (

) is $10 and the price of capital (  ) is $20. What is the equation of the isocost line corresponding to a total cost of $100?

) is $20. What is the equation of the isocost line corresponding to a total cost of $100?

A) PL + 20PK

B) 100 = 10L + 20K

C) 100 = 30(L+K)

D) 100 + 30

E) none of the above

) is $10 and the price of capital ( ) is $20. What is the equation of the isocost line corresponding to a total cost of $100?A) PL + 20PK

B) 100 = 10L + 20K

C) 100 = 30(L+K)

D) 100 + 30

E) none of the above

Question

Figure 7.3.4At the optimum combination of two inputs,

A) the slopes of the isoquant and isocost curves are equal.

B) costs are minimized for the production of a given output.

C) the marginal rate of technical substitution equals the ratio of input prices.

D) all of the above

E) A and C only

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/178

Play

Full screen (f)

Deck 7: The Cost of Production

1

Fixed costs are fixed with respect to changes in:

A) output.

B) capital expenditure.

C) wages.

D) time.

A) output.

B) capital expenditure.

C) wages.

D) time.

output.

2

Prospective sunk costs:

A) are relevant to economic decision-making.

B) are considered as investment decisions.

C) rise as output rises.

D) do not occur when output equals zero.

A) are relevant to economic decision-making.

B) are considered as investment decisions.

C) rise as output rises.

D) do not occur when output equals zero.

are relevant to economic decision-making.

3

Which of the following statements correctly uses the concept of opportunity cost in decision making? I. "Because my secretary's time has already been paid for, my cost of taking on an additional project is lower than it otherwise would be."

II) "Since NASA is running under budget this year, the cost of another space shuttle launch is lower than it otherwise would be."

A) I is true, and II is false.

B) I is false, and II is true.

C) I and II are both true.

D) I and II are both false.

II) "Since NASA is running under budget this year, the cost of another space shuttle launch is lower than it otherwise would be."

A) I is true, and II is false.

B) I is false, and II is true.

C) I and II are both true.

D) I and II are both false.

I and II are both false.

4

Two small airlines provide shuttle service between Las Vegas and Reno. The services are alike in every respect except that Fly Right bought its airplane for $500,000, while Fly by Night rents its plane for $30,000 a year. If Fly Right were to go out of business, it would be able to rent its plane to another airline for $30,000. Which airline has the lower costs?

A) Fly Right.

B) Fly by Night

C) Neither, the costs are identical.

D) Neither, Fly by Night has lower costs at small output levels and Fly Right has lower costs at high output levels.

A) Fly Right.

B) Fly by Night

C) Neither, the costs are identical.

D) Neither, Fly by Night has lower costs at small output levels and Fly Right has lower costs at high output levels.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

5

The total cost (TC) of producing computer software diskettes (Q) is given as: What is the fixed cost?

A) 200

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

What is the fixed cost?A) 200

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

6

Constantine purchased 100 shares of IBM stock several years ago for $150 per share. The price of these shares has fallen to $55 per share. Constantine's investment strategy is "buy low, sell high." Therefore, he will not sell his IBM stock until the price rises above $150 per share. If he sells at a price lower than $150 per share he will have "bought high and sold low." Constantine's decision:

A) is correct and shows a solid command of the nature of opportunity cost.

B) is incorrect because the original price paid for the shares is a sunk cost and should have no bearing on whether the shares should be held or sold.

C) is incorrect because when the price of a stock falls, the law of demand states that he should buy more shares.

D) is incorrect because it treats the price of the shares as an explicit cost.

A) is correct and shows a solid command of the nature of opportunity cost.

B) is incorrect because the original price paid for the shares is a sunk cost and should have no bearing on whether the shares should be held or sold.

C) is incorrect because when the price of a stock falls, the law of demand states that he should buy more shares.

D) is incorrect because it treats the price of the shares as an explicit cost.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following statements demonstrates an understanding of the importance of sunk costs for decision making? I. "Even though I hate my MBA classes, I can't quit because I've spent so much money on tuition."

II) "To break into the market for soap our firm needs to spend $10M on creating an image that is unique to our new product. When deciding whether to develop the new soap, we need to take this marketing cost into account."

A) I only

B) II only

C) Both I and II

D) Neither I nor II

II) "To break into the market for soap our firm needs to spend $10M on creating an image that is unique to our new product. When deciding whether to develop the new soap, we need to take this marketing cost into account."

A) I only

B) II only

C) Both I and II

D) Neither I nor II

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following statements is true regarding the differences between economic and accounting costs?

A) Accounting costs include all implicit and explicit costs.

B) Economic costs include implied costs only.

C) Accountants consider only implicit costs when calculating costs.

D) Accounting costs include only explicit costs.

A) Accounting costs include all implicit and explicit costs.

B) Economic costs include implied costs only.

C) Accountants consider only implicit costs when calculating costs.

D) Accounting costs include only explicit costs.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

9

Incremental cost is the same concept as ________ cost.

A) average

B) marginal

C) fixed

D) variable

A) average

B) marginal

C) fixed

D) variable

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

10

The difference between the economic and accounting costs of a firm are:

A) the accountant's fees.

B) the corporate taxes on profits .

C) the opportunity costs of the factors of production that the firm owns.

D) the sunk costs incurred by the firm.

E) the explicit costs of the firm.

A) the accountant's fees.

B) the corporate taxes on profits .

C) the opportunity costs of the factors of production that the firm owns.

D) the sunk costs incurred by the firm.

E) the explicit costs of the firm.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

11

The total cost (TC) of producing computer software diskettes (Q) is given as: What is the marginal cost?

A) 200

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

What is the marginal cost?A) 200

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

12

The total cost (TC) of producing computer software diskettes (Q) is given as: . What is the variable cost?

A) 200

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

. What is the variable cost?A) 200

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

13

The total cost (TC) of producing computer software diskettes (Q) is given as: What is the average fixed cost?

A) 500

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

What is the average fixed cost?A) 500

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

14

Consider the following statements when answering this question. I. Increases in the rate of income tax decrease the opportunity cost of attending college.

II) The introduction of distance learning, which enables students to watch lectures at home, decreases the opportunity cost of attending college.

A) I is true, and II is false.

B) I is false, and II is true.

C) I and II are both true.

D) I and II are both false.

II) The introduction of distance learning, which enables students to watch lectures at home, decreases the opportunity cost of attending college.

A) I is true, and II is false.

B) I is false, and II is true.

C) I and II are both true.

D) I and II are both false.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

15

Carolyn knows average total cost and average variable cost for a given level of output. Which of the following costs can she not determine given this information?

A) Total cost

B) Average fixed cost

C) Fixed cost

D) Variable cost

E) Carolyn can determine all of the above costs given the information provided.

A) Total cost

B) Average fixed cost

C) Fixed cost

D) Variable cost

E) Carolyn can determine all of the above costs given the information provided.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

16

Farmer Jones bought his farm for $75,000 in 1975. Today the farm is worth $500,000, and the interest rate is 10 percent. ABC Corporation has offered to buy the farm today for $500,000 and XYZ Corporation has offered to buy the farm for $530,000 one year from now. Farmer Jones could earn net profit of $15,000 (over and above all of his expenses) if he farms the land this year. What should he do?

A) Sell to ABC Corporation.

B) Farm the land for another year and sell to XYZ Corporation.

C) Accept either offer as they are equivalent.

D) Reject both offers.

A) Sell to ABC Corporation.

B) Farm the land for another year and sell to XYZ Corporation.

C) Accept either offer as they are equivalent.

D) Reject both offers.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following costs always declines as output increases?

A) Average cost

B) Marginal cost

C) Fixed cost

D) Average fixed cost

E) Average variable cost

A) Average cost

B) Marginal cost

C) Fixed cost

D) Average fixed cost

E) Average variable cost

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

18

The total cost (TC) of producing computer software diskettes (Q) is given as: What is the average total cost?

A) 500

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

What is the average total cost?A) 500

B) 5Q

C) 5

D) 5 + (200/Q)

E) none of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

19

In order for a taxicab to be operated in New York City, it must have a medallion on its hood. Medallions are expensive, but can be resold, and are therefore an example of:

A) a fixed cost.

B) a variable cost.

C) an implicit cost.

D) an opportunity cost.

E) a sunk cost.

A) a fixed cost.

B) a variable cost.

C) an implicit cost.

D) an opportunity cost.

E) a sunk cost.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

20

In 1985, Alice paid $20,000 for an option to purchase ten acres of land. By paying the $20,000, she bought the right to buy the land for $100,000 in 1992. When she acquired the option in 1985, the land was worth $120,000. In 1992, it is worth $110,000. Should Alice exercise the option and pay $100,000 for the land?

A) Yes

B) No

C) It depends on what the rate of inflation was between 1985 and 1992.

D) It depends on what the rate of interest was.

A) Yes

B) No

C) It depends on what the rate of inflation was between 1985 and 1992.

D) It depends on what the rate of interest was.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

21

Use the following two statements to answer this question: I. The average total cost of a given level of output is the slope of the line from the origin to the total cost curve at that level of output.

II The marginal cost of a given level of output is the slope of the line that is tangent to the total cost curve at that level of output.

A) Both I and II are true.

B) I is true, and II is false.

C) I is false, and II is true.

D) Both I and II are false.

II The marginal cost of a given level of output is the slope of the line that is tangent to the total cost curve at that level of output.

A) Both I and II are true.

B) I is true, and II is false.

C) I is false, and II is true.

D) Both I and II are false.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

22

Scenario 7.1:

The average total cost to produce 100 cookies is $0.25 per cookie. The marginal cost is constant at $0.10 for all cookies produced.

Refer to Scenario 7.1. For 100 cookies, the average total cost is:

A) falling.

B) rising.

C) neither rising nor falling.

D) less than average fixed cost.

The average total cost to produce 100 cookies is $0.25 per cookie. The marginal cost is constant at $0.10 for all cookies produced.

Refer to Scenario 7.1. For 100 cookies, the average total cost is:

A) falling.

B) rising.

C) neither rising nor falling.

D) less than average fixed cost.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

23

Use the following two statements to answer this question: I. The average total cost of a given level of output is the slope of the line from the origin to the total cost curve at that level of output.

II) The marginal cost of a given level of output is the slope of the line that is tangent to the variable cost curve at that level of output.

A) Both I and II are true.

B) I is true, and II is false.

C) I is false, and II is true.

D) Both I and II are false.

II) The marginal cost of a given level of output is the slope of the line that is tangent to the variable cost curve at that level of output.

A) Both I and II are true.

B) I is true, and II is false.

C) I is false, and II is true.

D) Both I and II are false.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

24

We typically think of labor as a variable cost, even in the very short run. However, some labor costs may be fixed. Which of the following items represents an example of a fixed labor cost?

A) An hourly employee

B) A temporary worker who is paid by the hour

C) A salaried manager who has a three-year employment contract

D) none of the above

A) An hourly employee

B) A temporary worker who is paid by the hour

C) A salaried manager who has a three-year employment contract

D) none of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

25

Scenario 7.1:

The average total cost to produce 100 cookies is $0.25 per cookie. The marginal cost is constant at $0.10 for all cookies produced.

Refer to Scenario 7.1. The total cost to produce 50 cookies is:

A) $20

B) $25

C) $50

D) $60

E) indeterminate

The average total cost to produce 100 cookies is $0.25 per cookie. The marginal cost is constant at $0.10 for all cookies produced.

Refer to Scenario 7.1. The total cost to produce 50 cookies is:

A) $20

B) $25

C) $50

D) $60

E) indeterminate

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

26

Complete the following table:

Total Variable Fixed Marginal

Output Cost Cost Cost Cost

0 50

1 60

2 75

3 100

4 150

5 225

6 400

Total Variable Fixed Marginal

Output Cost Cost Cost Cost

0 50

1 60

2 75

3 100

4 150

5 225

6 400

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

27

Scenario 7.1:

The average total cost to produce 100 cookies is $0.25 per cookie. The marginal cost is constant at $0.10 for all cookies produced.

Refer to Scenario 7.1. Which piece of information would NOT be helpful in calculating the marginal cost of the 75th unit of output?

A) The total cost of 75 units

B) The total cost of 74 units

C) The variable cost of 75 units

D) The variable cost of 74 units

E) The firm's fixed cost

The average total cost to produce 100 cookies is $0.25 per cookie. The marginal cost is constant at $0.10 for all cookies produced.

Refer to Scenario 7.1. Which piece of information would NOT be helpful in calculating the marginal cost of the 75th unit of output?

A) The total cost of 75 units

B) The total cost of 74 units

C) The variable cost of 75 units

D) The variable cost of 74 units

E) The firm's fixed cost

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

28

Scenario 7.1:

The average total cost to produce 100 cookies is $0.25 per cookie. The marginal cost is constant at $0.10 for all cookies produced.

Refer to Scenario 7.1. The total cost to produce 100 cookies is:

A) $0.10

B) $0.25

C) $25.00

D) $100.00

E) indeterminate

The average total cost to produce 100 cookies is $0.25 per cookie. The marginal cost is constant at $0.10 for all cookies produced.

Refer to Scenario 7.1. The total cost to produce 100 cookies is:

A) $0.10

B) $0.25

C) $25.00

D) $100.00

E) indeterminate

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

29

For any given level of output:

A) marginal cost must be greater than average cost.

B) average variable cost must be greater than average fixed cost.

C) average fixed cost must be greater than average variable cost.

D) fixed cost must be greater than variable cost.

E) None of the above is necessarily correct.

A) marginal cost must be greater than average cost.

B) average variable cost must be greater than average fixed cost.

C) average fixed cost must be greater than average variable cost.

D) fixed cost must be greater than variable cost.

E) None of the above is necessarily correct.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

30

In a short-run production process, the marginal cost is rising and the average total cost is falling as output is increased. Thus, marginal cost is:

A) below average total cost.

B) above average total cost.

C) between the average variable and average total cost curves.

D) below average fixed cost.

A) below average total cost.

B) above average total cost.

C) between the average variable and average total cost curves.

D) below average fixed cost.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

31

Complete the following table (round each answer to the nearest whole number):

Total Variable Fixed Marginal Average Avg. Var. Avg. Fixed

Output Cost Cost Cost Cost Cost Cost Cost

0

1 5

2 30

3 13

4 105 10

5 110

6 50

Total Variable Fixed Marginal Average Avg. Var. Avg. Fixed

Output Cost Cost Cost Cost Cost Cost Cost

0

1 5

2 30

3 13

4 105 10

5 110

6 50

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following relationships is NOT valid?

A) Rising marginal cost implies that average total cost is also rising.

B) When marginal cost is below average total cost, the latter is falling.

C) When marginal cost is above average variable cost, AVC is rising.

D) none of the above

A) Rising marginal cost implies that average total cost is also rising.

B) When marginal cost is below average total cost, the latter is falling.

C) When marginal cost is above average variable cost, AVC is rising.

D) none of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

33

Complete the following table (round each answer to the nearest whole number):

Total Variable Fixed Marginal Average Avg. Var. Avg. Fixed

Output Cost Cost Cost Cost Cost Cost Cost

0 30

1 35

2 60

3 110

4 200

5 320

6 600

Total Variable Fixed Marginal Average Avg. Var. Avg. Fixed

Output Cost Cost Cost Cost Cost Cost Cost

0 30

1 35

2 60

3 110

4 200

5 320

6 600

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

34

From Example 7.2, most pizza restaurants have large fixed costs and relatively low variable costs. What does this tell us about the average variable cost (AVC) of producing pizza?

A) AVC is relatively low.

B) AVC is relatively high.

C) AVC is high for low quantities but declines quickly.

D) AVC is increasing for all quantity levels.

A) AVC is relatively low.

B) AVC is relatively high.

C) AVC is high for low quantities but declines quickly.

D) AVC is increasing for all quantity levels.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

35

Figure 7.2.1Refer to Figure 7.2.1 above. The diagram above contains ________ cost curves.

A) short-run

B) intermediate run

C) long-run

D) both short-run and long-run

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

36

Jim left his previous job as a sales manager and started his own sales consulting business. He previously earned $70,000 per year, but he now pays himself $25,000 per year while he is building the new business. What is the economic cost of the time he contributes to the new business?

A) $25,000 per year

B) Zero

C) $70,000 per year

D) $45,000 per year

A) $25,000 per year

B) Zero

C) $70,000 per year

D) $45,000 per year

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

37

Your firm owns an old truck that is used to make local deliveries. The truck is fully depreciated and only costs $1.20 per hour to operate, but you could rent it to another firm for $15.00 per hour. What is the opportunity cost of operating this truck in your business?

A) $1.20 per hour

B) $15.00 per hour

C) $16.20 per hour

D) Less than $1.20 per hour

A) $1.20 per hour

B) $15.00 per hour

C) $16.20 per hour

D) Less than $1.20 per hour

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

38

Use the following two statements to answer this question: I. The average cost curve and the average variable cost curve reach their minima at the same level of output.

II) The average cost curve and the marginal cost curve reach their minima at the same level of output.

A) Both I and II are true.

B) I is true, and II is false.

C) I is false, and II is true.

D) Both I and II are false.

II) The average cost curve and the marginal cost curve reach their minima at the same level of output.

A) Both I and II are true.

B) I is true, and II is false.

C) I is false, and II is true.

D) Both I and II are false.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

39

Complete the following table:

Total Variable Fixed Marginal

Output Cost Cost Cost Cost

0 60

1 10

2 90

3 100

4 80

5 180

6 50

Total Variable Fixed Marginal

Output Cost Cost Cost Cost

0 60

1 10

2 90

3 100

4 80

5 180

6 50

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

40

In a short-run production process, the marginal cost is rising and the average variable cost is falling as output is increased. Thus,

A) average fixed cost is constant.

B) marginal cost is above average variable cost.

C) marginal cost is below average fixed cost.

D) marginal cost is below average variable cost.

A) average fixed cost is constant.

B) marginal cost is above average variable cost.

C) marginal cost is below average fixed cost.

D) marginal cost is below average variable cost.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

41

Figure 7.2.1Refer to Figure 7.2.1 above. At what level of output are average total cost, average cost, average fixed cost and marginal cost increasing?

A) 2 units of output

B) 7 units of output

C) 10 units of output

D) none of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

42

Figure 7.2.1Refer to Figure 7.2.1 above. When 2 units of output are produced:

A) marginal cost is falling.

B) average total cost is falling.

C) average variable cost is less than average fixed cost.

D) marginal cost is less than average total cost.

E) all of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

43

Suppose a pizza restaurant has two pizza ovens that may be used to bake pizzas, so the restaurant has a maximum capacity constraint that affects the shape of the firm's short-run marginal cost curve. What happens to maximum capacity segment of this curve if the firm adds another pizza oven?

A) Shifts upward

B) Shifts downward

C) Shifts leftward

D) Shifts rightward

A) Shifts upward

B) Shifts downward

C) Shifts leftward

D) Shifts rightward

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

44

In our analysis, it is best to treat capital as if it was:

A) rented, even if it was purchased.

B) purchased, even if it is just rented.

C) purchased and also rented.

D) rented first, then purchased.

A) rented, even if it was purchased.

B) purchased, even if it is just rented.

C) purchased and also rented.

D) rented first, then purchased.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following is the user cost of capital?

A) implicit cost of capital + explicit cost of capital

B) interest rate × value of capital - depreciation

C) economic depreciation + (interest rate)(value of capital)

D) interest rate - depreciation

A) implicit cost of capital + explicit cost of capital

B) interest rate × value of capital - depreciation

C) economic depreciation + (interest rate)(value of capital)

D) interest rate - depreciation

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

46

Consider the following statements when answering this question: I. If the marginal product of labor falls whenever more labor is used, and labor is the only factor of production used by the firm, than at every output level the firm's short-run average variable cost exceeds marginal cost.

II) If labor obeys the law of diminishing returns, and is the only factor of production used by the firm, then at every output level short-run average variable costs exceed marginal costs.

A) I is true, and II is false.

B) I is false, and II is true.

C) I and II are both true.

D) I and II are both false.

II) If labor obeys the law of diminishing returns, and is the only factor of production used by the firm, then at every output level short-run average variable costs exceed marginal costs.

A) I is true, and II is false.

B) I is false, and II is true.

C) I and II are both true.

D) I and II are both false.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

47

Trisha believes the production of a dress requires 4 labor hours and 2 machine hours to produce. If Trisha decides to operate in the short run, she must spend $500 to lease her business space. Also, a labor hour costs $15 and a machine hour costs $35. What is Trisha's cost of production as a function of dresses produced?

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

48

Figure 7.2.1Refer to Figure 7.2.1 above. At what level of output is average total cost closest to marginal cost?

A) 2 units of output

B) 7 units of output

C) 8 units of output

D) 10 units of output

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

49

In the short run, suppose average total cost is a straight line and marginal cost is positive and constant. Then, we know that fixed costs must:

A) be declining with output.

B) be positive.

C) equal zero.

D) We do not have enough information to answer this question.

A) be declining with output.

B) be positive.

C) equal zero.

D) We do not have enough information to answer this question.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

50

In the short run, suppose average total cost is a straight line and marginal cost is positive and constant. Then, we know that:

A) marginal cost is less than average total cost.

B) average total cost is positive and constant.

C) average total cost equals marginal cost.

D) A and B are correct.

E) B and C are correct.

A) marginal cost is less than average total cost.

B) average total cost is positive and constant.

C) average total cost equals marginal cost.

D) A and B are correct.

E) B and C are correct.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

51

Consider the following statements when answering this question: I. The marginal cost curve intersects the average total cost and average variable cost curves at their minimum values.

II) When a firm has positive fixed costs, the output level associated with minimum average variable costs is less than the output associated with minimum average total costs.

A) I is true, and II is false.

B) I is false, and II is true.

C) I and II are both true.

D) I and II are both false.

II) When a firm has positive fixed costs, the output level associated with minimum average variable costs is less than the output associated with minimum average total costs.

A) I is true, and II is false.

B) I is false, and II is true.

C) I and II are both true.

D) I and II are both false.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

52

Consider the following statements when answering this question: I. Whenever a firm's average variable costs are falling as output rises, marginal costs must be falling too.

II) Whenever a firm's average total costs are rising as output rises, average variable costs must be rising too.

A) I is true, and II is false.

B) I is false, and II is true.

C) I and II are both true.

D) I and II are both false.

II) Whenever a firm's average total costs are rising as output rises, average variable costs must be rising too.

A) I is true, and II is false.

B) I is false, and II is true.

C) I and II are both true.

D) I and II are both false.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

53

Annual economic depreciation equals:

A) the value of capital at end of year minus new investment.

B) the amortization payment made annually for the purchase of an asset, spread over the life of the asset.

C) the annual loss of value of buildings and machines due to deterioration.

D) the change in the weighted average cost of capital, or percentage change in the components of debt and equity.

A) the value of capital at end of year minus new investment.

B) the amortization payment made annually for the purchase of an asset, spread over the life of the asset.

C) the annual loss of value of buildings and machines due to deterioration.

D) the change in the weighted average cost of capital, or percentage change in the components of debt and equity.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

54

Figure 7.2.1Refer to Figure 7.2.1 above. When 7 units of output are produced:

A) average fixed cost reaches its minimum.

B) average total cost reaches its minimum.

C) average variable cost reaches its minimum.

D) marginal cost reaches its minimum.

E) all of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

55

Consider the following statements when answering this question: I. A firm's marginal cost curve does not depend on the level of fixed costs.

II) As output increases the difference between a firm's average total cost and average variable cost curves cannot rise.

A) I is true, and II is false.

B) I is false, and II is true.

C) I and II are both true.

D) I and II are both false.

II) As output increases the difference between a firm's average total cost and average variable cost curves cannot rise.

A) I is true, and II is false.

B) I is false, and II is true.

C) I and II are both true.

D) I and II are both false.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

56

A firm's total cost function is given by the equation:

TC = 4000 + 5Q + 10Q2.

(1) Write an expression for each of the following cost concepts:

a. Total Fixed Cost

b. Average Fixed Cost

c. Total Variable Cost

d. Average Variable Cost

e. Average Total Cost

f. Marginal Cost

(2) Determine the quantity that minimizes average total cost. Demonstrate that the predicted relationship between marginal cost and average cost holds.

TC = 4000 + 5Q + 10Q2.

(1) Write an expression for each of the following cost concepts:

a. Total Fixed Cost

b. Average Fixed Cost

c. Total Variable Cost

d. Average Variable Cost

e. Average Total Cost

f. Marginal Cost

(2) Determine the quantity that minimizes average total cost. Demonstrate that the predicted relationship between marginal cost and average cost holds.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

57

Which of the following costs are always increasing as output increases?

A) Marginal Cost only

B) Fixed Cost only

C) Total Cost only

D) Variable Cost only

E) Total Cost and Variable Cost

A) Marginal Cost only

B) Fixed Cost only

C) Total Cost only

D) Variable Cost only

E) Total Cost and Variable Cost

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

58

Consider the following statements when answering this question I. If a firm employs only one variable factor of production, labor, and the marginal product of labor is constant, then the marginal costs of production are constant too.

II) If a firm employs only one variable factor of production, labor, and the marginal product of labor is constant, then short-run average total costs cannot rise as output rises.

A) I is true, and II is false.

B) I is false, and II is true.

C) I and II are both true.

D) I and II are both false.

II) If a firm employs only one variable factor of production, labor, and the marginal product of labor is constant, then short-run average total costs cannot rise as output rises.

A) I is true, and II is false.

B) I is false, and II is true.

C) I and II are both true.

D) I and II are both false.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

59

If a factory has a short-run capacity constraint (e.g., an auto plant can only produce 800 cars per day at maximum capacity), the marginal cost of production becomes ________ at the capacity constraint.

A) infinite

B) zero

C) highly elastic

D) less than the average variable cost

A) infinite

B) zero

C) highly elastic

D) less than the average variable cost

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

60

From Equation (7.1) in the book, the short-run marginal cost of production is MC = w/MPL. Based on this equation, which of the following statements is NOT true?

A) If the marginal product of labor is constant, then MC is constant.

B) If the marginal product of labor is a concave curve, then the MC curve is also concave.

C) If the marginal product of labor is a concave curve, then the MC curve is U-shaped.

D) MC increases as the marginal product of labor declines.

A) If the marginal product of labor is constant, then MC is constant.

B) If the marginal product of labor is a concave curve, then the MC curve is also concave.

C) If the marginal product of labor is a concave curve, then the MC curve is U-shaped.

D) MC increases as the marginal product of labor declines.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

61

A plant uses machinery and waste water to produce steel. The owner of the plant wants to maintain an output of 10,000 tons a day, even though the government has just imposed a $100 per gallon tax on using waste water. The reduction in the amount of waste water that results from the imposition of this tax depends on:

A) the amount of waste water used before the tax was imposed.

B) the cost to the firm of using waste water before the tax was put in place.

C) the rental rate of machinery.

D) the marginal product of waste water only.

E) the ratio of the marginal product of waste water to the marginal product of machinery.

A) the amount of waste water used before the tax was imposed.

B) the cost to the firm of using waste water before the tax was put in place.

C) the rental rate of machinery.

D) the marginal product of waste water only.

E) the ratio of the marginal product of waste water to the marginal product of machinery.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

62

Which of the following is the user cost of capital per dollar of capital?

A) depreciation + interest rate

B) the user cost of capital

C) the opportunity cost of capital

D) all of the above

A) depreciation + interest rate

B) the user cost of capital

C) the opportunity cost of capital

D) all of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

63

The total cost of producing a given level of output is:

A) maximized when a corner solution exists.

B) minimized when the ratio of marginal product to input price is equal for all inputs.

C) minimized when the marginal products of all inputs are equal.

D) minimized when marginal product multiplied by input price is equal for all inputs.

A) maximized when a corner solution exists.

B) minimized when the ratio of marginal product to input price is equal for all inputs.

C) minimized when the marginal products of all inputs are equal.

D) minimized when marginal product multiplied by input price is equal for all inputs.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

64

Figure 7.3.2Refer to Figure 7.3.2 above. Which of the following changes, which causes the move from A to B?

A) The price of one of the inputs

B) the productivity of inputs

C) The quantity to be produced

D) The budget of the producer

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

65

An isocost line reveals the

A) costs of inputs needed to produce along an isoquant.

B) costs of inputs needed to produce along an expansion path.

C) input combinations that can be purchased for a given total cost.

D) output combinations that can be produced with a given outlay of funds.

A) costs of inputs needed to produce along an isoquant.

B) costs of inputs needed to produce along an expansion path.

C) input combinations that can be purchased for a given total cost.

D) output combinations that can be produced with a given outlay of funds.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

66

When an isocost line is just tangent to an isoquant, we know that:

A) output is being produced at minimum cost.

B) output is not being produced at minimum cost.

C) the two products are being produced at the least input cost to the firm.

D) the two products are being produced at the highest input cost to the firm.

A) output is being produced at minimum cost.

B) output is not being produced at minimum cost.

C) the two products are being produced at the least input cost to the firm.

D) the two products are being produced at the highest input cost to the firm.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

67

Figure 7.3.3Refer to Figure 7.3.3 above. The expansion path in the figure leads to the construction of:

A) a short run marginal cost curve.

B) a long run marginal cost curve.

C) a long run total cost curve.

D) a long run average total cost curve.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

68

A firm employs 100 workers at a wage rate of $10 per hour, and 50 units of capital at a rate of $21 per hour. The marginal product of labor is 3, and the marginal product of capital is 5. The firm:

A) is producing its current output level at the minimum cost.

B) could reduce the cost of producing its current output level by employing more capital and less labor.

C) could reduce the cost of producing its current output level by employing more labor and less capital.

D) could increase its output at no extra cost by employing more capital and less labor.

E) Both B and D are true.

A) is producing its current output level at the minimum cost.

B) could reduce the cost of producing its current output level by employing more capital and less labor.

C) could reduce the cost of producing its current output level by employing more labor and less capital.

D) could increase its output at no extra cost by employing more capital and less labor.

E) Both B and D are true.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

69

A firm's expansion path is:

A) the firm's production function.

B) a curve that makes the marginal product of the last unit of each input equal for each output.

C) a curve that shows the least-cost combination of inputs needed to produce each level of output for given input prices.

D) none of the above

A) the firm's production function.

B) a curve that makes the marginal product of the last unit of each input equal for each output.

C) a curve that shows the least-cost combination of inputs needed to produce each level of output for given input prices.

D) none of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

70

If the capital market is competitive, the user cost of capital equals:

A) the rental rate of capital.

B) the return in that market.

C) the rate of return of investing elsewhere.

D) all of the above.

A) the rental rate of capital.

B) the return in that market.

C) the rate of return of investing elsewhere.

D) all of the above.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

71

Assume that a firm spends $500 on two inputs, labor (graphed on the horizontal axis) and capital (graphed on the vertical axis). If the wage rate is $20 per hour and the rental cost of capital is $25 per hour, the slope of the isocost curve will be:

A) 500.

B) 25/500.

C) -4/5.

D) 25/20 or 1.25.

A) 500.

B) 25/500.

C) -4/5.

D) 25/20 or 1.25.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

72

Figure 7.3.1Refer to Figure 7.3.1 above. Which point on the graph shows the optimal combination of inputs?

A) Point A, when the production process is capital intensive

B) Point B

C) Point D, when the production process is capital intensive

D) All three points, A, B and D are optimal

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

73

In the long run, which of the following is considered a variable cost?

A) Expenditures for wages

B) Expenditures for research and development

C) Expenditures for raw materials

D) Expenditures for capital machinery and equipment

E) all of the above

A) Expenditures for wages

B) Expenditures for research and development

C) Expenditures for raw materials

D) Expenditures for capital machinery and equipment

E) all of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

74

Figure 7.3.4Refer to Figure 7.3.4 above. The long run cost curve comes from:

A) a map of isoquants.

B) a map of isocosts.

C) an expansion path.

D) an optimal combination of inputs for a given level of output.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

75

Suppose that the price of labor ( ) is $10 and the price of capital ( ) is $20. What is the equation of the isocost line corresponding to a total cost of $100?

A) PL + 20PK

B) 100 = 10L + 20K

C) 100 = 30(L+K)

D) 100 + 30

E) none of the above

) is $10 and the price of capital ( ) is $20. What is the equation of the isocost line corresponding to a total cost of $100?A) PL + 20PK

B) 100 = 10L + 20K

C) 100 = 30(L+K)

D) 100 + 30

E) none of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

76

Figure 7.3.4At the optimum combination of two inputs,

A) the slopes of the isoquant and isocost curves are equal.

B) costs are minimized for the production of a given output.

C) the marginal rate of technical substitution equals the ratio of input prices.

D) all of the above

E) A and C only

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

77

Which of the following is NOT an expression for the cost minimizing combination of inputs?

A) MRTS = MPL /MPK

B) MPL/w = MPK/r

C) MRTS = w/r

D) MPL/MPK = w/r

E) none of the above

A) MRTS = MPL /MPK

B) MPL/w = MPK/r

C) MRTS = w/r

D) MPL/MPK = w/r

E) none of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

78

With its current levels of input use, a firm's MRTS is 3 (when capital is on the vertical axis and labor is on the horizontal axis). This implies:

A) the firm could produce 3 more units of output if it increased its use of capital by one unit (holding labor constant).

B) the firm could produce 3 more units of output if it increased its use of labor by one unit (holding capital constant).

C) if the firm reduced its capital stock by one unit, it would have to hire 3 more workers to maintain its current level of output.

D) if it used one more unit of both capital and labor, the firm could produce 3 more units of output.

E) the marginal product of labor is 3 times the marginal product of capital.

A) the firm could produce 3 more units of output if it increased its use of capital by one unit (holding labor constant).

B) the firm could produce 3 more units of output if it increased its use of labor by one unit (holding capital constant).

C) if the firm reduced its capital stock by one unit, it would have to hire 3 more workers to maintain its current level of output.

D) if it used one more unit of both capital and labor, the firm could produce 3 more units of output.

E) the marginal product of labor is 3 times the marginal product of capital.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

79

A firm wants to minimize the total cost of producing 100 tons of dynamite. The firm uses two factors of production, chemicals and labor. The combination of chemicals and labor that minimizes production costs will be found where:

A) the marginal products of chemicals and labor are equal.

B) the ratio of the amount of chemicals used to the amount of labor used equals the ratio of the marginal product of chemicals to the marginal product of labor.

C) the ratio of the amount of chemicals used to the amount of labor used equals the ratio of the price of chemicals to the wage rate.

D) the production of an additional unit of dynamite costs the same regardless of whether chemicals or labor are used.

E) none of the above

A) the marginal products of chemicals and labor are equal.

B) the ratio of the amount of chemicals used to the amount of labor used equals the ratio of the marginal product of chemicals to the marginal product of labor.

C) the ratio of the amount of chemicals used to the amount of labor used equals the ratio of the price of chemicals to the wage rate.

D) the production of an additional unit of dynamite costs the same regardless of whether chemicals or labor are used.

E) none of the above

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

80

An effluent fee is imposed on a steel firm to reduce the amount of waste materials that it dumps in a river. Use the following two statements to answer this question: I. The more easily factors of production can be substituted for one another (for example, capital can be used to reduce waste water), the more effective the fee will be in reducing effluent.

II) The greater the degree of substitution of capital for waste water, the less the firm will have to pay in effluent fees.

A) Both I and II are true.

B) I is true, and II is false.

C) I is false, and II is true.

D) Both I and II are false.

II) The greater the degree of substitution of capital for waste water, the less the firm will have to pay in effluent fees.

A) Both I and II are true.

B) I is true, and II is false.

C) I is false, and II is true.

D) Both I and II are false.

Unlock Deck

Unlock for access to all 178 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 178 flashcards in this deck.