Multiple Choice

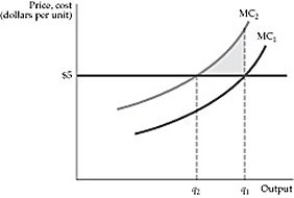

Figure 8.5.2

Figure 8.5.2

-Higher input prices result in:

A) upward shifts of MC and reductions in output.

B) upward shifts of MC and increases in output.

C) downward shifts of MC and reductions in output.

D) downward shifts of MC and increases in output.

E) increased demand for the good the input is used for.

Correct Answer:

Verified

Correct Answer:

Verified

Q99: In a constant-cost industry, price always equals:<br>A)

Q100: Although the long-run equilibrium price of oil

Q101: Firms often use patent rights as a:<br>A)

Q102: A few sellers may behave as if

Q103: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB3095/.jpg" alt=" Figure 8.5.1 -Refer

Q105: Suppose all firms have constant marginal costs

Q106: If a graph of a perfectly competitive

Q107: Suppose the state legislature in your state

Q108: Imposition of an output tax on all

Q109: If any of the assumptions of perfect