Multiple Choice

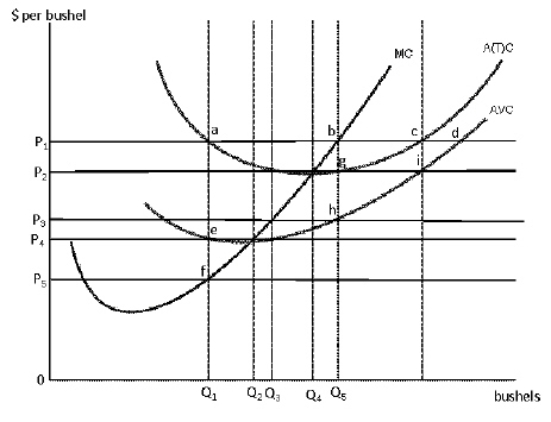

Exhibit 8-19 A Single Firm in a Perfectly Competitive Market  Consider Exhibit 8-19.When the market price is P1, which of the following most acurately reflects the firms short-run situation?

Consider Exhibit 8-19.When the market price is P1, which of the following most acurately reflects the firms short-run situation?

A) The firm will choose to produce quantity Q5 and earn exactly 0 profit

B) The firm will choose to produce quantity Q5 and earn a profit

C) The firm will choose to produce quantity Q5 and suffer a loss

D) The firm will choose to produce quantity Q1 and earn a profit > 0

E) The firm will choose to produce quantity Q1 and earn exactly 0 profit

Correct Answer:

Verified

Correct Answer:

Verified

Q19: Suppose a perfectly competitive increasing-cost industry is

Q20: In the short run, if a firm

Q21: Suppose that, in the short run, a

Q22: Firms in perfect competition will leave the

Q23: When marginal revenue equals marginal cost, the

Q25: If new firms enter a perfectly competitive

Q26: If a market is productively efficient,<br>A)the output

Q27: Exhibit 8-19 A Single Firm in a

Q28: In the long run, a perfectly competitive

Q29: Suppose the equilibrium price in a perfectly