Multiple Choice

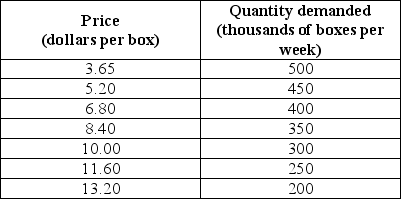

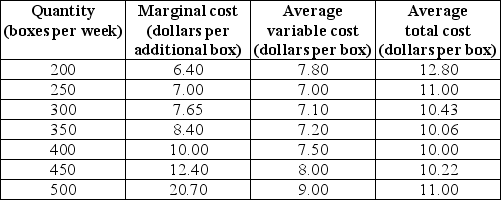

Use the table below to answer the following question.

Table 11.4.1

-Refer to Table 11.4.1.The top table shows the market demand schedule for paper.The market is perfectly competitive and there are 1,000 firms that produce paper.Each firm has the costs shown in the bottom table when it uses its least-cost plant.The market price in the long run is ________ a box and the equilibrium quantity produced in the long run is ________ boxes a week.

A) $11.60;250,000

B) $10.00;400,000

C) $10.00;300,000

D) $6.40;a little more than 400,000

E) $8.40;350,000

Correct Answer:

Verified

Correct Answer:

Verified

Q43: If a firm faces a perfectly elastic

Q44: Technological change<br>A)brings only temporary gains to producers.<br>B)brings

Q45: Use the information below to answer the

Q46: If a perfectly competitive firm's marginal revenue

Q47: Which one of the following does not

Q49: Use the table below to answer the

Q50: If a perfectly competitive firm is producing

Q51: Use the information below to answer the

Q52: Economic profit equals<br>A)total fixed cost plus total

Q53: A decrease in demand brings all of