Multiple Choice

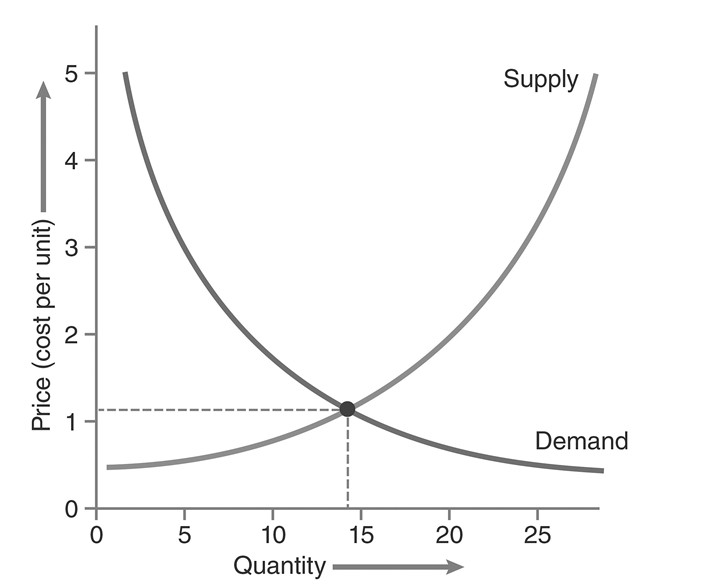

-The intersection of the two lines on the graph represents_________ .

A) the convergence point,which is the point at which the supply and demand curves converge

B) the equilibrium point,which is the price at which consumers are willing to pay given the quantity that producers are willing to make

C) the convergence point,which is the quantity that consumers will buy when the product costs a certain amount

D) the equilibrium point,which is the quantity of product a manufacturer is willing to produce in a declining economy

Correct Answer:

Verified

Correct Answer:

Verified

Q14: Someone presenting a deontological argument for not

Q15: In a developing country experiencing rapid economic

Q16: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB5135/.jpg" alt=" -This graph illustrates_

Q17: Both the gross domestic product GDP)and genuine

Q18: In 1968,an ecologist named Garrett Hardin published

Q20: Someone with an_ perspective might argue that

Q21: The GDP of the United States _.<br>A)includes

Q22: Which of the following is a tenet

Q23: Externalities include_ .<br>A)the costs of raw materials<br>B)worker's

Q24: Discount rates are used to determine the_