Short Answer

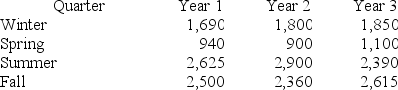

Consider the following set of quarterly sales data, given in thousands of dollars.

The following dummy variable model that incorporates a linear trend and constant seasonal variation was used: y(t) = β0 + β1t + βQ1(Q1) + βQ2(Q2) + βQ3(Q3) + Et. In this model, there are three binary seasonal variables (Q1, Q2, and Q3), where Qi is a binary (0,1) variable defined as:

The following dummy variable model that incorporates a linear trend and constant seasonal variation was used: y(t) = β0 + β1t + βQ1(Q1) + βQ2(Q2) + βQ3(Q3) + Et. In this model, there are three binary seasonal variables (Q1, Q2, and Q3), where Qi is a binary (0,1) variable defined as:

Qi = 1, if the time series data is associated with quarter i;

Qi = 0, if the time series data is not associated with quarter i.

The results associated with this data and model are given in the following Minitab computer output.

The regression equation is

Sales = 2442 + 6.2 Time − 693 Q1 − 1499 Q2 + 153 Q3

Analysis of Variance

Analysis of Variance

At α = .05, test the significance of the model.

At α = .05, test the significance of the model.

Correct Answer:

Verified

Reject H0, the model is significant and a...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q12: The price and quantity of several food

Q13: Consider the following data.<br> <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB7056/.jpg" alt="Consider

Q14: Use the following price information for three

Q15: XYZ Company, Annual Data <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB7056/.jpg" alt="XYZ

Q16: Seasonal variations are periodic patterns in a

Q18: Consider the regression equation <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB7056/.jpg" alt="Consider

Q19: A simple index is obtained by dividing

Q20: Assume that the current date is February

Q21: The linear regression trend model was applied

Q22: The demand for a product for the