Multiple Choice

What are the names of the following models?

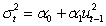

(I)  (II)

(II)  (III)

(III)  (IV)

(IV)

A) GARCH (1) , ARCH (1,1) , GARCH(q) and ARCH(p,q) , respectively

B) ARCH(1) , GARCH(1,1) , ARCH(q) and GARCH(p,q) , respectively

C) ARCH(1) , EGARCH(1,1) , ARCH(q) and EGARCH(p,q) , respectively

D) EGARCH (1) , ARCH(1,1) , EGARCH (q) and ARCH(p,q) , respectively

Correct Answer:

Verified

Correct Answer:

Verified

Q9: Which of these is an appropriate technique

Q10: Volatility clustering is<br>A) The tendency for financial

Q11: Suppose that a researcher wanted to obtain

Q12: Suppose that a researcher estimates a GARCH(1,1)

Q13: Which of the following are NOT features

Q14: Which of the following would represent the

Q16: What are the steps required to estimate

Q17: Consider the three approaches to conducting hypothesis

Q18: <br>-Which of the following statements are true

Q19: GJR and EGARCH are types of GARCH