Multiple Choice

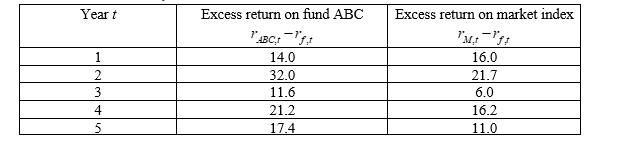

Suppose you have 5-year annual data on the excess returns on a fund manager’s portfolio (“fund ABC”) and the excess returns on a market index (where  is the return on fund ABC,

is the return on fund ABC,  is the risk-free rate and

is the risk-free rate and  is the return on the market index) :

is the return on the market index) :

-The estimated alpha (  ) and beta (

) and beta (  ) of a rival fund, Fund DEF, are 2.3 and 3.1, respectively. If the expected market risk premium is 12%, what would we expect the excess return of Fund DEF to be?

) of a rival fund, Fund DEF, are 2.3 and 3.1, respectively. If the expected market risk premium is 12%, what would we expect the excess return of Fund DEF to be?

A) 39.5%

B) 30.7%

C) 5.4%

D) 64.8%

Correct Answer:

Verified

Correct Answer:

Verified

Q3: Which of the following is the most

Q4: Consider an increase in the size of

Q5: Suppose you have calculated the following regression

Q6: What does a positive linear relationship between

Q7: Which of the following statements is correct

Q9: Regression is concerned with describing and evaluating

Q10: The type I error associated with testing

Q11: What is the relationship, if any, between

Q12: Which of the following is NOT correct

Q13: Assuming there are 1000 observations in your