Multiple Choice

The following questions are based on the problem below.

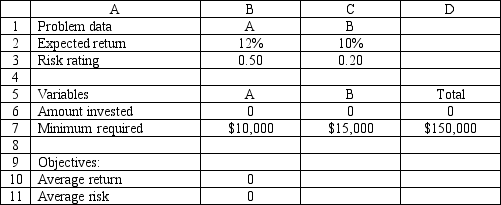

An investor has $150,000 to invest in investments A and B. Investment A requires a $10,000 minimum investment, pays a return of 12% and has a risk factor of .50. Investment B requires a $15,000 minimum investment, pays a return of 10% and has a risk factor of .20. The investor wants to maximize the return while minimizing the risk of the portfolio. The following multi-objective linear programming (MOLP) has been solved in Excel.

-Refer to Exhibit 7.2. What Risk Solver Platform (RSP) constraint involves cells $B$6:$C$6?

A) $B$6:$C$6=$B$7:$C$7

B) $B$6:$C$6 $B$7:$C$7

C) $B$6:$C$6 $B$7:$C$7

D) $B$6:$C$6=$D$7

Correct Answer:

Verified

Correct Answer:

Verified

Q7: Exhibit 7.1<br>The following questions are based on

Q8: Exhibit 7.1<br>The following questions are based on

Q16: A constraint which cannot be violated is

Q20: The RHS value of a goal constraint

Q27: Exhibit 7.2<br>The following questions are based on

Q34: The MINIMAX objective<br>A) yields the smallest possible

Q44: An investor wants to invest $50,000 in

Q48: Decision-making problems which can be stated as

Q50: Exhibit 7.3<br>The following questions are based on

Q62: Which of the following is true regarding