Multiple Choice

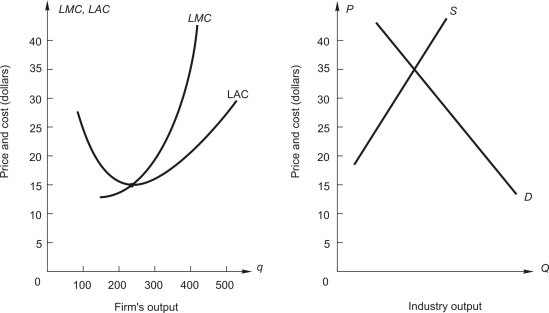

Refer to the following figure:

The graph on the left shows long-run average and marginal cost for a typical firm in a perfectly competitive industry. The graph on the right shows demand and long-run supply for an increasing-cost industry.

-If this were a constant-cost industry, what would be the price when the industry gets to long-run competitive equilibrium?

A) between $35 and $20

B) $35

C) $20

D) below $20

E) above $35

Correct Answer:

Verified

Correct Answer:

Verified

Q4: a perfectly competitive market<br>A)a firm must lower

Q40: Refer to the following:<br>Consider a competitive

Q41: Use the following data for

Q42: Refer to the following:<br>Consider a competitive

Q43: Use the following data for a

Q43: An industry is in long-run competitive equilibrium.The

Q44: Refer to the following:<br>Total cost schedule

Q47: Refer to the following:<br>A consulting company

Q49: Use the following information to answer

Q74: In order to minimize losses in the