Multiple Choice

Use the following to answer question:

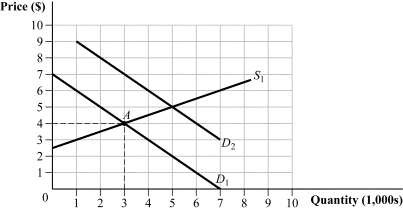

Figure 8.17

-(Figure 8.17) Initially, the constant-cost industry was in long-run equilibrium at point A when the demand for the good increased to D2. How much output will be produced in the long run as a result of the demand increase?

A) 3,000

B) 5,000

C) 6,000

D) 7,000

Correct Answer:

Verified

Correct Answer:

Verified

Q49: To maximize profits, a firm should produce

Q62: In the market for lock washers, a

Q77: Use the following to answer question:<br>Figure 8.3

Q80: Suppose that the perfectly competitive market for

Q81: Suppose that the market for gourmet deli

Q87: Use the following to answer question:<br>Figure 8.7

Q101: Explain what will happen in each of

Q103: If the long-run total cost curve for

Q104: A perfectly competitive industry consists of 500

Q108: In a perfectly competitive market, each firm