Essay

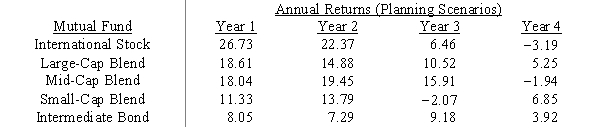

Investment manager Max Gaines wishes to develop a mutual fund portfolio based on the Markowitz portfolio model. He needs to determine the proportion of the portfolio to invest in each of the five mutual funds listed below so that the variance of the portfolio is minimized subject to the constraint that the expected return of the portfolio be at least 4%. Formulate the appropriate nonlinear program.

Correct Answer:

Verified

IS = proportion of portfolio invested in...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q3: The interpretation of the dual price for

Q16: The function f (X,Y)= X <sup>2</sup> +

Q17: Financial planner Minnie Margin has a substantial

Q18: Which of the following is incorrect?<br>A) A

Q20: When the number of blending components exceeds

Q21: The key idea behind constructing an index

Q24: Discuss the essence of the pooling problem

Q28: Native Customs sells two popular styles of

Q29: In the Bass model for forecasting the

Q32: Functions that are convex have a single