Multiple Choice

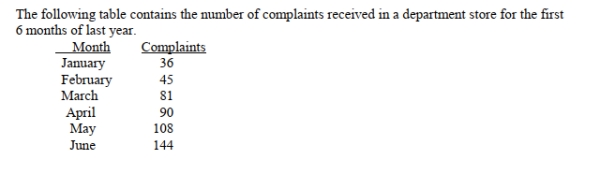

SCENARIO 16-3

-Referring to Scenario 16-3, suppose the last two smoothed values are 81 and 96 (Note: they

Are not) .What would you forecast as the value of the time series for September?

A) 81

B) 86

C) 91

D) 96

Correct Answer:

Verified

Correct Answer:

Verified

Q13: True or False: A least squares linear

Q14: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB2675/.jpg" alt=" " class="answers-bank-image d-block" rel="preload"

Q16: True or False: In selecting a forecasting

Q17: True or False: MAD is the summation

Q19: True or False: Each forecast using the

Q20: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB2675/.jpg" alt=" " class="answers-bank-image d-block" rel="preload"

Q22: SCENARIO 16-3 <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB2675/.jpg" alt="SCENARIO 16-3

Q23: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB2675/.jpg" alt=" " class="answers-bank-image d-block" rel="preload"

Q32: The method of least squares is used

Q109: The method of moving averages is used<br>A)to