Multiple Choice

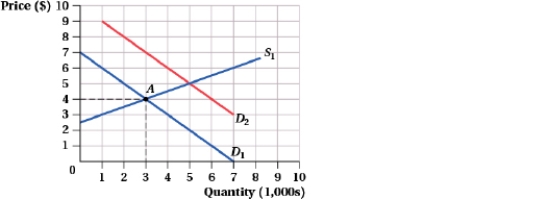

(Figure: Long Run Output I) Initially, the constant-cost industry was in long-run equilibrium at point A when the demand for the good increased to D2. How much output will be produced in the long run as a result of the demand increase?

A) 3,000

B) 5,000

C) 6,000

D) 7,000

Correct Answer:

Verified

Correct Answer:

Verified

Q33: Suppose that a perfectly competitive firm's AVC

Q34: Suppose that the market for painting services

Q35: Suppose that the market for ice cream

Q36: Suppose that the market for painting services

Q37: Suppose the long-run equilibrium price in a

Q39: Use the following table to answer the

Q40: A perfectly competitive firm maximizes profit by

Q41: Suppose that a firm is producing where

Q42: Suppose that the market for ice cream

Q43: Suppose that the market for painting services