Short Answer

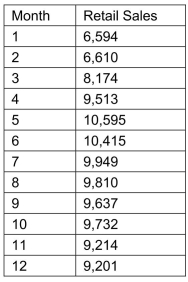

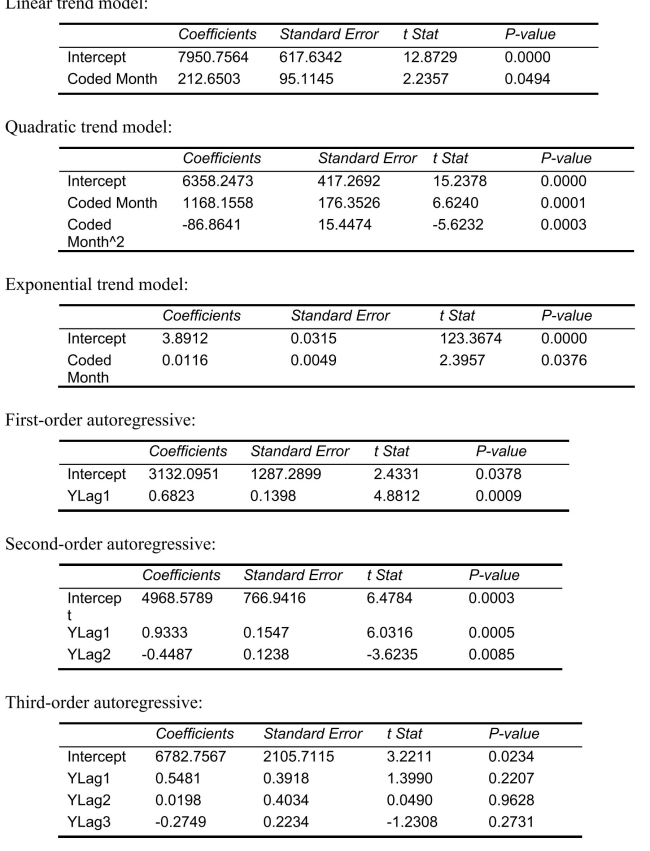

SCENARIO 16-13 Given below is the monthly time series data for U.S.retail sales of building materials over a specific year.  The results of the linear trend, quadratic trend, exponential trend, first-order autoregressive, second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the

The results of the linear trend, quadratic trend, exponential trend, first-order autoregressive, second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the  month is 0:

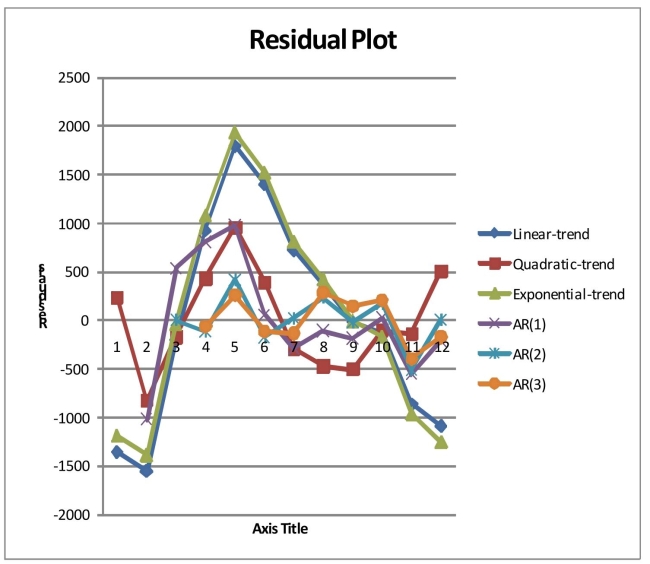

month is 0:  Below is the residual plot of the various models:

Below is the residual plot of the various models:

-Referring to Scenario 16-13, what is the exponentially smoothed value for the 1  month using a smoothing coefficient of W = 0.25 if the exponentially smoothed value for the 1

month using a smoothing coefficient of W = 0.25 if the exponentially smoothed value for the 1  and

and  month are 9,477.7776 and 9,411.8332, respectively?

month are 9,477.7776 and 9,411.8332, respectively?

Correct Answer:

Verified

Correct Answer:

Verified

Q1: SCENARIO 16-6<br>The president of a chain of

Q14: After estimating a trend model for annual

Q15: SCENARIO 16-13 Given below is the monthly

Q16: SCENARIO 16-11 The manager of a health

Q19: SCENARIO 16-13 Given below is the monthly

Q21: SCENARIO 16-13 Given below is the monthly

Q52: The overall upward or downward pattern of

Q58: SCENARIO 16-13<br>Given below is the monthly time

Q121: SCENARIO 16-13<br>Given below is the monthly time

Q154: SCENARIO 16-8<br>The manager of a marketing consulting