Multiple Choice

Exhibit 10-2 A monopolistic competitive firm

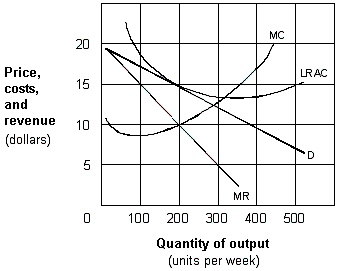

Comparing the firms in a monopolistic competitive industry shown in Exhibit 10-2 to a perfectly competitive firm in long-run equilibrium, we find that both firms

A) choose a price equal to the marginal cost at the profit-maximizing quantity.

B) will experience entry of new firms into the industry.

C) earn zero economic profits.

D) minimize cost per unit at their profit-maximizing quantity.

Correct Answer:

Verified

Correct Answer:

Verified

Q30: Suppose that R. J. Reynolds raises the

Q31: While there is no specific number of

Q32: Exhibit 10-1 A monopolistic competitive firm<br><img src="https://d2lvgg3v3hfg70.cloudfront.net/TBX8793/.jpg"

Q33: Under which one of the following market

Q34: In the long run, monopolistically competitive firms

Q36: A market situation where a small number

Q37: The markets for Products X and Y

Q38: In order to make oil profits as

Q39: Exhibit 10-2 A monopolistic competitive firm<br><img src="https://d2lvgg3v3hfg70.cloudfront.net/TBX8793/.jpg"

Q40: A kink in the demand curve facing