Multiple Choice

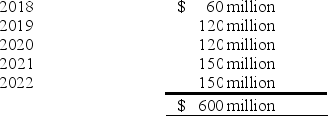

Isaac Inc. began operations in January 2018. For certain of its property sales, Isaac recognizes income in the period of sale for financial reporting purposes. However, for income tax purposes, Isaac recognizes income when it collects cash from the buyer's installment payments. In 2018, Isaac had $600 million in sales of this type. Scheduled collections for these sales are as follows:  Assume that Isaac has a 30% income tax rate and that there were no other differences in income for financial statement and tax purposes.

Assume that Isaac has a 30% income tax rate and that there were no other differences in income for financial statement and tax purposes.

Suppose that, in 2019, legislation revised the income tax rates so that Isaac would be taxed in 2020 and beyond at 40%, rather than 30%. Assume that there were no other differences in income for financial statement and tax purposes.

-Ignoring operating expenses and additional sales in 2019, what deferred tax liability would Isaac report in its year-end 2019 balance sheet?

A) $168 million.

B) $144 million.

C) $126 million.

D) $240 million.

Correct Answer:

Verified

Correct Answer:

Verified

Q88: In its 2018 annual report to shareholders,

Q89: Which of the following circumstances creates a

Q90: Listed below are 5 terms followed by

Q91: A reconciliation of pretax financial statement income

Q92: The following information relates to Franklin Freightways

Q94: Under current tax law a net operating

Q95: At the end of the preceding year,

Q96: Expenditures currently deducted in the tax return

Q97: A magazine publisher collects one year in

Q98: Puritan Corp. reported the following pretax