Essay

THE NEXT QUESTIONS ARE BASED ON THE FOLLOWING INFORMATION:

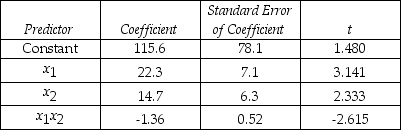

An economist is in the process of developing a model to predict the price of gold.She believes that the two most important variables are the price of a barrel of oil (x1)and the interest rate (x2).She proposes the model y = β0 + β1x1 + β2x2 + β3x1x3 + ε.A random sample of 20 daily observations was taken.The computer output is shown below.

THE REGRESSION EQUATION IS

y = 115.6 + 22.3x1 + 14.7x2 - 1.36x1x2

S = 20.9 R-Sq = 55.4%

ANALYSIS OF VARIANCE

-Do these results allow us,at the 5% significance level,to conclude that the model is useful in predicting the price of gold?

Correct Answer:

Verified

H0 : β1 = β2 = β3 = 0 vs.H1 : At least one β1 i...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q158: Suppose we estimate the regression Y<sub>t</sub> =

Q159: Why is it so important to understand

Q160: If the independent variables in a regression

Q161: If the Durbin-Watson statistic d has values

Q162: Briefly discuss approaches that can be employed

Q163: THE NEXT QUESTIONS ARE BASED ON THE

Q165: Consider the following plot of residuals from

Q166: THE NEXT QUESTIONS ARE BASED ON THE

Q167: THE NEXT QUESTIONS ARE BASED ON THE

Q168: Write the model specification and define the