Multiple Choice

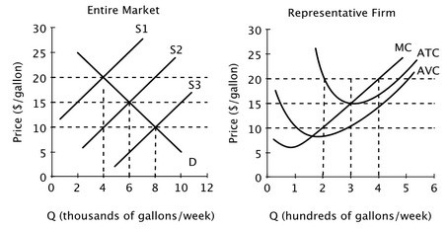

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  In the long run, the equilibrium price will be ________ per gallon, and each firm's profit-maximizing quantity will be ________ gallons per week.

In the long run, the equilibrium price will be ________ per gallon, and each firm's profit-maximizing quantity will be ________ gallons per week.

A) $20; 400

B) $15; 6,000

C) $15; 300

D) $20; 4,000

Correct Answer:

Verified

Correct Answer:

Verified

Q109: Which of the following statements about explicit

Q110: The phrase "smart for one, but dumb

Q111: Refer to the figure below. <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB6547/.jpg"

Q112: Free entry and exit of firms is

Q113: Which of the following statements about implicit

Q115: Economic rent is:<br>A)the amount people pay for

Q116: Which of the following statements is true?<br>A)Accounting

Q117: Last year Christine worked as a consultant.

Q118: Generally, _ motivates firms to enter an

Q119: Assume that all firms in this industry