Multiple Choice

The condition for optimal portfolio choice can be represented by:

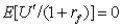

A)

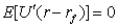

B)

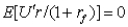

C)

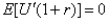

D)

Correct Answer:

Verified

Correct Answer:

Verified

Related Questions

Q2: A risk-averse individual is offered a gamble

Q3: Risk aversion is best explained by:<br>A)timidness.<br>B)increasing marginal

Q4: Suppose a person's utility of wealth is

Q5: An individual will never buy complete insurance

Q6: More risk-averse people will:<br>A)hold fewer risky assets

Q8: Which of the following utility functions exhibits

Q9: The formula for the Pratt measure of

Q10: Risk-averse individuals will diversify their investments because

Q11: People who always choose not to participate

Q12: An option may add value to a