Multiple Choice

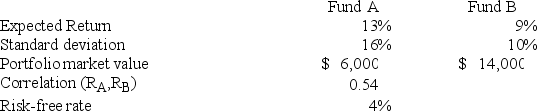

A portfolio consists of the following two funds.  What is the Sharpe ratio of the portfolio?

What is the Sharpe ratio of the portfolio?

A) 0.39

B) 0.45

C) 0.52

D) 0.60

E) 0.64

Correct Answer:

Verified

Correct Answer:

Verified

Related Questions

Q34: A portfolio has a 3-year standard deviation

Q35: Trailer Co.stock has an expected return of

Q36: Which measure would you use to know

Q38: A portfolio has a variance of 0.031050,a

Q40: The one-year standard deviation of your portfolio

Q44: You want to create the best portfolio

Q52: A Sharpe-optimal portfolio provides which one of

Q61: Which one of the following is a

Q78: The Sharpe ratio is best used to

Q83: Which of the following measures are dependent