Multiple Choice

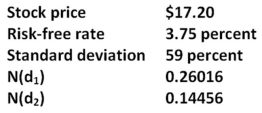

What is the value of a 6-month call with a strike price of $25 given the Black-Scholes option pricing model and the following information?

A) $0

B) $0.93

C) $1.06

D) $1.85

E) $2.14

Correct Answer:

Verified

Correct Answer:

Verified

Related Questions

Q38: For the equity of a firm to

Q68: Explain how an increase in T-bill rates

Q69: The Black-Scholes option pricing model can be

Q70: A decrease in which of the following

Q71: What is the value of a 6-month

Q72: Which of the following statements are correct?<br>I.Increasing

Q74: Given the following information,what is the value

Q75: Which one of the following statements related

Q76: Under European put-call parity,the present value of

Q78: The delta of a call option on