Multiple Choice

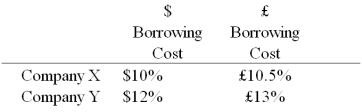

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow £5,000,000 fixed for 5 years.The exchange rate is $2 = £1 and is not expected to change over the next 5 years.Their external borrowing opportunities are:  A swap bank wants to design a profitable interest-only fixed-for-fixed currency swap.In order for X and Y to be interested,they can face no exchange rate risk

A swap bank wants to design a profitable interest-only fixed-for-fixed currency swap.In order for X and Y to be interested,they can face no exchange rate risk  What must the values of A and B in the graph shown above be in order for the swap to be of interest to firms X and Y?

What must the values of A and B in the graph shown above be in order for the swap to be of interest to firms X and Y?

A) A = $10.50%; B = £12%.

B) A = $10%; B = £13%.

C) A = $12%; B = £13%.

D) A = £10.50%; B = $12%.

Correct Answer:

Verified

Correct Answer:

Verified

Q3: Floating for floating currency swaps<br>A)the reference rates

Q10: Consider the dollar- and euro-based borrowing opportunities

Q12: Devise a direct swap for A and

Q14: When a swap bank serves as a

Q23: Explain how firm B could use two

Q52: Pricing a currency swap after inception involves<br>A)finding

Q71: Explain how firm A could use the

Q77: Company X and company Y have mirror-image

Q82: When an interest-only swap is established on

Q95: An interest-only single currency interest rate swap<br>A)is