Multiple Choice

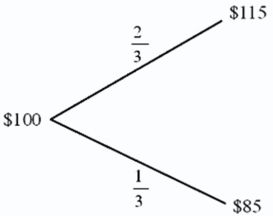

Find the value of a call option written on €100 with a strike price of $1.00 = €1.00.In one period,there are two possibilities: the exchange rate will move up by 15 percent or down by 15 percent .The U.S.risk-free rate is 5 percent over the period.The risk-neutral probability of dollar depreciation is 2/3 and the risk-neutral probability of the dollar strengthening is 1/3.

A) $9.5238

B) $0.0952

C) $0

D) $3.1746

Correct Answer:

Verified

Correct Answer:

Verified

Q72: Find the input d<sub>1</sub> of the Black-Scholes

Q73: Empirical tests of the Black-Scholes option pricing

Q74: Exercise of a currency futures option results

Q75: For an American call option,A and B

Q76: Comparing "forward" and "futures" exchange contracts,we can

Q79: Consider this graph of a call option.The

Q80: Consider an option to buy £10,000

Q81: Consider an option to buy €12,500

Q82: The current spot exchange rate is $1.55

Q91: For European currency options written on euro