Multiple Choice

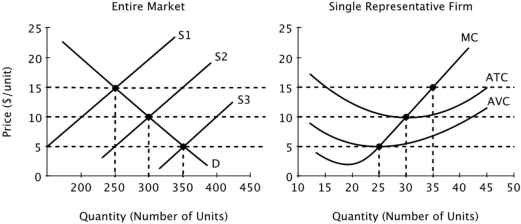

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  If the market supply curve is given by S3, then in the long run firms will:

If the market supply curve is given by S3, then in the long run firms will:

A) exit the market, leading the market supply curve to shift back to S2.

B) exit the market, leading the market supply curve to shift back to S1.

C) enter the market, leading the market supply curve to shift back to S2.

D) neither enter nor exit the market, so the market supply curve will remain at S3.

Correct Answer:

Verified

Correct Answer:

Verified

Q13: A market equilibrium is only efficient if:<br>A)the

Q17: In perfectly competitive markets, an implication of

Q19: Assume that all firms in this industry

Q21: Refer to the figure below. <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB3719/.jpg"

Q22: An example of an implicit cost is:<br>A)interest

Q40: The cumulative difference between the price producers

Q83: The role that prices play in directing

Q110: The phrase "smart for one, but dumb

Q121: If all firms in a perfectly competitive

Q140: The allocative function of price is to:<br>A)distribute