Multiple Choice

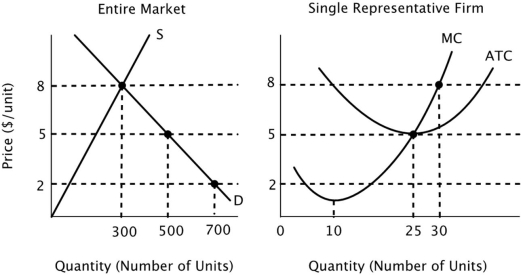

The figure below depicts the short-run market equilibrium in a perfectly competitive market and the cost curves for a representative firm in that market. Assume that all firms in this market have identical cost curves.  In the long run equilibrium in this market:

In the long run equilibrium in this market:

A) price will equal $5, and there will be 20 firms in the industry.

B) price will equal $5, and there will be 10 firms in the industry.

C) price will equal $8, and there will be 20 firms in the industry.

D) price will equal $5 and total output will equal 500 units, but there is not enough information to determine how many firms will be in the industry.

Correct Answer:

Verified

Correct Answer:

Verified

Q14: The sum of producer surplus and consumer

Q38: Superstar professional athletes can sustain their economic

Q50: The supplier of a factor of production

Q58: In a perfectly competitive market, if supply

Q89: Suppose the market for coffee is in

Q118: Generally, _ motivates firms to enter an

Q144: Suppose a small island nation imports sugar

Q147: Mary Jane is willing to babysit for

Q147: Assume that all firms in this industry

Q148: Entry into a perfectly competitive industry to