Multiple Choice

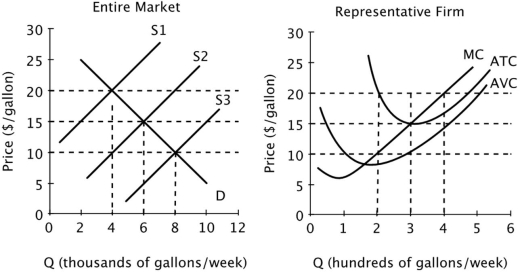

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  If the market supply curve is given by S3, then we would expect firms to:

If the market supply curve is given by S3, then we would expect firms to:

A) exit the market in the long run.

B) enter the market in the long run.

C) neither exit nor enter the market in the long run.

D) shut down in the short run.

Correct Answer:

Verified

Correct Answer:

Verified

Q4: Explicit costs:<br>A)measure the opportunity costs of the

Q15: Unlike economic profit, economic rent:<br>A)can be less

Q27: In the long run, in a perfectly

Q32: Professor Plum, who earns $100,000 per year,

Q33: Adam Smith's theory of the invisible hand

Q53: Efficiency is an important goal because when

Q116: Refer to the figure below. <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB3719/.jpg"

Q119: The figure below shows the supply and

Q121: Refer to the figure below. <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB3719/.jpg"

Q148: If there is excess demand in a