Multiple Choice

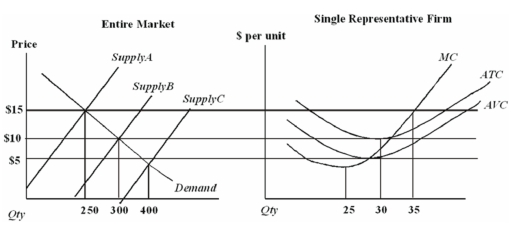

Assume that all firms in this industry have identical cost functions.

The long-run equilibrium price in this industry is

A) $15.

B) $10.

C) $5.

D) $5 for some firms and $10 for others.

Correct Answer:

Verified

Correct Answer:

Verified

Related Questions

Q101: If the demand curve fails to capture

Q102: Daily Supply and Demand: Oranges in Hurricane

Q103: Which of the following is NOT guaranteed

Q104: The following graphs depict a perfectly competitive

Q105: A market equilibrium is only efficient when:<br>A)buyers

Q107: Assume that all firms in this industry

Q108: Daily Supply and Demand: Oranges in Hurricane

Q109: Barriers to entry are _,and one effect

Q110: Suppose that a firm is located along

Q111: An implication of entry and exit in