Multiple Choice

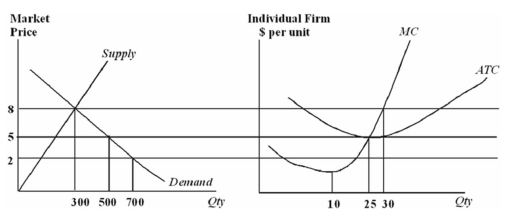

The following graphs depict a perfectly competitive firm and its market.

Assume that all firms in this industry have identical cost functions.

In the long run equilibrium in this market,

A) price will equal $5,and there will be 20 firms in the industry.

B) price will equal $5,and there will be 10 firms in the industry.

C) price will equal $8,and there will be 20 firms in the industry.

D) price will equal $5 and total output will equal 500 units,but there is not enough information to know how many firms there will be.

Correct Answer:

Verified

Correct Answer:

Verified

Q32: Accounting profits minus implicit costs equals:<br>A)total revenues.<br>B)economic

Q33: Last year Pat was a soybean farmer

Q34: If resources are currently misallocated in a

Q35: If an individual producer is willing to

Q36: The argument that efficiency is an appropriate

Q38: If a single firm,belonging to a perfectly

Q39: Chris was the business manager for a

Q40: Last year Pat was a soybean farmer

Q41: The economic theory of business behavior assumes

Q42: Generally,_ motivate firms to enter an industry