Multiple Choice

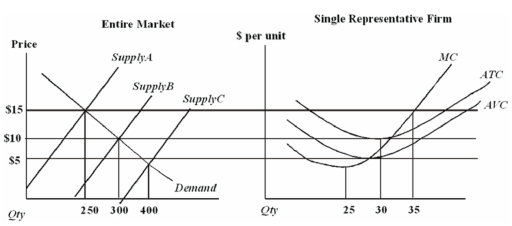

Assume that all firms in this industry have identical cost functions.

The long-run equilibrium price in this industry is

A) $15.

B) $10.

C) $5.

D) $5 for some firms and $10 for others.

Correct Answer:

Verified

Correct Answer:

Verified

Related Questions

Q8: In a perfectly competitive industry over the

Q15: Suppose you quit your job to start

Q16: Which of the following statements illustrates the

Q32: Daily Supply and Demand: Oranges in Hurricane

Q34: Daily Supply and Demand: Oranges in Hurricane

Q45: According to the textbook,individual incentives have led

Q50: Excess demand in a market is evidence

Q69: Consumer surplus is the value of:<br>A)consumer spending

Q75: Suppose a market is in equilibrium.The area

Q112: Duke is a particularly highly skilled negotiator.The