Multiple Choice

Use the following to answer question(s) :

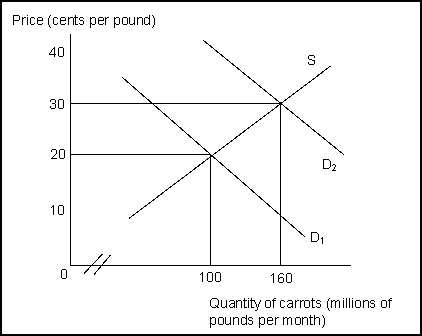

Exhibit: The Market for Carrots

-(Exhibit: The Market for Carrots) If this is a perfectly competitive market, which of the following is true?

A) The supply curve is linear and is determined by average total cost.

B) The equilibrium price and output are determined by demand and supply.

C) Each firm in this market is a price setter.

D) The price is too high.

Correct Answer:

Verified

Correct Answer:

Verified

Q198: If P > ATC the firm will

Q199: If price falls below the minimum of

Q200: The slope of the total revenue curve

Q201: Use the following to answer question(s): <br>Exhibit:

Q202: The supply curve for the firm in

Q204: A firm's total output times the price

Q205: Use the following to answer question(s): <br>Exhibit:

Q207: In the long run, provided that there

Q208: A decrease in production costs for firms

Q351: Provided that there are no external benefits