Multiple Choice

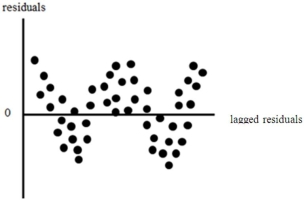

Suppose that you plot the residuals from a regression of GDP on the unemployment rate and you get the following

You would conclude that the error terms are

A) definitely autocorrelated.

B) likely not autocorrelated.

C) possibly autocorrelated and you would perform a formal test for autocorrelation.

D) possibly autocorrelated and you would perform a correction for heteroskedasticity.

Correct Answer:

Verified

Correct Answer:

Verified

Q12: Autoregressive error terms are potentially problematic because

Q13: How do you perform Prais-Winsten method for

Q14: If positive autocorrelation is not present,then the

Q15: You can determine whether a unit root

Q16: Suppose that you plot the residuals from

Q18: A simple method for determining whether autocorrelation

Q19: Conintegration is<br>A)an iterative process for removing a

Q20: Suppose you are interested in explaining

Q21: How do you perform the Durbin-Watson test

Q22: The final step of the Regression test