Essay

Case Study Short Essay Examination Questions

"Grave Dancer" Takes Tribune Corporation Private in an Ill-Fated Transaction

At the closing in late December 2007, well-known real estate investor Sam Zell described the takeover of the Tribune Company as "the transaction from hell." His comments were prescient in that what had appeared to be a cleverly crafted, albeit highly leveraged, deal from a tax standpoint was unable to withstand the credit malaise of 2008. The end came swiftly when the 161-year-old Tribune filed for bankruptcy on December 8, 2008.

On April 2, 2007, the Tribune Corporation announced that the firm's publicly traded shares would be acquired in a multistage transaction valued at $8.2 billion. Tribune owned at that time 9 newspapers, 23 television stations, a 25% stake in Comcast's SportsNet Chicago, and the Chicago Cubs baseball team. Publishing accounts for 75% of the firm's total $5.5 billion annual revenue, with the remainder coming from broadcasting and entertainment. Advertising and circulation revenue had fallen by 9% at the firm's three largest newspapers (Los Angeles Times, Chicago Tribune, and Newsday in New York) between 2004 and 2006. Despite aggressive efforts to cut costs, Tribune's stock had fallen more than 30% since 2005.

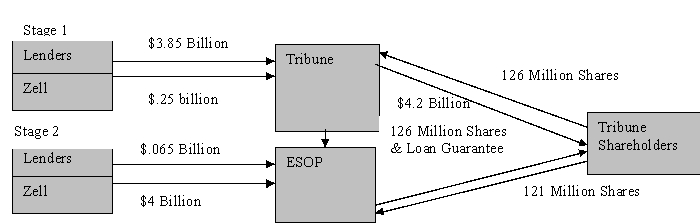

The transaction was implemented in a two-stage transaction, in which Sam Zell acquired a controlling 51% interest in the first stage followed by a backend merger in the second stage in which the remaining outstanding Tribune shares were acquired. In the first stage, Tribune initiated a cash tender offer for 126 million shares (51% of total shares) for $34 per share, totaling $4.2 billion. The tender was financed using $250 million of the $315 million provided by Sam Zell in the form of subordinated debt, plus additional borrowing to cover the balance. Stage 2 was triggered when the deal received regulatory approval. During this stage, an employee stock ownership plan (ESOP) bought the rest of the shares at $34 a share (totaling about $4 billion), with Zell providing the remaining $65 million of his pledge. Most of the ESOP's 121 million shares purchased were financed by debt guaranteed by the firm on behalf of the ESOP. At that point, the ESOP held all of the remaining stock outstanding valued at about $4 billion. In exchange for his commitment of funds, Mr. Zell received a 15-year warrant to acquire 40% of the common stock (newly issued) at a price set at $500 million.

Following closing in December 2007, all company contributions to employee pension plans were funneled into the ESOP in the form of Tribune stock. Over time, the ESOP would hold all the stock. Furthermore, Tribune was converted from a C corporation to a Subchapter S corporation, allowing the firm to avoid corporate income taxes. However, it would have to pay taxes on gains resulting from the sale of assets held less than ten years after the conversion from a C to an S corporation (Figure 1).  Figure 13.1

Figure 13.1

Tribune deal structure.

The purchase of Tribune's stock was financed almost entirely with debt, with Zell's equity contribution amounting to less than 4% of the purchase price. The transaction resulted in Tribune being burdened with $13 billion in debt (including the approximate $5 billion currently owed by Tribune). At this level, the firm's debt was ten times EBITDA, more than two and a half times that of the average media company. Annual interest and principal repayments reached $800 million (almost three times their preacquisition level), about 62% of the firm's previous EBITDA cash flow of $1.3 billion. While the ESOP owned the company, it was not be liable for the debt guaranteed by Tribune.

The conversion of Tribune into a Subchapter S corporation eliminated the firm's current annual tax liability of $348 million. Such entities pay no corporate income tax but must pay all profit directly to shareholders, who then pay taxes on these distributions. Since the ESOP was the sole shareholder, Tribune was expected to be largely tax exempt, since ESOPs are not taxed.

In an effort to reduce the firm's debt burden, the Tribune Company announced in early 2008 the formation of a partnership in which Cablevision Systems Corporation would own 97% of Newsday for $650 million, with Tribune owning the remaining 3%. However, Tribune was unable to sell the Chicago Cubs (which had been expected to fetch as much as $1 billion) and the minority interest in SportsNet Chicago to help reduce the debt amid the 2008 credit crisis. The worsening of the recession, accelerated by the decline in newspaper and TV advertising revenue, as well as newspaper circulation, thereby eroded the firm's ability to meet its debt obligations.

By filing for Chapter 11 bankruptcy protection, the Tribune Company sought a reprieve from its creditors while it attempted to restructure its business. Although the extent of the losses to employees, creditors, and other stakeholders is difficult to determine, some things are clear. Any pension funds set aside prior to the closing remain with the employees, but it is likely that equity contributions made to the ESOP on behalf of the employees since the closing would be lost. The employees would become general creditors of Tribune. As a holder of subordinated debt, Mr. Zell had priority over the employees if the firm was liquidated and the proceeds distributed to the creditors.

Those benefitting from the deal included Tribune's public shareholders, including the Chandler family, which owed 12% of Tribune as a result of its prior sale of the Times Mirror to Tribune, and Dennis FitzSimons, the firm's former CEO, who received $17.7 million in severance and $23.8 million for his holdings of Tribune shares. Citigroup and Merrill Lynch received $35.8 million and $37 million, respectively, in advisory fees. Morgan Stanley received $7.5 million for writing a fairness opinion letter. Finally, Valuation Research Corporation received $1 million for providing a solvency opinion indicating that Tribune could satisfy its loan covenants.

What appeared to be one of the most complex deals of 2007, designed to reap huge tax advantages, soon became a victim of the downward-spiraling economy, the credit crunch, and its own leverage. A lawsuit filed in late 2008 on behalf of Tribune employees contended that the transaction was flawed from the outset and intended to benefit Sam Zell and his advisors and Tribune's board. Even if the employees win, they will simply have to stand in line with other Tribune creditors awaiting the resolution of the bankruptcy court proceedings.

:

-Is this transaction best characterized as a merger,acquisition,leveraged buyout,or spin-off? Explain your

answer.

Correct Answer:

Verified

A leveraged buyout,since the T...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q10: Which of the following characteristics of a

Q12: Which of the following is not true

Q24: Case Study Short Essay Examination Questions<br>Financing LBOs--The

Q56: When a public company is subject to

Q70: Pacific Investors Acquires California Kool in a

Q108: A leveraged buyout initiated by a firm's

Q111: Photography Icon Kodak Declares Bankruptcy, A Victim

Q119: The high premiums paid to LBO target

Q120: Debt issues not secured by specific assets

Q124: Because of their high liquidity, lenders often