Essay

Use the table for the question(s)below.

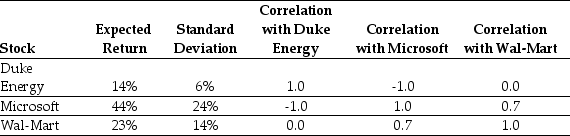

Consider the following expected returns,volatilities,and correlations:

-Consider a portfolio consisting of only Microsoft and Wal-Mart stock.Calculate the volatility of such a portfolio when the weight on Microsoft stock is 0%,25%,50%,75%,and 100%

Correct Answer:

Verified

Var(Rp)= x12Var(...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q21: Use the table for the question(s)below.<br>Consider the

Q26: Use the information for the question(s)below.<br>Suppose you

Q29: Use the following information to answer the

Q29: Use the table for the question(s)below.<br>Consider the

Q32: Use the information for the question(s)below.<br>Suppose you

Q34: Use the information for the question(s)below.<br>Tom's portfolio

Q57: Which of the following statements is FALSE?<br>A)The

Q100: Consider an equally weighted portfolio that contains

Q105: Use the table for the question(s)below.<br>Consider the

Q110: Use the information for the question(s)below.<br>Suppose you