Essay

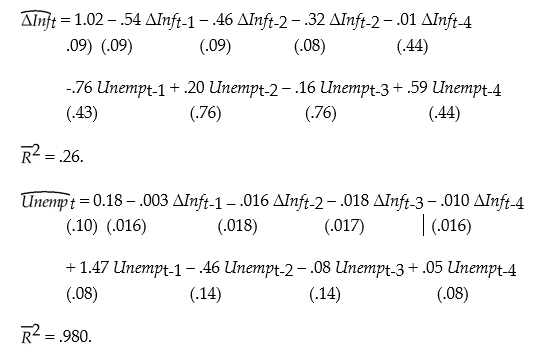

You have collected quarterly data on inflation and unemployment rates for Canada from 1961:III to 1995:IV to estimate a VAR(4)model of the change in the rate of inflation and the unemployment rate. The results are

(a)Explain how you would use the above regressions to conduct one period ahead forecasts.

(b)Should you test for cointegration between the change in the inflation rate and the unemployment rate and, in the case of finding cointegration here, respecify the above model as a VECM?

(c)The Granger causality test yields the following F-statistics: 3.75 for the test that the coefficients on lagged unemployment rate in the change of inflation equation are all zero; and 0.36 for the test that the coefficients on lagged changes in the inflation rate are all zero. Based on these results, does unemployment Granger-cause inflation? Does inflation Granger-cause unemployment?

Correct Answer:

Verified

(a)One period ahead forecasts are the sa...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q40: The error term in a multiperiod regression<br>A)is

Q41: Using the ADL(1,1)regression Y<sub>t</sub> = ?<sub>0</sub>

Q42: The following is not a consequence of

Q43: If Y<sub>t</sub> is I(2), then<br>A)Δ2Y<sub>t</sub> is stationary.<br>B)Y<sub>t</sub>

Q44: The biggest conceptual difference between using VARs

Q46: Consider the following model Y<sub>t</sub> =

Q47: In a VECM,<br>A)past values of Y<sub>t</sub> -

Q48: Economic theory suggests that the law

Q49: A VAR allows you to test joint

Q50: You can determine the lag lengths in