Multiple Choice

The following data relate to Questions 18-22:

During the year ended June 30 20X7, Johnson Ltd became deeply involved in trade with Malaysia. On July 1 20X6, the company acquired 50% of the share capital of a Malaysian palm oil producer, Plantations Berhad, for $7,000,000. For the year ended June 30 20X7, the following balance sheet and income statement were prepared by Plantations Berhad (amounts in thousands) :

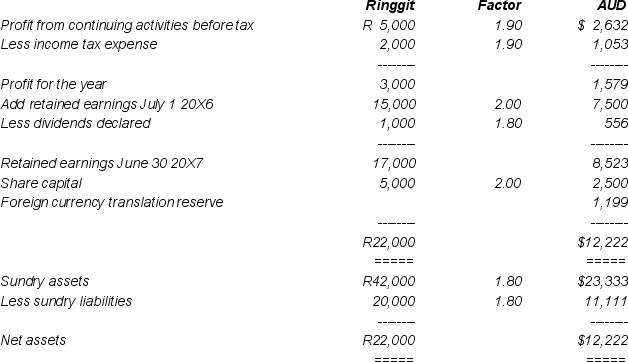

Income Statement for the Year ended June 30 20X7

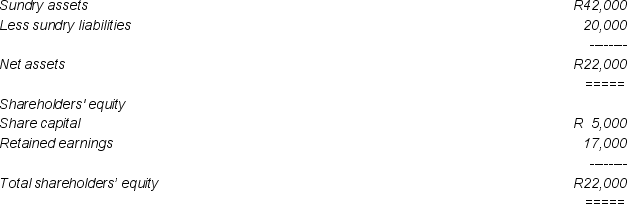

Balance Sheet as at June 30 20X7

Balance Sheet as at June 30 20X7

Statement of the Movement in Retained Earnings in the Year ended June 30 20X7

Statement of the Movement in Retained Earnings in the Year ended June 30 20X7

The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands) :

The functional currency of Plantations Berhad was Malaysian Ringgit. The following translation statement was prepared for the company (amounts in thousands) :

Additional information:

Additional information:

a) A deferred tax liability of 30% of the foreign currency translation reserve is to be recognised.

b) On July 1 20X6, as a partial hedge against its investment in Plantations Berhad, Johnson Ltd took out a three (3) year loan of R 8,000,000 from the Bank Negara at 12% interest, with interest payable quarterly commencing September 30 20X6.

c) On May 15 20X7 Johnson Ltd placed an order for R 2,000,000 in merchandise for resale from Malaysian Industries Berhad, payable in USD. The goods were shipped FOB on May 31 with settlement due on July 31 20X7.

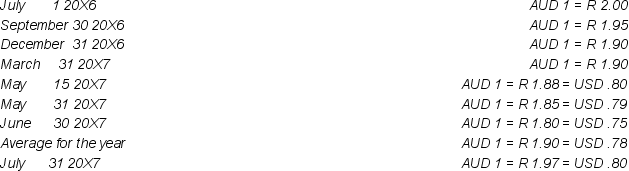

At relevant dates the exchange rates were:

-At June 30 20X7 Johnson Ltd recognised its equity in the dividends declared by Plantations Berhad in its income statement.When the dividend was subsequently received from Plantations Berhad,the exchange rate was AUD 1 = R 1.78.The exchange gain or loss recognised by Johnson Ltd on receiving that dividend was (rounded to the nearest dollar)

A) A gain of $6,242

B) A loss of $3,121

C) A gain of $3,121

D) None of the above.

Correct Answer:

Verified

Correct Answer:

Verified

Q1: Under the temporal method,all revenue and expense

Q14: Discuss the treatment of differences in accounting

Q18: A 'natural hedge' occurs when an Australian

Q19: The following data relate to Questions 18-22:<br>During

Q20: Translation of financial statements into the presentation

Q21: The presentation currency will be determined by:<br>A)

Q22: The following data relate to Questions 18-22:<br>During

Q25: Under the current rate method foreign exchange

Q26: Translation of financial statements of foreign operations

Q28: The term 'foreign currency transaction' refers to