Not Answered

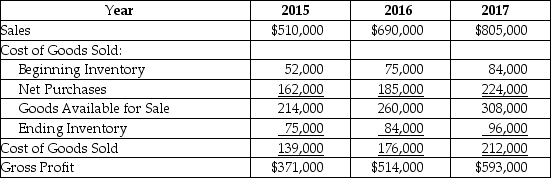

Courtney's Cafes,Inc.CFO discovered a series of errors in its inventory system in early 2018,when he was making year-end adjustments to the financial statements for 2017.The errors began in 2015.Below is a summary of the sales and cost of goods sold on income statement items for the three years:

Upon further analysis,the CFO determined that each of the years had ending inventory errors.The correct amounts for the years were: 2015,$63,000; 2016,$101,000; and 2017,$106,000.The amounts for 2015 beginning inventory and all purchases are correct as stated.

Upon further analysis,the CFO determined that each of the years had ending inventory errors.The correct amounts for the years were: 2015,$63,000; 2016,$101,000; and 2017,$106,000.The amounts for 2015 beginning inventory and all purchases are correct as stated.

Required:

Correct Answer:

Verified

Correct Answer:

Verified

Q18: Retrospective changes require restatement of all periods

Q31: When there is a guaranteed residual value,

Q42: For a lessor to classify a lease

Q44: Judgments are important in determining which type

Q47: A material error is one that if

Q50: A material error in ending inventory requires

Q51: The financing cash flows section is based

Q52: Which of the following is a cash

Q52: During 2015,a $50,000 loss on the sale

Q53: The conceptual model for the statement of