Essay

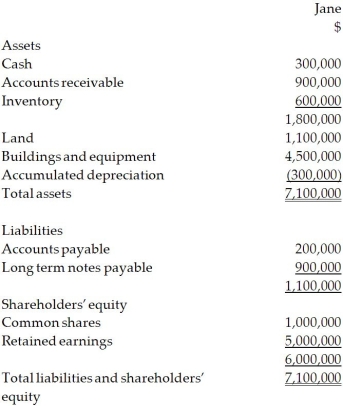

On December 31, 20X2, Esther Company purchased 80% of the outstanding common shares of Jane Company for $7.5 million in cash. On that date, the shareholders' equity of Jane totalled $6 million and consisted of $1 million in no par common shares and $5 million in retained earnings. Both companies use the straight-line method to calculate depreciation and amortization. The statement of financial position for Jane is provided below at December 31, 20X2.  For the year ending December 31, 20X4, the statements of comprehensive income for Esther and Jane were as follows: At December 31, 20X4, the condensed statement of financial position for the two companies were as follows:

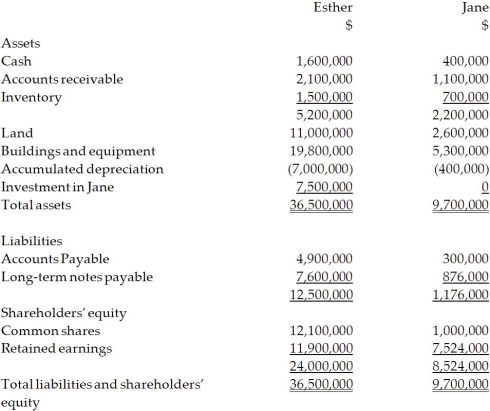

For the year ending December 31, 20X4, the statements of comprehensive income for Esther and Jane were as follows: At December 31, 20X4, the condensed statement of financial position for the two companies were as follows:  OTHER INFORMATION:

OTHER INFORMATION:

1. On December 31, 20X2, Jane had a building with a fair value that was $450,000 greater than its carrying value. The building had an estimated remaining useful life of 15 years.

2. On December 31, 20X2, Jane had inventory with a fair value that was $150,000 less than its carrying value. This inventory was sold in 20X3.

3. During 20X3, Jane sold merchandise to Esther for $100,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Esther and the other 60% remained in its December 31, 20X3, inventories. On December 31, 20X4, the inventories of Esther contained merchandise purchased from Jane on which Jane had recognized a gross profit in the amount of $20,000. Total sales from Jane to Esther were $150,000 during 20X4.

4. During 20X4, Esther declared and paid dividends of $300,000, while Jane declared and paid dividends of $100,000.

5. Esther accounts for its investment in Jane using the cost method.

Required:

Calculate goodwill on the consolidated balance sheet at December 31, 20X4, under the entity method and the parent-company extension method. Explain the differences between the two balances.

Correct Answer:

Verified

Entity method  Parent company extension ...

Parent company extension ...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q18: Bates Ltd. owns 60% of the

Q19: On December 31, 20X5, Paper Co.

Q20: Assume that a parent company has four

Q21: Which of the following is not a

Q22: On December 31, 20X5, Paper Co.

Q24: On December 31, 20X5, Paper Co.

Q25: Which consolidation approach excludes the NCI?<br>A)Proportionate consolidation<br>B)Parent-company

Q26: Portia Ltd. acquired 80% of Siro Ltd.

Q27: Olthius Ltd. purchased 60% of Fredo Ltd.

Q28: On December 31, 20X6, the balance