Essay

On January 1, 2016, Parent Company purchased 100% of the common stock of Subsidiary Company for $390,000.On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $50,000, $100,000, and $200,000 respectively.Any excess of cost over book value is due to goodwill.Parent accounts for the Investment in Subsidiary using the simple equity method.

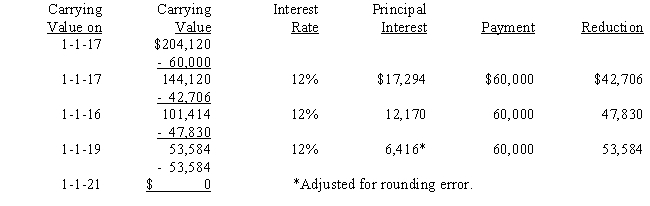

On January 1, 2017, Parent purchased equipment for $204,120 and immediately leased the equipment to Subsidiary on a 4-year lease.The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.

A lease amortization schedule, applicable to either company, is presented below:

On January 1, 2016, Parent held merchandise acquired from Subsidiary for $10,000.During 2016, subsidiary sold merchandise to Parent for $50,000, of which $15,000 is held by Parent on December 31, 2016.Subsidiary's usual gross profit on affiliated sales is 40%.

On January 1, 2016, Parent held merchandise acquired from Subsidiary for $10,000.During 2016, subsidiary sold merchandise to Parent for $50,000, of which $15,000 is held by Parent on December 31, 2016.Subsidiary's usual gross profit on affiliated sales is 40%.

Required:

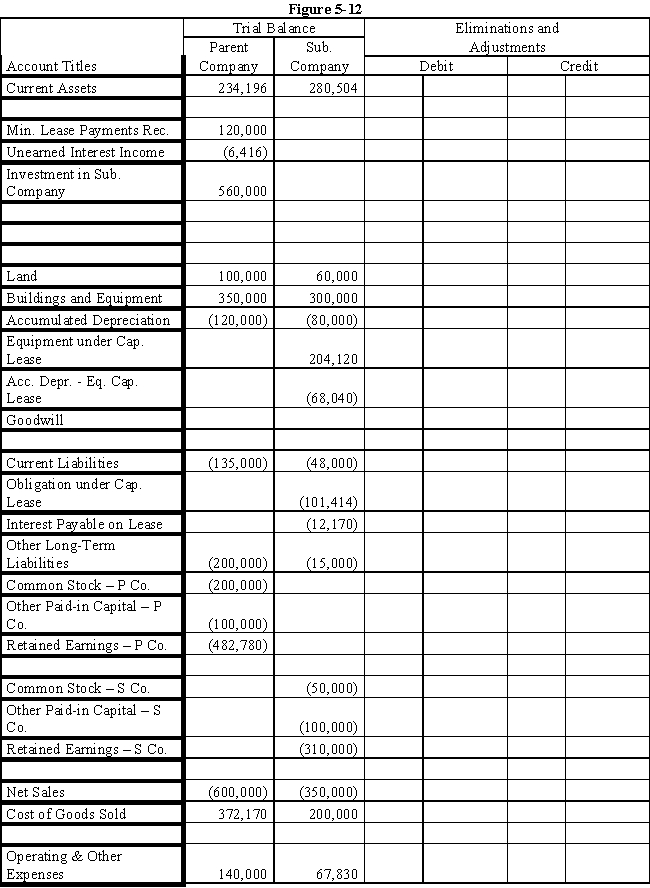

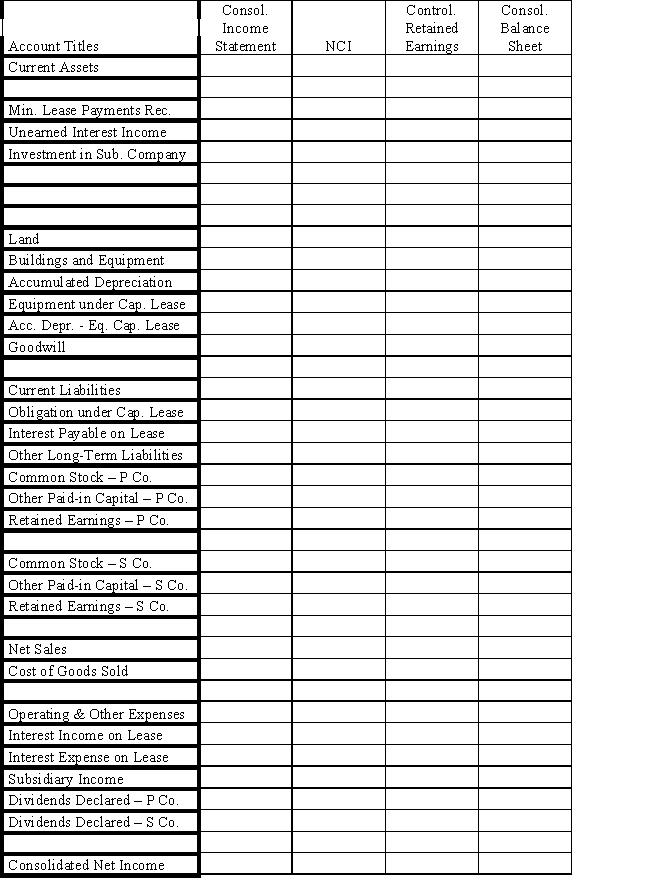

Complete the Figure 5-12 worksheet for consolidated financial statements for the year ended December 31, 2016.Round all computations to the nearest dollar.

Correct Answer:

Verified

Answer 5-12.

...

...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q30: Company S is a 100%-owned subsidiary of

Q31: The effect of an operating lease on

Q32: Company S is a 100%-owned subsidiary of

Q33: Company S is a 100%-owned subsidiary of

Q34: Lease terms can be considered to be

Q36: Soap Company issued $200,000 of 8%, 5-year

Q37: The motivation of a parent company to

Q38: Company P owns 80% of Company S.On

Q39: Elimination procedures for intercompany bonds purchased from

Q40: A subsidiary has outstanding $100,000 of 8%