Multiple Choice

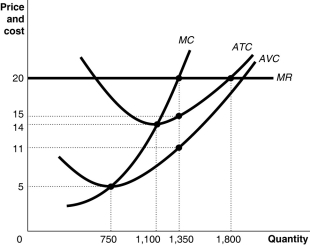

Figure 7-5  Figure 7-5 shows cost and demand curves facing a typical firm in a constant-cost, perfectly competitive industry.

Figure 7-5 shows cost and demand curves facing a typical firm in a constant-cost, perfectly competitive industry.

-Refer to Figure 7-5.What is the minimum price the firm requires to produce output?

A) $20

B) $14

C) $5

D) It cannot be determined.

Correct Answer:

Verified

Correct Answer:

Verified

Q17: Which of the following is not a

Q42: How are sunk costs and fixed costs

Q73: Firms in perfectly competitive industries are unable

Q160: Which of the following describes a situation

Q165: If the market price is $25 in

Q199: What characteristic of a competitive market has

Q210: A perfectly competitive industry achieves allocative efficiency

Q238: Ben's Peanut Shoppe suffers a short-run loss.Ben

Q266: In the long run, a perfectly competitive

Q275: What assumptions are necessary for a market