Multiple Choice

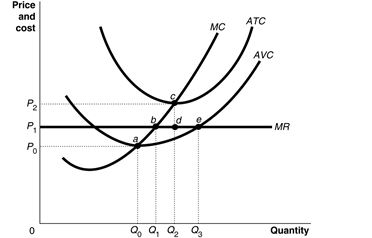

-Refer to Figure 7-11.Suppose the prevailing price is P1 and the firm is currently producing its loss-minimising quantity.In the long-run equilibrium

A) there will be fewer firms in the industry and total industry output decreases.

B) there will be more firms in the industry and total industry output increases.

C) there will be fewer firms in the industry but total industry output increases.

D) there will be more firms in the industry and total industry output remains constant.

Correct Answer:

Verified

Correct Answer:

Verified

Q55: A firm could continue to operate for

Q63: Ethan Nicholas, who developed the iShoot application

Q88: Market supply is found by<br>A)vertically summing the

Q111: A perfectly competitive firm in a constant-cost

Q112: A constant-cost industry is an industry in

Q113: Competition has driven the economic profits in

Q206: A perfectly competitive firm's marginal revenue<br>A)is greater

Q209: For a perfectly competitive firm, which of

Q217: When firms exit a perfectly competitive industry,

Q241: If firms do not earn economic profits