Multiple Choice

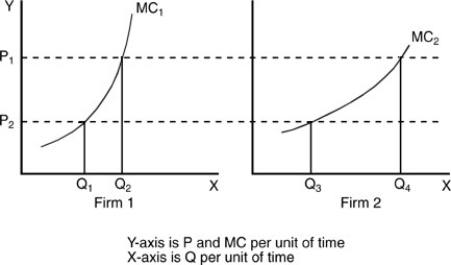

-In the above figure, assuming Firm 1 and Firm 2 are the sole producers in the industry, the industry quantity supplied at price P2 is equal to

A) Q1 + Q2.

B) Q1 + Q3.

C) Q2 + Q4.

D) Q4 - Q2.

Correct Answer:

Verified

Correct Answer:

Verified

Related Questions

Q44: If an industry's long-run per-unit costs are

Q45: The change in total revenues resulting from

Q46: Why is the pricing outcome of a

Q47: The firm in a perfectly competitive industry

Q48: A firm is currently producing at the

Q50: For a perfect competitor, the marginal revenue

Q51: If markets are perfectly competitive, then the

Q52: Which of the following best describes a

Q53: Under perfect competition, a firm that sets

Q54: If the long-run supply curve is horizontal,