Multiple Choice

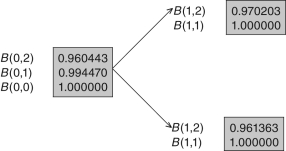

Use the following tree to answer the questions that follow.

-What are the dollar returns on the one-period zero-coupon bond in the up and down nodes?

A) 1.0307,1.0402

B) 1.0102,1.0010

C) 1.0102,1.0102

D) 1.0056,1.0056

E) 1.0056,1.0402

Correct Answer:

Verified

Correct Answer:

Verified

Q1: The following is NOT an assumption underlying

Q2: An interest rate cap is:<br>A) a European

Q3: Use the following tree to answer the

Q5: Which of the following statements is correct?<br>A)

Q6: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB4275/.jpg" alt=" Use the fact

Q7: Which of the following statements about the

Q8: An interest rate floor is:<br>A) a European

Q9: A necessary and sufficient condition to

Q10: Assume zero-coupon bond prices are B(0,0)= $1,B(0,1)=

Q11: Assume zero-coupon bond prices are B(0,0)=$1,B(0,1)= $0.967846,B(0,2)=$0.943010.What